The Governor's Concluding Remarks for 2025

Ladies and Gentlemen,

Last year the global economy was unexpectedly resilient. GDP grew by 3.4 per cent, half a point more than expected, despite the ongoing conflicts in Ukraine and Gaza, tighter US tariffs and the hostilities in the Middle East.

US growth exceeded 2 per cent. Artificial intelligence (AI) was a driving force behind this momentum: the construction of data centres supported investment, and the rise in the equity prices of the companies that are spearheading this transformation increased financial wealth and boosted consumption.

China also contributed significantly to the global expansion, growing by 5 per cent. Faced with weak domestic demand, Chinese firms responded to US tariffs by lowering prices in foreign markets and diversifying their trade outlets. This is an effective strategy in the very short term, but a fragile one in the long run, as it does not address domestic deflationary pressures and fuels new protectionist responses.

Global economic activity also benefited from the easing of monetary conditions made possible by the disinflationary environment.

Optimism prevailed in financial markets, resulting in high equity valuations, low risk premia and the search for yields in less transparent segments. The appreciation of gold and bitcoin and the rapid expansion of private credit pointed to the risk of valuations being overly optimistic in some areas of the market.

These signals became more apparent between 2025 and 2026. The instruments that had benefited more from the expansionary phase gave back some of their gains and valuations started to incorporate risks that investors had long underestimated.

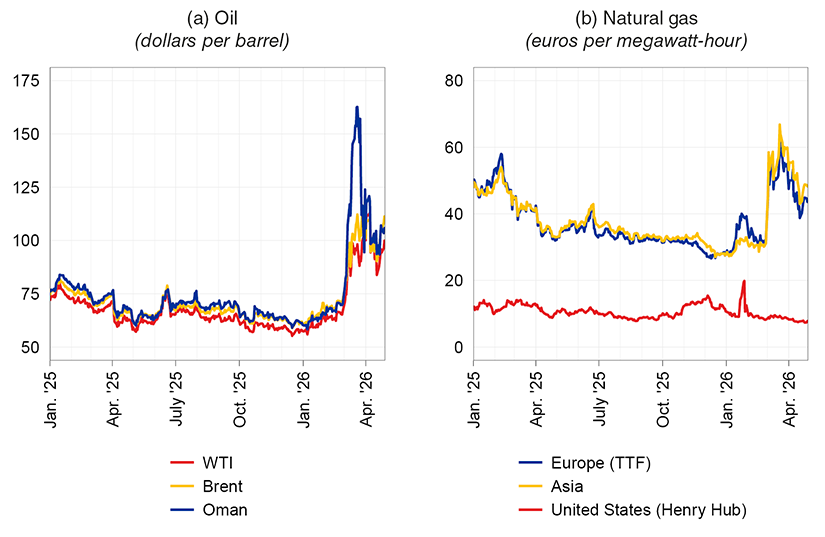

The situation has been changed dramatically by the conflict in the Persian Gulf. The blockade of the Strait of Hormuz - which would normally be the conduit for one fifth of global oil and liquefied gas supplies - has led to supply shortages and strong price increases for energy commodities.

Oil prices have risen across all geographical areas, reflecting the integration of global production and distribution chains (Figure 1.a). In the more fragmented gas market, prices have followed different patterns: they have gone up in Europe and Asia, which rely on imports; they have remained stable in the US, where abundant domestic production and infrastructure constraints on exports mitigate the pass-through of international tensions to domestic prices (Figure 1.b).

Figure 1

Energy commodity prices

Source: Based on London Stock Exchange Group (LSEG) data.

These pressures are extending to raw materials that are essential for many sectors. The surge in fertilizer prices is particularly worrisome. Its effects on food prices will materialize in full at the beginning of next year, once the sowing and harvesting cycles are over. This will aggravate food insecurity, potentially pushing tens of millions of people in low-income countries into extreme poverty.

Consumer prices and short-term inflation expectations are on the rise everywhere. A few years on from the post-pandemic inflationary shock, expectations of a timely response from central banks are exacerbating the rise in interest rates across all maturities.

The economic outlook has deteriorated sharply.

Higher energy prices are eroding households' disposable income and squeezing firms' margins. Rising yields are tightening financial conditions. Public debt, after years of expansionary policies, leaves little scope for support measures.

Assuming a rapid resolution of the conflict, the IMF forecasts global growth to drop to 3.1 per cent in 2026, with inflation at 4.4 per cent, almost 1 percentage point higher than estimated last year. The scenario would be much worse if the conflict were to continue.

It is difficult to determine how long hostilities will last and how stable the post-war order will be. In any case, the damage to energy infrastructure will continue to weigh on supplies; freight and insurance costs for shipping through the Strait of Hormuz will remain high for a long time. Uncertainty is bound to stay at elevated levels, hindering household and business planning and curbing consumption and investment.

There is also a risk of financial amplification. At the outbreak of the conflict, investors shifted towards safe assets, resulting in an appreciation of the dollar, rising risk premia and capital outflows from emerging markets.

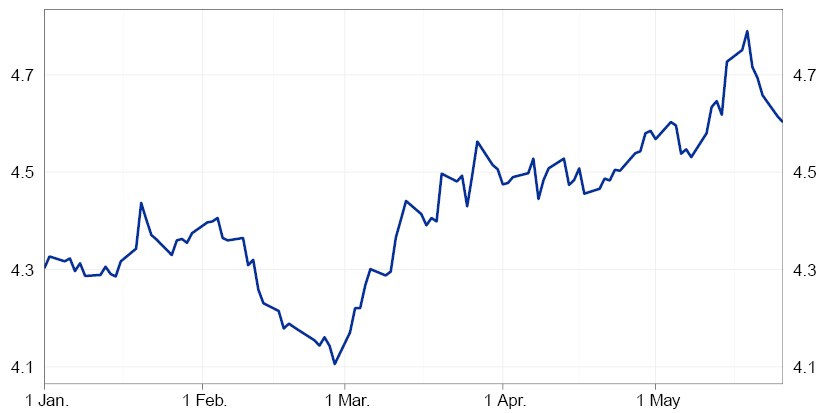

More recently, equity prices have recovered losses. This is a sign of confidence but may also reflect an underestimation of the economic effects of the crisis. The surge in long-term interest rates in recent weeks is at odds with this rebound and points to persisting tensions in financial markets (Figure 2).

Figure 2

G7 countries' long-term government bond yields in 2026

(per cent)

Sources: ICE BofA Merrill Lynch and NBER.

(1) Weighted average yield on G7 government bonds with a maturity of 10 years or more.

The broad picture remains fragile. With high public debt and increasing vulnerabilities in non-bank financial intermediation, even limited shocks can generate ripple effects.

Global growth is exposed to risks that are more numerous, more interconnected and more difficult to govern than in the past.

Trade

Global trade was stronger than expected in 2025, with 5 per cent growth. One contributing factor was a substantial geographical re-direction of flows - which helped to partially circumvent trade barriers - and by US tariffs that were lower than initially announced. AI-related goods accounted for about half of the increase in global merchandise trade flows.

Protectionist policies have not reduced the imbalances that they intended to correct. The US goods trade deficit has remained unchanged as a share of GDP, as a number of factors have continued to fuel import growth;1 90 per cent of the tariffs were passed on to US consumers and firms.2 In parallel, China has strengthened its global trade presence, resulting in very large surpluses.3

Looking ahead, there is a risk of international trade weakening. According to the IMF, persistently high trade barriers would reduce world trade growth to below 3 per cent in 2026; the Gulf conflict could exacerbate the slowdown.

The picture emerging from these turbulent years reveals a fundamental contradiction. Concerns about economic security and strategic independence are driving governments to reduce foreign reliance and to protect essential sectors. These are now vital goals. However, if pursued through indiscriminate fragmentation, these efforts would end up restricting markets, increasing costs, weakening value chains, and reducing incentives for cooperation and compliance with rules. They would thus undermine precisely what they are intended to protect: the well-being of citizens.

Going back to the previous order is unrealistic. However, the benefits of international openness must be preserved, by correcting its distortions and preventing interdependence from turning into a permanent source of vulnerability. Ties with countries that recognize the value of relationships based on a common set of rules must be strengthened.

The multilateral system built after World War II, albeit imperfect and sometimes unbalanced, fostered integration and economic growth for eight decades. Its strength was not to remove international tensions, but to govern them through shared rules.

Beyond the current contingencies, it is essential to tackle the factors that have gradually eroded this system: the increasingly asymmetric application of rules, distortive industrial policies, persistent macroeconomic imbalances and an unequal distribution of the benefits of integration.

In a world that remains deeply interconnected, fragmentation does not eliminate imbalances: it shifts them, hides them, and makes them deeper and more expensive to correct.

Global imbalances

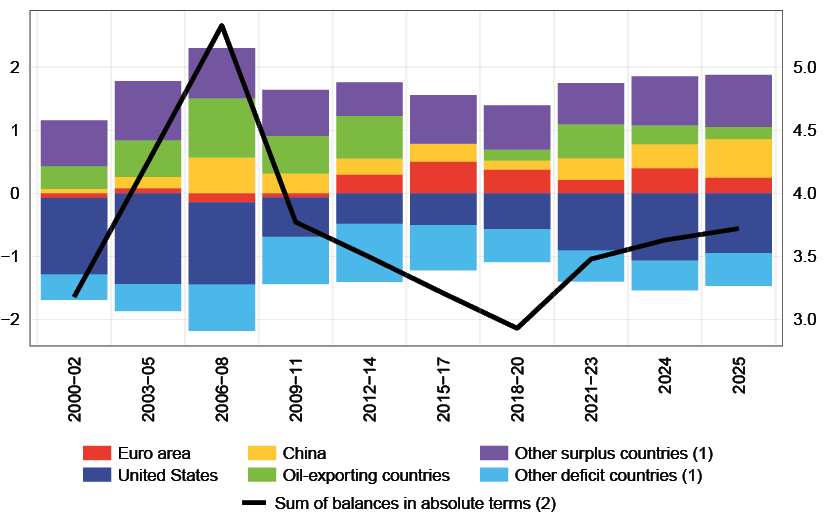

International current account balances in the balance of payments widened in 2025, reaching their highest level since the global financial crisis (Figure 3).

Figure 3

Current account balances

(per cent of global GDP)

Source: Based on IMF data, World Economic Outlook. Global Economy in the Shadow of War, April 2026.

(1) The main countries running surpluses in 2025 were Japan, Taiwan, South Korea, Singapore and Switzerland; the main countries with deficits were the United Kingdom, Brazil and Australia. − (2) Right-hand scale.

The United States accounts for two thirds of the global deficit. On the other end, China accounts for about one third of the surplus; the European share is smaller.

Positive or negative balances are normal in open economies. They become excessive if they surpass the level warranted by structural differences between countries - whether demographic or linked to growth prospects - and if they reflect unsustainable choices in national development strategies and in fiscal, industrial and financial policies.4

The US current account deficit is fuelled by a high public deficit and low household savings. China's surplus reflects a growth model that holds back consumption and stimulates exports, including through policies to support manufacturing.5 Europe's surplus points to the chronic difficulty of turning savings into innovative investment.

The persistence of these imbalances has resulted in large international negative and positive net investment positions. The United States has a net negative investment position of 90 per cent of GDP, which mirrors the positive positions of China, other Asian economies and the euro area. The income generated by these positions - in the form of interest and dividends - tends to widen imbalances.

This poses material risks to financial stability. Large economies' excessive surpluses compress real rates globally, favouring risk-taking and debt accumulation.6 In deficit countries, tighter financing conditions can lead to sharp increases in risk premia, with repercussions on capital flows.

The energy crisis can lead to a partial and temporary correction, with a smaller surplus for China, which is a net importer of energy, and a contained deficit for the US, an oil and gas exporter. However, it does not affect the structural causes of imbalances.

A sustained adjustment would require major corrections: in the United States, a reduction in the public deficit; in China, stronger domestic consumption, a scaling down of distortive industrial policies and greater exchange rate flexibility; in Europe, a sizeable increase in investment and the full integration of the single market.7

IMF analysis suggests that these corrections, if coordinated across the three large areas, would reduce global imbalances, while increasing world GDP by 1 per cent.8 They would also enable a significant reduction in financial risks, which would be hard to achieve through adjustments limited to surplus or deficit countries alone.9

Imbalances that build up without being governed are rarely reabsorbed in an orderly manner. More often, they escalate into trade tensions, as in the 1980s before the Plaza Accord,10 or into financial risks, as was the case before the 2008 global crisis.

Reducing imbalances is in the interest of individual countries and is essential for global stability. It requires consistent national policies, the effects of which are reinforced by international cooperation. Without cooperation, interdependence risks channelling crises, rather than providing a framework to govern them.

The impact of artificial intelligence on the economy and work

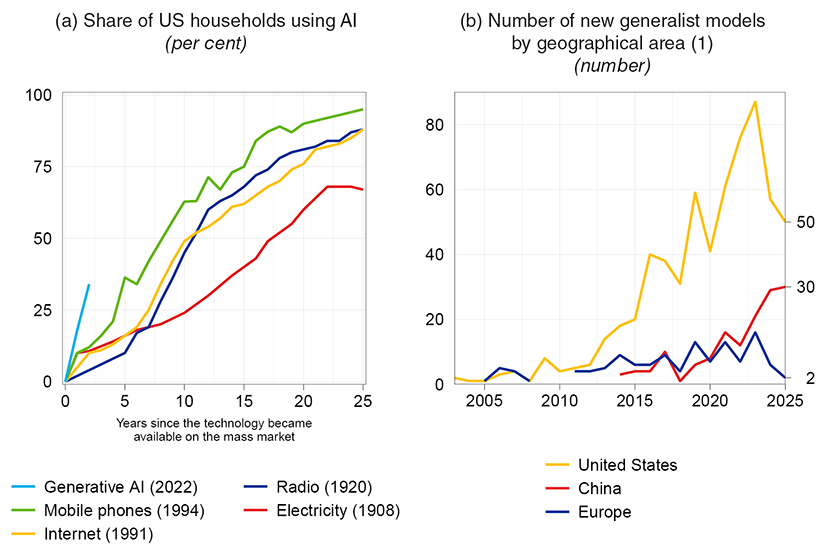

Artificial intelligence is already part of macroeconomic developments. It supports investment, trade and financial valuations. Yet its reach is wider: like all general-purpose transformative technologies, it is redefining how we produce, work and make decisions.11 It is spreading faster than previous technological revolutions (Figure 4.a), with AI investment growing exponentially. We are no longer in an experimental phase.

The development of frontier models, and the resulting economic and strategic power, is highly concentrated. Five large US firms hold around three quarters of the world's computing capacity. Most general-purpose models are being developed in the United States (Figure 4.b); China is rapidly closing the gap, while Europe is lagging behind.

Figure 4

Recent developments in AI

Sources: Based on data from Our World in Data (Share of United States households using specific technologies) and Microsoft AI Economy Institute, AI diffusion report: where AI is most used, developed, and built, November 2025; S. Sajadieh et al., The AI Index 2026 Annual Report, AI Index Steering Committee, Stanford Institute for Human-Centered Artificial Intelligence, Stanford University, Stanford, CA, April 2026.

(1) AI models are selected based on innovation, impact and performance criteria.

However, this concentration does not preclude widespread benefits. In big technological revolutions, the greatest gains often went to those able to adopt and apply a new technology, rather than to those who originated it. The race for growth will play out on this ground.

Artificial intelligence is finding application in increasingly wide-ranging fields, from production processes to services and healthcare. In manufacturing, it is improving design, plant maintenance and the organization of supply chains;12 in biomedical research, it is accelerating the development of new drugs.13 Its broad adoption can translate into significant productivity gains.14

AI's impact on work deserves special attention. For the first time, a technology can perform tasks involving highly cognitive skills, which have so far been regarded as safe from automation. That technical progress is transforming labour demand is nothing new; what is new is the scope of activities that are potentially being affected.

However, history shows that major innovations do not merely render some professions obsolete: they generate new ones. The latter have accounted for half of US employment growth since the turn of the century; today, 60 per cent of those in employment perform tasks that did not exist 80 years ago.15

Moreover, by reducing costs and prices, AI-induced productivity gains could expand demand, boost economic activity and support employment.16

The content of work will change, although it is not yet possible to fully predict how it will develop. In some cases, artificial intelligence will work side by side with humans, allowing them to focus on higher value-added activities; in others, the human contribution will be redefined around what automation cannot replace: interpreting results, exercising judgement and ensuring process reliability.

The transition will not be without cost. Not all workers can easily switch from obsolete to new tasks; the more highly skilled ones could reap greater benefits, which would exacerbate inequalities.17

For artificial intelligence to become a driver of widespread growth, it will be necessary to encourage its adoption across firms, including small and medium-sized enterprises, and to invest in people's skills. The workers most exposed to change will need to be protected and retrained, so that productivity gains translate not only into greater efficiency, but also into new job opportunities and a broader sharing of the benefits of innovation.

Europe

The real economy and inflation

Euro-area GDP rose by 1.4 per cent in 2025; excluding Ireland's contribution, which is influenced by the statistical treatment of the business of multinational firms, growth remained at around 1.0 per cent.

Economic activity was affected, especially in Germany and Italy, by the weakness of the manufacturing sector, which was particularly exposed to increasing international competition. China's competitive pressure contributed to dampening exports and investment, including investment in intellectual property, which are crucial for the medium-term outlook.18 Households' propensity to save remained high, at a time of persisting uncertainty.

Inflation has returned to the 2 per cent medium-term target, reflecting lower pressures from both demand and costs. This has allowed the ECB Governing Council to cut its key interest rates by a total of 100 basis points, and to keep them unchanged since last June.

The outbreak of the conflict in the Middle East has led to a considerable deterioration in the macroeconomic situation since March. Household confidence has fallen sharply, returning to 2022 levels, and anticipating weaker consumption. The outlook has also deteriorated for service firms, which had been the main driver of economic activity up until then.

Financial conditions have become more restrictive: yields have risen, sovereign spreads have widened and European banks have tightened their credit standards and plan to continue to do so, all of which will affect investment.

The increase in commodity prices has already affected fuel prices and is passing through to energy prices. Indirect effects on the prices of other goods and services will emerge gradually, at an intensity that will depend on the time frame for resolving the crisis.

According to the ECB's March 2026 projections, in the baseline scenario - in which the energy shock would rapidly be absorbed - growth in the euro area will go down to 0.9 per cent in 2026, before rising to 1.5 per cent in the following two years. Inflation will rise to 2.6 per cent in 2026, and then to return to the target.

In the less favourable scenarios, a prolongation of the conflict and further damage to the Gulf's energy infrastructures could subtract 1 percentage point overall from growth in the two years 2026-27. Inflation could peak at more than 6 per cent and, if left unchecked, remain above target for some time, while the energy shock gradually spreads to a growing number of sectors.

Monetary policy

Given the high uncertainty over the evolution of inflation and economic activity, in April, the Governing Council considered it appropriate to keep the monetary policy stance unchanged and to await further information.

The conditions for countering inflation are more favourable than in the years 2021-22: the key interest rates, which were negative then, are now in line with the estimates for the neutral rate;19 domestic demand is weaker. Moreover, although medium-term inflation expectations are susceptible to pressures, they remain firmly anchored to the target and there are no wage tensions.

However, the forward-looking picture seems to call for a recalibration of the monetary policy stance to counter the risk of persistent inflationary tensions. The energy shock is already pushing up consumer prices. Even in the event of a rapid resolution of the conflict, a swift normalization of oil and gas prices seems unlikely.

Firms have already started to anticipate increasing their selling prices, and consumers' inflation expectations are rising, especially in the short term. The reduction in inventories of gas and oil products and the emergence of new issues in global supply chains could further amplify these trends.

Monetary policy cannot prevent higher energy prices from spreading throughout the economy, but it must prevent this process from sparking persistent inflation, embedded in the expectations and choices of firms and workers. A wage-price spiral must be averted, as once it has begun, it would be harmful and costly to eliminate.

The Governing Council will decide in June, based on the information available at that time and on the new projections. It will be crucial to assess the extent to which higher energy prices can pass through to other prices and how much they can affect consumption, investment and economic activity. The calibration of the monetary response will depend on this assessment.

Not being tied to a predetermined path remains essential. The Governing Council will act in a timely and measured manner to prevent the energy shock from turning into persistent inflation.

Defending price stability means preserving households' purchasing power, business confidence and the conditions for lasting growth.

European policies

The European Union is entering this new phase of international instability with unresolved fragilities, which are limiting its growth potential and its weight in the global economy.

Foreign dependence in strategic sectors - from defence to energy and to advanced technologies - is more noticeable today than in the past. The single market remains incomplete, precisely in sectors such as finance, energy and telecommunications, which could best support economic growth and strategic autonomy.

These issues are at the heart of the 'Competitiveness Compass'.20 Three of the initiatives launched are particularly important for the real economy: the Industrial Accelerator Act,21 the 28th Regime22 and the European Grids Package.23 If they are implemented decisively, they could strengthen industrial capacity, support innovative firms and speed up the energy transition.

However, reforms are progressing slowly: less than half of the legislative proposals on competitiveness and security announced for the years 2025-26 have been presented so far, and less than one quarter of these have been formally adopted.24

International instability leaves no room for hesitation or incomplete responses. The effectiveness of the reforms will depend on Europe's ability to overcome the obstacles that too often slow down their implementation: long negotiations, watered-down compromises, uneven application at national level and resources announced but still not mobilized.

The priorities have been identified; the task now is to turn them into timely decisions, adequate funding and concrete results. The credibility of European action will be measured on this capacity to execute.

The case of artificial intelligence is emblematic, and quick action is crucial in this sphere. The EU has drawn up rules for the use of models and information, a strategy for the development of the sector, and dedicated investment programmes.25 It also has a wealth of data26 and scientific expertise to leverage for developing applications and promoting their adoption. Yet the delays in implementing initiatives that are already under way risk holding progress back and widening the gap with the other large economies.27

This tardiness is compounded by a serious limitation. The European Union has abundant savings but is still unable to turn them into productive investments, especially those with greater value added and at higher risk, on which innovation, competitiveness and long-term growth depend.

As long as capital markets remain fragmented along national lines, European savings will continue to be invested elsewhere, financing growth in other economies rather than in the EU. An integrated capital market is essential for financing innovation, which requires patient investors willing to take risks over long horizons.

The savings and investment union strategy is an important step,28 but true financial integration requires a European sovereign bond: a liquid and safe asset that can provide a benchmark for markets and attract resources from abroad, thereby strengthening the international role of the euro. If it is based on an adequate common fiscal capacity, it could promote the financing of investments of European interest. This would avoid the inefficiencies of uncoordinated national initiatives, and it would also be easier to mobilize large-scale private capital.

Legal and political obstacles to integration can no longer be an excuse for inaction. The mutual distrust that had scarred Europe starting with the sovereign debt crisis was overcome during the pandemic. The challenges are no less serious today: they involve security, energy, and technology.

In exceptional times, Europe must be able to build solutions that match its economic weight and global responsibilities. It is not just the EU's competitiveness that is at stake, but also its ability to influence the balances of an increasingly unstable and fragmented world.

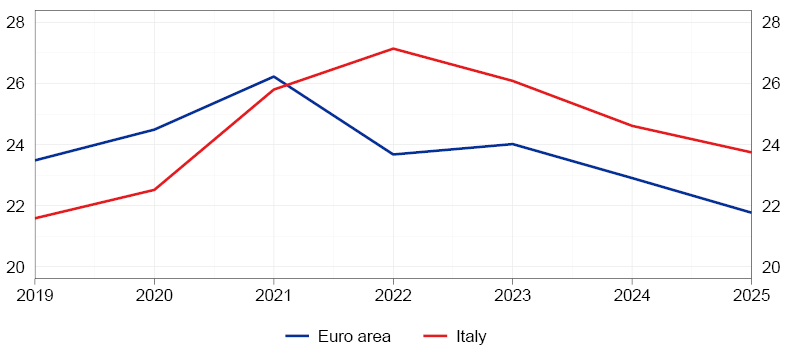

The Italian economy

The Italian economy has shown considerable resilience since 2019. Despite the pandemic and the 2022 energy shock, Italy's GDP has increased by more than 6 per cent - a result in line with the euro-area average in aggregate terms, but better on a per capita basis.

Growth has been driven by investment29 and supported by exports;30 employment has risen significantly. The net international investment position has improved too, turning positive - after having been strongly negative ten years ago - and reaching 15 per cent of GDP.

These results have been supported by the prudent management of public finances in recent years, which has bolstered investor confidence and prevented international shocks from turning into large-scale domestic crises.

More recently, however, momentum has waned, weighed down by the deterioration in the geopolitical environment, the tightening of US trade policies and the difficulties of the German economy, Italy's main export market. Domestic demand has been held back by modest growth in disposable income, reflecting the loss of purchasing power in wages.31 GDP grew by 0.5 per cent in 2025, less than the euro-area average.

The conflict in the Persian Gulf has undermined an already fragile outlook. Economic activity is projected to remain weak in the coming months; in the worst-case scenarios, it could stagnate or shrink.

Looking ahead, competitiveness could become a central issue again. Italian exporters still have limited presence in Asian markets, which are set to be the main drivers of global demand, while competition from China is increasing pressures on high-tech manufacturing sectors too. Italy retains significant strengths in mechanics, pharmaceuticals and high-quality goods production: only by investing and innovating will their potential be harnessed.

Without a marked increase in productivity, the Italian economy could remain locked into structurally modest growth rates. Output per hour worked in the non-financial private sector has only grown by 6 per cent since the turn of the century, compared with gains of between 13 and 34 per cent in the other large euro-area economies.

Demographic trends make this challenge extremely urgent. With the working-age population declining sharply, we will not be able to rely permanently on employment growth to support economic development.

In order to boost productivity, the weaknesses that have held back the Italian economy for decades must be addressed: poor innovation, low levels of human capital, and energy dependence. The investment effort of recent years must be sustained and made more effective by improving the quality of public policies.

Investment and the National Recovery and Resilience Plan32

Investment has rebounded, marking the most significant shift in recent years. It has risen not only in construction, but also in machinery and intangible assets - all essential components for growth prospects.

Public support has been substantial. Between 2021 and 2025, spending under the National Recovery and Resilience Plan (NRRP) exceeded €100 billion, accounting for 30 per cent of total capital accumulation.

Subsequent revisions have adapted the Plan to the complexity of its implementation: some projects have been scaled back or replaced by already ongoing initiatives, and some reform targets have been recalibrated. These adjustments are expected to a certain extent in a programme of this scale.

Expenditure to date has supported demand and raised GDP by almost 1 percentage point per year on average over the five-year period.33 It has strengthened digital, rail, electricity and water infrastructures.

The Plan has also affected the functioning of public administration. It has introduced procedures more geared towards achieving targets, with simplified processes and pre-allocated resources. Contracts financed under the NRRP have been awarded more frequently - by around one quarter - and more quickly than in ordinary activity, with the value of tenders relative to GDP being more than double that of the previous decade.

It is still too early to assess the impact on growth potential. This will largely depend on the ability to sustain the modernization effort over time.

A sharp slowdown in public investment at the end of the NRRP appears unlikely, thanks to the possibility of using part of the still unspent resources in the coming years and to the commitments made by the Government in the medium-term fiscal-structural plan.

Sustaining this increase in investment, however, will require a contribution from the private sector. Firms have significant own resources (Figure 5), which need to be directed towards investment in innovation.

Figure 5

Non-financial corporate saving

(percentage points)

Source: Eurostat (Non-financial accounts by institutional sector).

(1) Gross saving as a percentage of value added.

Some structural weaknesses risk holding this back: a productive system that is fragmented into small firms, which are slower to adopt new technologies; a lack of innovative firms that are able to scale up; and an insufficient propensity to invest in intangible assets - research and development, software, data and organizational capital.

Artificial intelligence: adoption challenges

Artificial intelligence can become a decisive lever to revive the productivity of the Italian economy. Its potential, however, will not be realized automatically. It will depend on the degree of uptake among firms - starting with small and medium-sized enterprises - and on the ability to integrate it into their production processes.

The share of firms using AI has increased in recent years, to 30 per cent.34 However, only around 5 per cent use it intensively. In most cases, its adoption remains confined to relatively simple applications,35 which improve individual productivity but do not fundamentally transform business processes. By international standards, the uptake of AI remains low.36

It is still early days, so there is time to avoid repeating the experience of the 1990s, when delays in the adoption of information and communication technologies built up and weighed on productivity for decades.37 Action needs to be swift now.

AI's potential contribution is significant. Labour productivity could increase by 0.2 percentage points per year under a slow-adoption scenario, and by more than 1 percentage point if AI spreads rapidly and widely.38

In the most favourable scenario, these gains could more than offset the decline in potential output caused by the contraction in the working-age population.39 Combined with higher labour force participation, this would make durable growth in the Italian economy possible.40

There are, however, significant obstacles to widespread adoption, especially for smaller firms. It involves high upfront costs and requires both technical and managerial skills to find the most suitable solutions, reorganize processes, manage legal risks and protect data confidentiality.41

Benefits increase when adoption spreads along supply chains. Individual firms, however, make decisions based on their expected returns, without fully taking into account the benefits for the whole productive system. Fragmentation in demand in turn discourages the emergence of specialized providers.

Public intervention can be decisive in overcoming these obstacles, especially in the early stages.42

Italy has significant strengths: some of the most advanced computing infrastructure in Europe, a strong scientific and academic tradition, and ample private savings. It needs a strategy to mobilize these resources, with targeted policies rather than generic subsidies.

First, technology transfer needs to be strengthened through public support structures capable of assisting firms in finding the solutions best suited to their needs. The ongoing initiatives remain fragmented and lack stable funding,43 but they can be strengthened by drawing lessons from countries that have been investing consistently in this area.44

It is also important to support the creation and growth of innovative firms, so as to turn the high-quality research conducted in Italy into products and services.45 To this end, the venture capital and private equity industries, which are capable of supporting high-risk, high-potential projects, should be strengthened.

The state can also act as a lead buyer of innovation.46 By directing public demand towards advanced applications in areas such as healthcare, energy, security and mobility,47 it can open up new markets, reduce risk for early movers and accelerate the uptake of new solutions.

The uptake of artificial intelligence in general government can also improve the efficiency and quality of public services for citizens and businesses.48

Lastly, it is essential to create conditions that support AI adoption, within a shared EU framework: facilitating access to computing infrastructure, promoting secure data sharing along value chains,49 and establishing a clear regulatory framework that protects firms and citizens without stifling experimentation.50

Promoting the use of AI calls for coordination and continuity. It does not require large amounts of public funding,51 but rather a coherent, sustainable strategy that provides firms with a stable framework for investing. As already noted, managing the effects on employment remains essential.

Training and innovation capacity

In a recent speech, I reflected on the importance of human capital for economic and social progress and for people's lives.52 Here I would like to focus on a specific point: skills are the foundation of innovation capacity. Without a skilled workforce, even the most advanced technologies yield limited benefits. What is more, innovation does not automatically reduce disparities: without widespread skills, it may increase them, rewarding those able to use it while leaving others behind.

In Italy, these risks are heightened by weaknesses in the training and effective use of human resources.

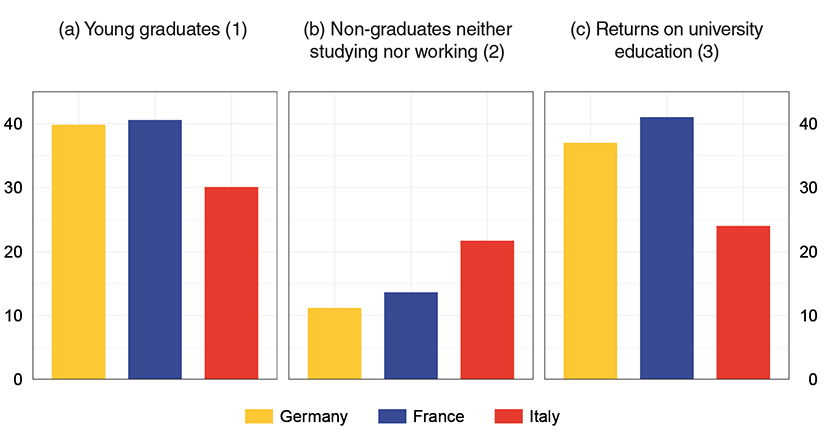

Since the beginning of the century, the share of people in their thirties with a university degree has more than doubled, to 30 per cent, but remains below that of the other major European economies (Figure 6.a). One in five young non-graduates is neither in education nor in employment - a rate twice as high as in other countries (Figure 6.b). Returns on tertiary education remain limited, while firms' demand for high-skilled workers remains weak (Figure 6.c). A rising number of young graduates move abroad in search of full recognition of their skills: more than 100,000 of them left the country between 2020 and 2024.53

Figure 6

Young graduates, NEETs and returns on university degrees

(per cent)

Sources: Based on data from Eurostat, 'Labour Force Survey' and 'European Union statistics on income and living conditions'.

(1) Percentages of graduates among the population aged 28 to 30. - (2) Percentage of non-graduates who are not in education, employment or training (NEETs) as a share of the population aged 28 to 30. - (3) Returns are calculated for individuals aged 28 to 34, accounting for gender composition.

This creates a vicious cycle. A less innovative production system generates insufficient demand for highly skilled labour and reduces incentives to invest in education; in turn, the shortage of skills makes it harder to adopt new technologies.

Breaking this cycle requires action on both sides. Skilled employment will increase if firms are incentivized to innovate and adopt new technologies. At the same time, the education system needs to be strengthened so that it can train highly qualified individuals and teach them how to work with AI. Relevant skills - such as supervisory abilities, critical judgement and the interpretation of results - are usually developed through technical and scientific studies, but also in other fields, including the humanities. Greater integration between lifelong learning and work experience will also be needed to adapt the skills of workers most exposed to the technological shock.

Over time, resources will need to be increased: in Italy, public spending on education is 1 percentage point of GDP lower than the EU average, with the gap concentrated in higher education spending.54

Energy

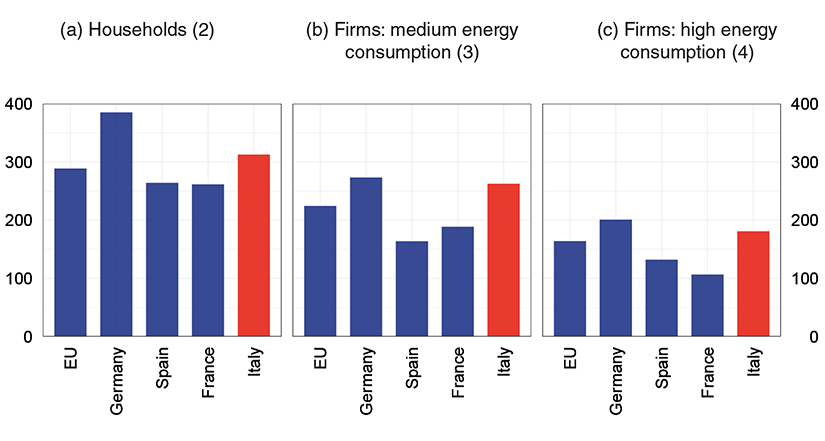

The conflict in the Persian Gulf has once again highlighted Italy's dependence on energy imports. For an economy that is particularly exposed, the recent price increases are leading to a significant transfer of wealth abroad, reducing households' disposable income (Figure 7.a), weakening firms' competitiveness (Figure 7.b and 7.c) and curbing growth.

Figure 7

Average costs of electricity purchases in 2025

(euros per megawatt-hour)

Source: Based on Eurostat data.

(1) Average of half-yearly values. - (2) Households consuming between 2,500 kWh and 4,999 kWh per year. - (3) Firms consuming between 500 MWh and 1,999 MWh per year. - (4) Firms consuming between 20,000 MWh and 69,999 MWh per year.

This dependence must be reduced by acting on three fronts: energy efficiency, the development of renewable sources and the strengthening of energy grids. Italy has made progress in each of these areas, but it must pick up the pace.

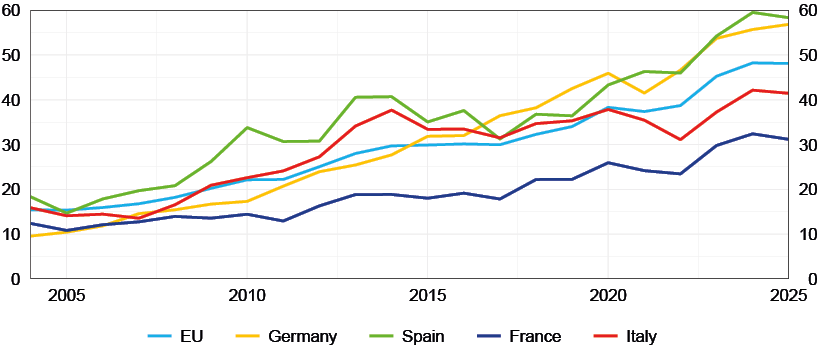

On the efficiency front, energy use per unit of GDP declined by 15 per cent between 2019 and 2024, in line with the average decrease in the EU. The share of electricity consumption from renewable sources rose from 35 to 41 per cent in 2025; in the European Union, however, this increase was greater (Figure 8).

Figure 8

Share of renewable energy sources in electricity consumption

(percentage points)

Source: Ember.

(1) Consumption is calculated as the sum of electricity production and net imports. The data for France are affected by the considerable use of nuclear energy, which covered around 80 per cent of consumption in 2025.

In terms of power grids, major investments are under way to strengthen transport and storage infrastructures, which is necessary to fully harness electricity generation from renewable sources. By 2040, domestic transport capacity is expected to increase by one and a half times, and interconnection capacity with foreign countries by 40 per cent.55 The European Commission's proposals under the Grids Package could provide a further boost.

As regards nuclear energy, the new technologies currently under development warrant careful assessment, as is also reflected in Parliament's ongoing examination of the enabling bill.56

Targeted and temporary support measures for households and firms may be necessary in critical phases to mitigate the impact of price increases, but they need to be complemented by structural measures aimed at addressing energy vulnerability. Only by accelerating the transition can we reduce dependence on external sources in a stable way and prevent new shocks from severely affecting incomes, competitiveness and growth again.

Banks and the financial system

Italian banks are facing this difficult cyclical phase from a position of strength. Profitability and capitalization are high; the price-to-book ratio is among the highest in Europe.

Progress has not, however, been even. The largest banks are performing very well, thanks to the recovery in net interest income, the growth in fees and commissions and the cost-to-income ratio being kept in check.

Profitability and operational efficiency continue to be weaker among less significant institutions. Their capital has strengthened, however, reaching 18.6 per cent of risk-weighted assets. The difficulties experienced in recent months by some small banks mainly reflect weaknesses in corporate governance and, at times, irregular practices. Banca d'Italia's interventions, in some cases joined by efforts from the banking sector itself, have made it possible to manage confined tensions in an orderly fashion, without repercussions on confidence in the system. The exit from the market of the most fragile intermediaries has helped to strengthen the sector.

The system's high capitalization has made room for new domestic and cross-border mergers and acquisitions.

Well-designed transactions can bring the structure of the Italian credit market closer to that of the other major European economies, make banks more competitive and promote more diversified revenue streams.57 Their value will depend on their ability to lead to more robust and efficient intermediaries, capable of financing the real economy and providing better quality, low-cost services to customers.

Competition must not be weakened, especially in local markets, where households and small businesses often have access to a limited number of financial institutions.

Lending to firms has picked up again in recent months, supported by lower borrowing costs. The increase was driven by lending to higher-quality firms, both large and small.

Loan growth is still subdued, reflecting above all moderate demand on the part of firms, characterized by strong profitability and by low leverage and financing needs. In the most recent surveys, covering the first quarter of this year, firms - including small ones - have not reported greater difficulty accessing credit. Banca d'Italia will continue to monitor the situation very closely: any reductions in loan supply could dampen economic activity.

Loans backed by public guarantees still account for more than one fifth of all loans to firms, triple that of the other major European economies.

Public guarantees play a critical role during crises; in ordinary circumstances, however, their extensive use may weaken loan selection and hinder the efficient allocation of resources. They should therefore be gradually restored to their intended function: correcting market failures, providing public support to deserving firms facing real difficulties in accessing funding and ensuring that the benefits are actually passed on to borrowers.58

The favourable scenario enjoyed by the credit market now risks being put to the test by the conflict in the Middle East. Heightened uncertainty and expectations of a more restrictive monetary policy could drive up borrowing costs and constrain loan supply; already in the March bank lending survey, Italian banks expected to tighten credit standards. Coupled with weakening economic activity, these factors could make repayment more difficult.

Against this background, prudence is needed. Yet prudence must not lead to an indiscriminate tightening of credit supply. Financing firms with sound investment plans helps banks safeguard asset quality, keep profitability sustainable and contribute to economic growth.

However, bank lending is not enough to finance innovation, technological investment and expansion; equity financing must also play a larger part.

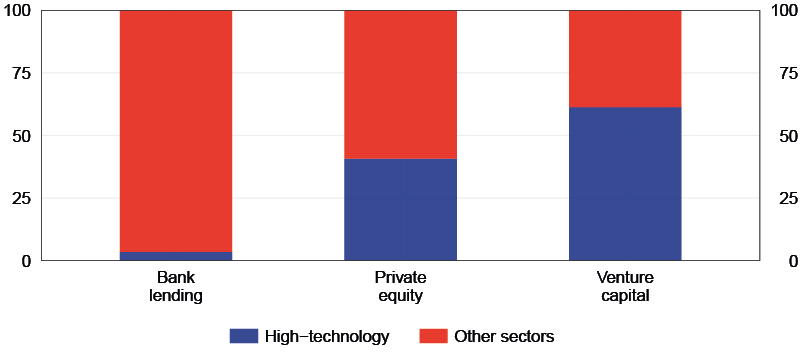

Private equity and venture capital funds could play an important role, as they focus in particular on innovative firms and high-tech sectors (Figure 9). In turn, the firms they invest in tend to innovate more and grow faster in terms of turnover, employment and productivity.59

Figure 9

Composition of financing for Italian firms by different categories of intermediary

(share of new transactions in 2023-25)

Sources: Anacredit, OECD and PitchBook.

(1) For private equity and venture capital, the analysis is based on new transactions for which the investment amount is available. The 'high-technology intensity' category includes firms operating in technology-intensive industrial sectors and knowledge-intensive technology services, which are identified according to the Eurostat-OECD classification (see OECD, ISIC Rev.3 Technology Intensity Definition, 2011). The 'other sectors' category includes medium- and low-technology manufacturing and services, mining and energy, and construction.

In Italy, however, these funds remain underdeveloped. The recent reform of the Consolidated Law on Finance includes measures to make it easier for them to operate, aligning rules and procedures with international practices. This is an important step that must now be followed up by strengthening the environment in which these intermediaries operate.

The long-standing discussion about equity capital should be revived, with action needed on several fronts: encouraging greater involvement by pension funds and insurance companies; increasing households' appetite for equity investments by lowering costs and educating consumers; and incentivizing entrepreneurs to open up to external financing.

There is no lack of analyses and proposals; 60 they must now be translated into a coherent strategy.

Technology and cyber risks

Stronger profitability enables Italian banks to scale up their investment in technology. It is not only about increasing operational efficiency: digital technologies make it possible to fine-tune credit assessment processes, customize services and reinforce customer relationships.

Expenditure by the largest Italian banking groups is comparable to that of their main European peers; small intermediaries lag behind, albeit with some notable exceptions.

Having become widespread in payment services, digitalization is now extending to other areas. A growing proportion of customers, especially younger ones, prefer services that are fast and easy to access through digital channels.

Artificial intelligence will speed up this transformation, thereby affecting how financial services are offered, how payments are made and how asset management is conducted.61

For intermediaries, the primary challenge is organizational, and not just technological. In order to reap the benefits of innovation and adapt to changing demand, they will need to invest in skills and overhaul their processes.

This transformation, however, raises new risks. Customers who are less familiar with digital applications are more exposed to financial exclusion and scams. Banca d'Italia is committed to protecting the most vulnerable groups, through alternative dispute resolution mechanisms and financial education initiatives.

Technological innovation is also changing the nature and frequency of IT and cyber risks, as well as the channels through which they are transmitted. Increasing reliance on third-party providers heightens vulnerabilities: multi-tier supply chains concentrated among a few providers can turn localized disruptions into wide-ranging ones.

Between 2023 and 2025, total ICT-related incidents involving Italian banks increased by 80 per cent compared with the previous three-year period; among them, cyber incidents doubled.62 While no significant losses were recorded, these events highlight vulnerabilities that should not be underestimated. Supervisory activities revealed shortcomings in the intermediaries' management of these risks.

Artificial intelligence adds a further layer of complexity. In recent weeks, there has been news of advanced AI models that can detect vulnerabilities in IT systems with unprecedented speed and depth. While this capability can make vulnerability patching quicker, it can also be more effectively exploited by cyber criminals, particularly where the safeguards adopted by intermediaries are inadequate.

Effective response requires action by both authorities and financial operators.

Banca d'Italia is in contact with the sector's leading global developers with the aim of properly implementing new AI models once they become publicly accessible, in order to protect its own IT systems and those of Italian intermediaries. We have recently launched a discussion with national authorities, financial operators and their IT service providers on these very topics.

More in general, we are cooperating with the European institutions to promote the swift and coordinated implementation of the DORA Regulation,63 in order to strengthen the operational and cyber resilience of the financial system.

Financial intermediaries are responsible for ensuring their systems' protection and continuity, even when they use third-party providers, with the latter sharing similar responsibilities.

The response cannot be purely technological. It requires action by executive bodies, which are called upon to establish sound governance and control frameworks, assign responsibilities clearly and draw up plans for timely intervention. At this current time of strong bank profitability, there is a need to allocate adequate resources to investment in infrastructure and human capital.

Conclusions

Eighty years ago, on 2 June, the women and men of Italy chose the Republic. They succeeded in overcoming deep divisions through discussion in the Constituent Assembly, setting in motion the building of the democratic institutions on which the reconstruction of the country would be founded.

This choice was accompanied by another equally decisive one: to position Italy in an open world order based on cooperation and shared rules.

Joining the post-war global multilateral architecture and participating as a founding member in the European project were essential conditions for the extraordinary economic development in the decades to follow.

In its Annual Report published in March 1946, Banca d'Italia - then headed by Luigi Einaudi, subsequently a member of the Constituent Assembly - set out clearly the premise of the new monetary order established at Bretton Woods: international collaboration extending to all fundamental economic relationships, inspired by a farsighted vision of the communality of interests and an awareness of how closely everyone's well-being depends on that of everyone else.64

There was more than economic analysis in those words. After the trauma of the war, there was a belief that peace and prosperity could only be founded on sound institutions, common rules, and cooperation between countries. It was a lesson born of history; it remains a guide for the present.

Today, that order is facing a profound crisis. Persistent macroeconomic imbalances, unequal distribution of the benefits of globalization, the return of protectionism, and the strategic use of economic, financial and technological resources have all weakened its foundations. Geopolitical tensions are being rapidly transmitted to the economic system and are affecting people's well-being. Global uncertainty now influences the decisions of households, firms and governments.

The answer cannot be withdrawal. Reaffirming the value of cooperation does not imply ignoring the fragilities of the previous framework, nor does it entail giving up economic security and strategic autonomy. It means preventing the pursuit of protection from turning into isolation. It means preventing interdependence from becoming a source of division rather than a driver of progress. It means preventing fragmentation from weakening the very things we want to defend: growth, stability and well-being.

In this unstable world, Europe must find its strength through greater unity. It has savings, production capacity, scientific expertise, institutions and values that are a model around the world. It has finally begun to take action, setting out its goals and priorities with clarity. It must now be quick to act, turning those goals and priorities into decisions, investments and results.

Italy must look to the future with determination. It has great strengths: cutting-edge scientific knowledge, human capital to leverage, a highly rated production system, and financially solid banks, businesses and households. This is an abundance of assets. For it to become a real advantage, it needs to be geared towards growth, income and well-being in the years ahead.

Technology will be the decisive arena for this challenge. Artificial intelligence, robotics and other innovations are reshaping production processes, work organization and the demand for skills. Sitting on the sidelines of this transformation would mean accepting a regression in the capacity to grow, just when population ageing makes it essential to increase the contribution of every worker and every firm.

Public intervention must accompany this transformation. By resolutely following a path that can steadily lighten the burden of public debt, resources will be unlocked for social spending and for growth. We must facilitate the technological leap of firms, strengthen human capital, direct savings towards productive investment, and support workers in the changes that the new economy will require.

The technological revolution will not generate shared prosperity spontaneously: it must be governed. The development of artificial intelligence must serve people and society, not the concentration of technological power. Adequate rules are needed to protect pluralism, open markets, competition and the dignity of work, and have to be agreed at global level.

The ultimate measure of success will be the ability to provide opportunities for young people. A country that innovates must be able to draw on skills, reward merit, retain and attract talent, and enable everyone to contribute according to their individual abilities. It is a matter of both efficiency and justice.

Creating the conditions for the new generations to achieve their aspirations and to contribute to Italy's progress is not just an economic responsibility: it is the civic duty of our age. Only in this way can Italy navigate an increasingly fragmented world, without succumbing to its divisions, and transform the technological transition into a time of freedom, work and confidence in the future.

Endnotes

- 1 These include US importers front-loading purchases at the beginning of 2025, ahead of the introduction of tariffs, and the unexpected expansion of goods imports linked to the development of artificial intelligence.

- 2 P.D. Fajgelbaum and A. Khandelwal, 'Tariffs in 2025: short-run impacts on the U.S. economy', NBER Working Papers, 35064, 2026.

- 3 F. Panetta, 'Trade and Finance in a Fragmented World', speech at the 32nd Assiom Forex Congress, Venice, 21 February 2026.

- 4 According to the IMF, in 2024, 40 per cent of global balances were higher than warranted by economic fundamentals and desirable policies; see the box 'Global current account imbalances: recent trends, drivers and prospects', in Chapter 1 of the Annual Report for 2025.

- 5 V. Aprigliano et al., 'China shock 2.0: structural drivers and implications for the euro area', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers), forthcoming.

- 6 B.S. Bernanke, 'The global saving glut and the U.S. current account deficit', speech at the Sandridge Lecture, Virginia Economists' Association, Richmond, 10 March 2025.

- 7 E. Letta, Much more than a market: speed, security, solidarity. Empowering the Single Market to deliver a sustainable future and prosperity for all EU citizens, April 2024; M. Draghi, The future of European competitiveness, September 2024.

- 8 IMF, World Economic Outlook. Global Economy in the Shadow of War, April 2026.

- 9 For example, unilateral interventions by surplus countries would push global real rates upwards, amplifying financial risks; see C.E. Bai, G. Gopinath, H. Rey and A. Weber, 'G7 economists memo on global imbalances', 28 March 2026.

- 10 The accord aimed to correct the overvaluation of the dollar and to ease protectionist tensions, particularly between Japan and the United States; see T. Hoshi, 'Global imbalances then and now: lessons from the Plaza Accord', in H. Rey, B. Weder di Mauro and J. Zettelmeyer (eds.), Paris Report 4: The new global imbalances, CEPR, 2026, pp. 355-366.

- 11 P.A. David, 'The dynamo and the computer: an historical perspective on the modern productivity paradox', American Economic Review Papers and Proceedings, 1990, 355-361; and T.F. Bresnahan and M. Trajtenberg, 'General purpose technologies "Engines of growth"?', Journal of Econometrics, 65, 1995, pp. 83-108.

- 12 R.X. Gao, J. Krüger, M. Merklein, H.-C. Möhring and J. Váncza, 'Artificial intelligence in manufacturing: state of the art, perspectives, and future directions', CIRP Annals - Manufacturing Technology, 73, 2024, pp. 723-749.

- 13 Artificial intelligence made it possible to reconstruct the structure of millions of proteins, an achievement rewarded with the Nobel Prize in Chemistry 2024; see A. Díaz-Holguín et al., 'AlphaFold accelerated discovery of psychotropic agonists targeting the trace amine-associated receptor 1', Science Advances, 10, 32, 2024.

- 14 F. Filippucci, P. Gal and M. Schief, 'Aggregate productivity gains from artificial intelligence: a sectoral perspective', AEA Papers and Proceedings, 116, 2026, pp. 31-35.

- 15 D. Acemoglu and P. Restrepo, 'The race between man and machine: implications of technology for growth, factor shares, and employment', American Economic Review, 108, 6, 2018, pp. 1488-1542 and D. Autor, C. Chin, A. Salomons and B. Seegmiller, 'New frontiers: the origins and content of New Work, 1940-2018', The Quarterly Journal of Economics, 139, 3, 2024, pp. 1399-1465.

- 16 We are referring to the Jevons paradox, according to which improvements in steam engine efficiency increased rather than reduced the consumption of coal, making it convenient to use it for new purposes; see W.S. Jevons, The Coal Question, London, Macmillan, 1865.

- 17 D. Autor, M.S. Kearney and L.F. Katz, 'Trends in U.S. wage inequality: revising the revisionists', The Review of Economics and Statistics, 90, 2, 2008, pp. 300-323; see also M. Goos, A. Manning and A. Salomons, 'Job polarization in Europe', American Economic Review, 99, 2, 2009, pp. 58-63.

- 18 V. Aprigliano et al., forthcoming, op. cit.

- 19 The neutral level of the interest rate is the one compatible with the absence of inflationary pressures and with the economy's potential growth. Estimates are generally around 2 per cent in nominal terms; see C. Brand, N. Lisack and F. Mazelis, 'Natural rate estimates for the euro area: insights, uncertainties and shortcomings', ECB, Economic Bulletin, 1, 2025, pp. 73-78.

- 20 The Competitiveness Compass is the strategy presented by the European Commission in January 2025 to relaunch economic growth and competitiveness in the European Union.

- 21 The Industrial Accelerator Act picks out strategic sectors in European manufacturing and envisages support measures as a European response to industrial policies in the United States and China; see European Commission, 'Proposal for a Regulation of the European Parliament and of the Council establishing a framework of measures for the acceleration of industrial capacity and decarbonisation in strategic sectors' and amending Regulations (EU) 2018/1724, (EU) 2024/1735 and (EU) 2024/3110', COM(2026) 100 final, 4 March 2026.

- 22 The proposal for the 28th Regime introduces a European corporate form to reduce the fragmentation of the single market, facilitate the raising of capital and foster the growth of innovative firms; see European Commission, 'Proposal for a Regulation of the European Parliament and of the Council on the 28th regime corporate legal framework - 'EU Inc.', COM(2026) 321 final, 18 March 2026.

- 23 The Grids Package reaffirms the importance of the strategy for cutting down the use of fossil fuels and increasing electrification; see European Commission, 'Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions. 'European Grids Package', COM(2025) 1005 final, 10 December 2025.

- 24 See the European Commission's website, Prosperity and competitiveness - Implementation tracker and Security and defence - Implementation tracker.

- 25 As well as regulating the use of artificial intelligence (AI Act), Europe has drawn up an action plan (AI Continent Action Plan) and an initiative to mobilize financial resources (InvestAI).

- 26 Europe has a large and diverse industrial system that generates a large amount of production process data over time: this is an asset that is difficult to acquire externally and that is even more difficult to replicate. These are the data needed to develop sectoral applications by adapting general-purpose models.

- 27 For example, as of mid-May, no InvestAI calls for tender had been published to fund gigafactories, although they were initially planned for the end of 2025.

- 28 For more details, see the European Commission's website, 'Savings and Investment Union. Connecting savings and productive investments' and 'Market Integration and Supervision Package'.

- 29 Investment has increased by 33.9 per cent, compared with 2.7 per cent in the euro area, 13.6 per cent in Spain, 2.8 per cent in France and -7.7 per cent in Germany.

- 30 Exports have grown by 8.8 per cent. Goods exports have increased by 7.2 per cent, against 3.2 per cent in Spain, 2.6 per cent in France and -3.5 per cent in Germany.

- 31 Compared with 2021, hourly wages have fallen by around 8 per cent in real terms. However, fiscal policy and employment growth have offset the loss of households' purchasing power; see F. Panetta, 'Investing in the Future: Youth, Innovation, and Human Capital' (only in Italian), inaugural lecture for the 2025-2026 academic year at the University of Messina, Messina, 15 January 2026.

- 32 For further details, see the boxes 'The implementation of the NRRP in its final phase' and 'The impact of the NRRP on the performance of public procurement' (only in Italian) in the Annual Report for 2025, 2026.

- 33 This estimate is in line with the government's assessment in the latest Public Finance Document.

- 34 For further details, see the Survey of Industrial and Service Firms conducted by Banca d'Italia at the beginning of 2026, and the box 'Artificial intelligence: uptake and effects on firms' in Chapter 6 of the Annual Report for 2025, 2026.

- 35 Most firms using generative AI employ it to generate text. Over half of them also use tools such as chatbots (to interact with customers or employees), AI agents, and other software for generating computer code.

- 36 According to Eurostat, 16 per cent of firms in Italy with ten or more employees used at least one AI tool in 2025, compared with 20 per cent on average in the EU and 26 per cent in Germany. The latest analyses also indicate that Italy is falling further behind.

- 37 F. Schivardi and T. Schmitz, 'The IT revolution and Southern Europe's two lost decades', Journal of the European Economic Association, 18, 5, 2020, pp. 2441-2486.

- 38 F. Bertolotti, A. Linarello and P. Zoi, 'Shock propagation and economic policies in the Italian production network', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers), forthcoming. The effects could be even greater: unlike past transformative technologies, from electricity to information technology, AI can accelerate research and development processes, including in its own field, setting self-reinforcing mechanisms in motion.

- 39 F. Panetta, 'The Governor's Concluding Remarks for 2024', 30 May 2025, in which it was estimated that without productivity gains and with employment rates remaining at their 2024 levels, GDP would decline by 11 per cent between 2024 and 2040.

- 40 'Parliamentary commission of inquiry into the economic and social effects stemming from the ongoing demographic transition', testimony by Andrea Brandolini, Deputy Director General of Economics, Statistics and Research at Banca d'Italia, Chamber of Deputies, Rome, 15 April 2025 (only in Italian).

- 41 According to Eurostat's 2025 'ICT usage and e-commerce in enterprises' survey, 10 per cent of Italian firms report not having adopted AI solutions despite having considered their use. The main obstacle indicated is a lack of skills, followed by regulatory uncertainty, poor data quality and availability, and legal risks. Similar evidence is observed in other EU countries.

- 42 L. Bellomarini et al., 'AI adoption: effects on productivity and support policies', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers), forthcoming.

- 43 M. Andini, F. D'Amuri, A. Linarello and G. Mattei (eds.), 'Competence Centres and technology transfer in Italy', in M. Andini et al., 'Research, innovation and technology transfer in Italy', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers), 954, 2025, pp. 91-106 (only in Italian).

- 44 AI Singapore's 100 Experiments programme promotes the adoption of artificial intelligence through pilot projects based on business use cases, with public co-financing. In Germany, the Fraunhofer institutes combine applied research with technology transfer; see L. Bellomarini et al., forthcoming, op. cit.

- 45 Italy ranks second in Europe in terms of high-quality publications on artificial intelligence. High-quality scientific output is defined as that included in the top decile of the distribution based on the number of citations, according to data from Scopus Custom Data and the Scimago Journal Rankings; see the OECD website, 'Science bibliometric indicators'.

- 46 In the United States, the Advanced Research Projects Agencies (ARPAs) play an important role in this area. These agencies, led by experts in the relevant technological fields, were established to promote innovation in the war industry during the Cold War. They have since expanded their scope to other areas, such as energy and the medical sciences.

- 47 Pre-commercial procurement (PCP) falls within this framework. It is a procurement procedure through which public authorities engage multiple operators in developing alternative technological solutions to meet a specific need. PCP funds and steers research and development activities, without necessarily purchasing the resulting applications. For an overview of the results of EU-funded PCPs, see the European Commission's website, 'CORDIS brings you the results of EU research and innovation'.

- 48 The 2025 Survey on the Digitalization of Local Governments, conducted by Banca d'Italia in partnership with the Presidency of the Council of Ministers and ANCI, points to a significant increase - from 2.6 per cent in 2022 to 12.8 per cent in 2024 - in the share of Italian municipalities using new digital technologies; adoption is evenly distributed across the country but concentrated among larger municipalities.

- 49 To this end, advanced solutions are needed - such as state-of-the-art encryption techniques and distributed learning models - that make it possible to use data while preserving their confidentiality; see Y. Chang, K. Zhang, J. Gong and H. Qian, 'Privacy-preserving federated learning via functional encryption, revisited', in IEEE Transactions on Information Forensics and Security, 18, 2023, pp. 1855-1869.

- 50 Without clear and stable guidance, firms may face difficulties in assessing compliance costs and legal risks, leading them to delay or scale back investment; see OECD, BCG and Insead, The adoption of artificial intelligence in firms: new evidence for policymaking, 2025, especially the paragraph on 'Uncertainties around regulatory compliance'.

- 51 In the most active countries, public funds allocated to AI development and adoption rarely exceed 0.5 per cent of GDP; see F. Fonteneau, J. Mollins, S. Marchi, L. Russo, A. Gentaz, M. Daoud and A.-A. André, 'Advancing the measurement of investments in artificial intelligence', OECD Artificial Intelligence Papers, 47, 2025.

- 52 F. Panetta, 'Investing in the Future: Youth, Innovation, and Human Capital' (only in Italian), 2026, op. cit. (only in Italian).

- 53 This figure refers to gross outflows. For further details, see Istat's website, 'Demo: demography in figures'. According to these data, the outflow of Italian graduates aged up to 34, net of return migration, was 14,000 in 2020, 8,000 in 2021, 13,000 in 2022, 19,000 in 2023 and 24,000 in 2024. In 2023, the net inflows of foreign graduates offset the net outflows of Italian graduates. The educational qualifications of immigrants are self-declared and cannot always be compared with those obtained by Italian graduates; see Istat, 2026 Annual Report. The country's situation, 2026 (only in Italian).

- 54 Italy spends roughly 4 per cent of GDP on education, compared with 5 per cent in the EU on average.

- 55 Terna, '2025 Development Plan: Overview', 2025.

- 56 Draft Law A.C. 2669, 'Delegation to the Government on sustainable nuclear energy' (submitted on 17 October 2025), Memorandum by Banca d'Italia, Chamber of Deputies, Rome, 23 February 2026.

- 57 At the end of 2025, the top five Italian groups held 68 per cent of the system's total assets, a share lower than that observed in the other main European economies, except for Germany.

- 58 Banca d'Italia recently examined the risks - legal, reputational and of ineffectiveness of the guarantees - associated with the granting of guaranteed loans by less significant banks. It has provided guidance to intermediaries and shared assessments with the competent institutions on measures that could improve how guarantees are granted.

- 59 M.G. Cassinis et al., 'Innovative firms unveiled: economic and financial insights from Italian start-ups', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers), 967, 2025.

- 60 On the role of institutional investors, see CEPR, Famiglie e risparmio: come cambiano le scelte finanziarie degli italiani, edited by L. Guiso, Bologna, Il Mulino, 2025. On how to encourage households to invest in equities, see the European Commission's webpage on 'Savings and Investment Accounts'.

- 61 OECD, Artificial Intelligence in Italian Financial Markets, 2026.

- 62 This refers to incidents involving banks, payment institutions and electronic money institutions. An increase in cyber risks is observed at global level as well.

- 63 Regulation (EU) 2022/2554 on digital operational resilience of the financial sector; for more information, see Banca d'Italia's website, 'DORA Regulation: communication to the market', 30 December 2024 (only in Italian).

- 64 Banca d'Italia, Annual Report of the Governor to the General Meeting of the Shareholders, 1945 (LII), Rome, 29 March 1946 (available on Banca d'Italia's website, Annual Report for 1945 - Abridged Version).

Instagram

Instagram