Digital Money and the Architecture of Trust

Ladies and gentlemen, dear colleagues,

It is a great pleasure to welcome you all to Banca d'Italia for this workshop on 'Digital Assets and Monetary Policy Transmission', co-organized with the European Central Bank, the Euro Area Business Cycle Network and CEPR.

I am especially pleased that we will begin with Hélène Rey's keynote on the internationalization of currencies and crypto-assets. That is an ideal starting point, because digital assets immediately raise cross-border questions: about currency competition, capital flows, and the international monetary system.

But whether money circulates domestically or internationally, one question remains fundamental: what gives it acceptance in the first place? A sixteenth-century Maltese coin bears the inscription Non aes, sed fides - not the metal, but trust.1 The history of money repeatedly teaches us that acceptance has never rested on its intrinsic value alone. Even when currencies seemed to derive their worth from precious metal, agricultural goods, or other commodities, what truly sustained their use was trust: trust in value, in convertibility, in broad acceptance, and in the institutions standing behind them.2

That lesson is even more important today. As money becomes increasingly digital - an electronic signal with no physical substance representing an entry in a database, or a token on a distributed ledger - it is tempting to focus on what new technology can enable: speed, programmability, efficiency, or new forms of settlement. But these are attributes of the payment instrument or of its underlying infrastructure, not the source of its value. What makes something money has not changed: it is accepted because it is trusted, and it is trusted because credible institutions and rules stand behind it.3

The central question, therefore, is not whether central bank digital currencies (CBDCs), stablecoins or tokenized deposits can each, individually, perform the role that traditional forms of money have historically played. The more relevant question is what kind of institutional architecture - combining different settlement assets, institutions and infrastructures - can deliver trust, resilience and effective monetary control while at the same time accompanying innovation, without hindering it.

The answer will not come from comparing instruments in isolation. It will depend on how public and private forms of money interact: on infrastructure design, interoperability, access to central bank money and services, convertibility, the legal structure of claims, and the evolving allocation of roles between banks, non-banks, payment and technology platforms, and public institutions. It will also depend on how oversight and regulation shape this interaction from the outset.4

Seven questions for the research agenda

The focus of this workshop is on one crucial question: how digital forms of money may affect monetary policy transmission. In my remarks, however, I would like to place that question within a broader analytical framework.

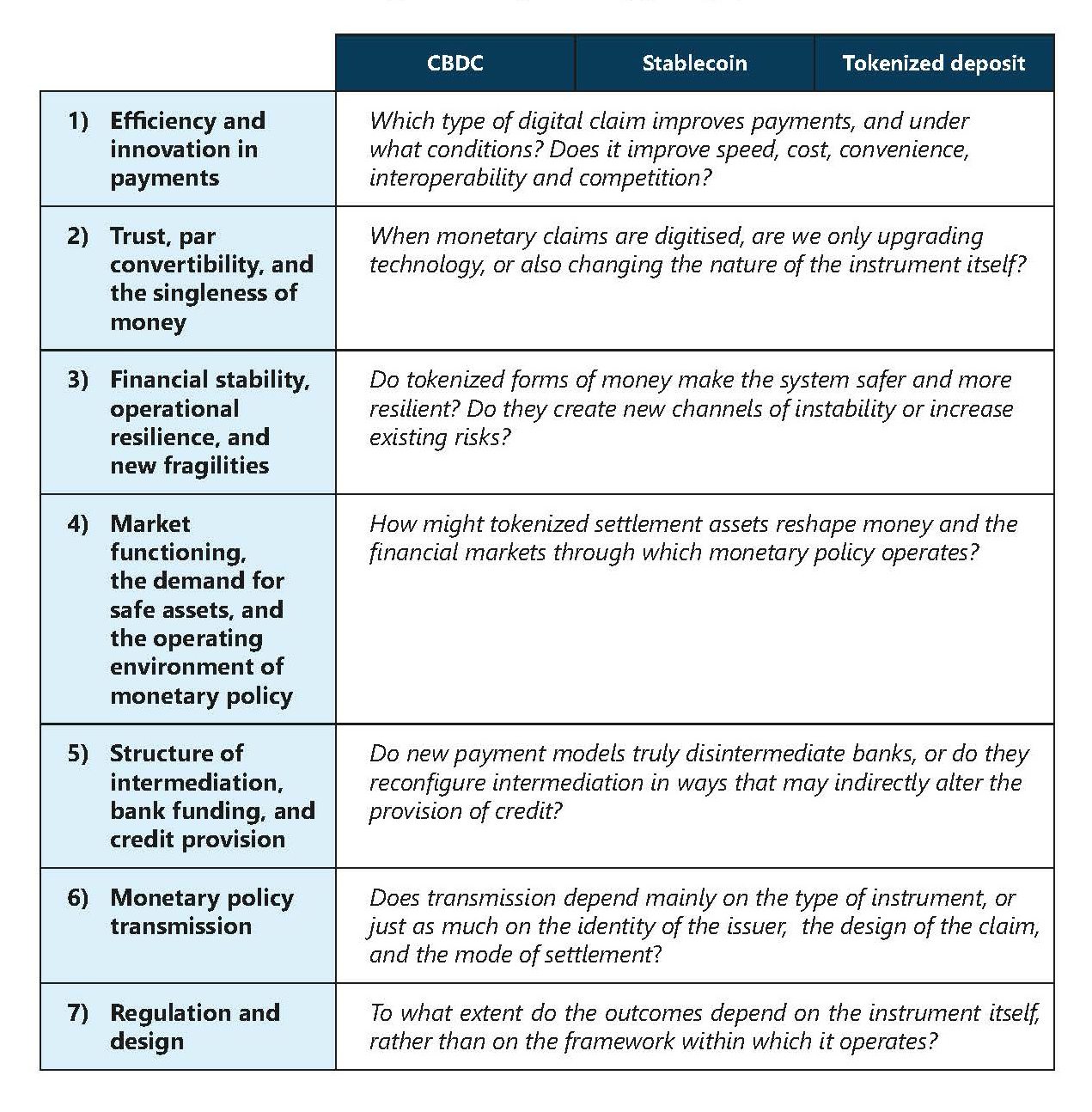

The main forms of digital money we are discussing are listed in Table 1: CBDCs, stablecoins and tokenized deposits.5 The key policy dimensions through which these forms of digital money need to be assessed are listed in the rows: efficiency and innovation, trust and convertibility, financial stability, market functioning, intermediation, monetary policy transmission, and the role of regulation and design.

What makes this framework meaningful are the underlying design features, settlement structure and institutional aspects of each instrument. From a policy perspective, the crucial design and settlement features are whether these claims are public or private, bearer or non-bearer, and whether they settle outside the central bank core infrastructure or remain anchored in central bank money.6 These features shape how they circulate, how they settle, and how they interact with the existing monetary system.

Stablecoins, for example, typically circulate as transferable private claims and settle outside the central bank core until redemption. By contrast, tokenized deposits, when properly designed, can preserve the logic of the two-tier monetary system, with transfers recorded through regulated intermediaries and settlement continuing to occur in central bank money.

This is why digital assets should not be discussed only in terms of technology - distributed ledgers, tokenization, programmability, and smart contracts. From a central bank perspective, a more fundamental issue is how these different architectures may alter the channels through which monetary policy influences financial conditions and, ultimately, the real economy.

These instruments may be important not only for payments, but also for the operating environment of monetary policy itself. They may influence bank funding structures, market liquidity, demand for safe assets, the functioning of repo and government bond markets, the distribution of reserves, the resilience of intermediation, and the transmission of policy rates to funding conditions.

It is in this spirit that I would like to organize my remarks around seven broad questions.7

1. The first question concerns efficiency and innovation in payments. This is where many discussions begin. Which type of digital claim improves payments, and under what conditions? Do CBDCs, stablecoins and tokenized deposits improve speed, cost, convenience, interoperability and competition?

DLT-based solutions may reduce frictions in cross-border payments, enable programmable and conditional settlement, and support new use cases in supply chain finance and securities markets.8 While the potential is real, current evidence suggests that the benefits will be neither automatic nor uniform. Whether they materialize depends on scale, interoperability across systems and integration with existing infrastructures.9

Efficiency gains also depend on the form of the instrument itself and the way it settles. Stablecoins may offer speed and may be readily integrated into highly composable on-chain environments, without relying on traditional interbank processes until redemption. Tokenized deposits may offer a different form of efficiency: they may extend programmability and new functionality while preserving integration with the banking system and settlement in central bank money.

The risk, however, is that innovation comes with fragmentation. Multiple non-interoperable platforms can fragment liquidity and limit scalability in ways that offset the underlying technical advantages.

Therefore, even in terms of efficiency, the issue is not purely technological. It is architectural. The key question is not whether digital instruments are more efficient in theory. It is whether, and under what conditions, network effects, interoperability and settlement design allow these gains to be realized on a large scale.

2. The second question concerns trust, par convertibility, and the singleness of money. When money is tokenized, does the instrument change, or just the plumbing?

This is not a semantic question. Traditional electronic money and bank deposits are claims on an institution, redeemable through defined channels, carrying no observable secondary-market price. By contrast, some tokenized instruments may become transferable and tradeable, and display a market price. In that case, tokenization is not merely a technical upgrade. It may alter the way trust is produced, and how it can break down.

This is precisely why the distinctions introduced earlier matter. Stablecoins typically may trade away from par and raise direct questions about convertibility and the singleness of money. Tokenized deposits need not work in the same way. They may preserve the logic of the two-tier monetary system. This does not mean that stablecoins cannot play a useful role in some settings, particularly where they address genuine frictions. But their monetary implications are not the same. Understanding precisely where and why they differ is an open research question.

The distinction between legal and effective convertibility becomes critical. Even if an instrument carries a legal right to redemption at par, it may still trade at a discount if arbitrage is imperfect, redemption is delayed or costly, or access to redemption is uneven. For an instrument to function as money, it must be accepted at par, even under stress.10

As direct liabilities of a central bank, CBDCs inherit the full institutional backing of public money. In contrast, the credibility of private instruments depends heavily on the quality of reserves, the design of redemption rights, and the effectiveness of convertibility in practice. For bank-based tokenized money, credibility continues to depend on the institutional safeguards that support deposits more broadly.11, 12

3. The third question concerns financial stability, operational resilience, and new fragilities. Do tokenized forms of money make the system safer and more resilient? Do they create new channels of instability or increase existing risks?

The answer depends heavily on design and settlement structures. Tokenization may remove old frictions, but it may also introduce new vulnerabilities. For bearer instruments, secondary market pricing can be not only a source of departure from the singleness of money, but also a channel of financial fragility.13 Small deviations from parity may in fact become immediately visible to market participants, accelerating fire-sale dynamics, even in the absence of solvency concerns.14 In this setting, the timing and design of redemption are not secondary implementation details, but central determinants of resilience.15

Where tokenized bank money remains embedded in an intermediation and settlement framework anchored in central bank money, fragility may take a different form. Operational, liquidity or concentration risks may still arise. But the market-based pressure on par value that characterizes bearer-style instruments is structurally reduced. So again, the key question is not simply whether money is tokenized, but whether the architecture amplifies price-sensitive fragility or contains it within a more robust settlement structure.

4. The fourth question concerns market functioning, the demand for safe assets, and the operating environment of monetary policy. How might tokenized settlement assets reshape money and the financial markets through which monetary policy operates?

This is a dimension sometimes underappreciated in the public debate, but highly relevant for central banks. The effects depend, once again, on design and on the reserve structure.

When reserves are invested in short-term government securities, stablecoin issuers may become significant players in those markets and in repo markets. At scale, that may affect yields, convenience premia and the availability of high-quality liquid assets.

When reserves are held as bank deposits, the effects are channelled more indirectly, through bank balance sheets and liquidity regulation. Changes in the volume and composition of deposits affect banks' demand for high-quality liquid assets under the LCR and NSFR frameworks, and therefore their behaviour in the government securities and repo markets.

When reserves are held as central bank liabilities, the effects may be felt more directly in money markets and repo markets, where those liabilities are traded. Demand for central bank reserves could become more volatile, particularly when stablecoin issuers are NBFIs. This may affect money market and repo rates and, ultimately, the transmission of monetary policy.

But the key issue goes beyond reserve composition alone. Stablecoins may reshape financial conditions partly by operating outside the traditional reserve-based financial plumbing until redemption. Tokenized deposits, by contrast, may preserve more of that plumbing, even when they introduce new forms of functionality at the user level. This raises an important point: tokenized assets may influence financial conditions not only by transmitting monetary policy, but also by reshaping the plumbing through which monetary policy operates.

Some of these effects may reinforce the intended stance of monetary policy; others may pull in the opposite direction. And some may emerge outside the traditional channels of monetary policy.16 That is why this question is not peripheral. It goes to the heart of how monetary control is exercised in a changing payments landscape.

5. The fifth question concerns the structure of intermediation, bank funding, and credit provision. Do new payment models truly disintermediate banks, or do they reconfigure intermediation in ways that may indirectly alter the provision of credit?

New payment models can unbundle functions traditionally performed by banks - deposit taking, payment processing, credit intermediation - and redistribute them across issuers, platforms and service providers. At first glance, this may suggest a process of disintermediation. But the picture is more nuanced.

In many cases, funds remain within the banking system. What changes is their composition. For instance, retail deposits may be replaced by other forms of funding that are typically more sensitive to market conditions. This shifts the focus from the size of bank balance sheets to their composition and stability. This also matters for the composition of the asset side, because the structure of liabilities affects the resilience and pricing of intermediation.

The question, therefore, is whether the redistribution of issuance, settlement, custody and liquidity-management functions across issuers, platforms and service providers improves efficiency while preserving accountability, resilience and policy traction. That remains an open question - and one this research agenda needs to address directly.

6. The sixth question, and for today perhaps the central one, concerns monetary policy transmission, in the narrow sense. Does transmission depend mainly on the type of instrument, or just as much on the identity of the issuer, the design of the claim, and the mode of settlement?

The identity of the issuer matters. When non-bank stablecoins expand, banks may replace retail deposits with funding that is not only treated as less stable under existing regulation, but also as more sensitive to policy rates. As a result, some transmission channels may strengthen; others may weaken.17 When banks issue non-remunerated stablecoins directly on their own balance sheets, the same channels may be affected differently. For CBDCs, the effects depend critically on design choices (such as holding limits, remuneration and access conditions), which determine the extent of deposit substitution and whether the central bank balance sheet expands to accommodate it.18, 19, 20

However, the mode of settlement may be just as important. Instruments that circulate outside the central bank core until redemption may affect transmission differently from those that remain embedded in settlement in central bank money.

Tokenized deposits are a case in point. As they remain within the perimeter of the two-tier system, are settled in central bank money and are issued by regulated intermediaries, they behave much more like an extension of traditional deposits than like stablecoins. This does not mean that they are neutral. Their transferability and use across new platforms may make bank funding easier to move and potentially more responsive to changes in policy rates.

In all these cases, the effect on transmission is not determined by tokenization alone. Rather, it is determined by the combination of issuer, design, and settlement architecture.

7. The seventh and final question concerns regulation and design: to what extent do the outcomes depend on the instrument itself, rather than on the framework within which it operates?

By this point, it is clear that a great deal depends on design. The advantages and risks associated with tokenized settlement assets depend on issuer type, reserve composition, redemption rules, settlement functionalities, legal claim structure, transferability, prudential treatment and the availability of public backstops.

In this context, regulation is part of the architecture that shapes innovation from the outset. Good design and good regulation do not merely constrain outcomes; they help determine them. They influence whether a tokenized instrument behaves as a modernized form of money embedded within a resilient settlement framework or as a bearer claim whose market price, under certain circumstances, may itself become a channel of fragility. They shape whether innovation leads to greater efficiency and coherence or to fragmentation and instability. And they also determine whether new digital forms of money support or undermine the singleness of money and the effectiveness of monetary policy.

Conclusion

To conclude, it is worth asking what the implications for policymakers are.

Much remains uncertain. Nevertheless, the framework is already taking shape, and choices made now could be hard to change later.

The recent Eurosystem payments strategy21 reflects this. On the retail side, the digital euro is the area where analytical work is most advanced. Its implications have been thoroughly examined across the dimensions relevant to public policy, such as monetary policy, financial stability, intermediation, payments efficiency, privacy, inclusion and the coexistence with private solutions. This is not yet the case for other instruments. While stablecoins and tokenized deposits may address genuine needs, their broader monetary implications are less clear. On the wholesale side, Pontes and Appia22 are important as both prepare the system for a world in which tokenization may become more prevalent, while preserving flexibility vis-à-vis how technology, use cases, and private initiatives will actually evolve. In all settings, central bank money remains the common reference point for settlement, convertibility and singleness.

In Europe, there may be value in thinking about a complementary strategy. With tokenization becoming more relevant, attention should turn not only to new instruments, but also to how Europe's existing payment arrangements could evolve in that direction. From this perspective, a tokenized extension of SEPA could become an important area for reflection, building on a distinctive European asset: a common payments framework with scale, shared standards and an established degree of interoperability. It could also offer a practical way of adapting the logic of the two-tier monetary system to new technological environments.23

While history does not tell us exactly what the future of money will look like, it does teach us one enduring lesson: money may change form, but it always depends on trust. Therefore, the real question is not which instrument should prevail in the abstract. Rather, it is what combination of public money, private innovation and institutional safeguards can best support efficiency without sacrificing trust, resilience and monetary control.

This is the question before us today. I hope that the papers and discussions at this conference will help to clarify this further. Thank you very much, and I wish you a stimulating and productive workshop.

References

Ahmed, R. and Aldasoro, I. (2025), "Stablecoins and safe asset prices", BIS Working Paper No. 1270, Workshop paper.

Altavilla, C., Boucinha, M., Burlon, L., Adalid, R., Fortes, R., and Maruhn, F. (2026), "Stablecoins and monetary policy transmission", ECB Working Paper No. 3199, Workshop paper.

Angelini, P., (2026), "DLT and stablecoins: where do we stand?", International Economic Symposium co-hosted by Banca d'Italia and NABE, Rome, 20 April 2026.

Assenmacher, K., Ferrari Minesso, M., Mehl, A., and Pagliari, M.S. (2026), "Exchange rate overshooting revisited: central bank digital currency in transition", ECB/DNB, Workshop paper.

Barbon, A., Barthélemy, J., and Nguyen, B. (2026), "DeFi-ying the Fed? Monetary Policy Transmission to Stablecoin Rates", Workshop paper.

Benigno, P. (2026), "Stablecoins and Central Bank Digital Currencies: Who Supplies Liquidity?", University of Bern/LUISS/CEPR, Workshop paper.

Bidder, R. (2026), "Money and Payments Infrastructure: Understanding the Plumbing.", Signed Article, Quarterly Bulletin Vol. 2026 No. 2. Central Bank of Ireland.

Bindseil, U., Coste, C.-E., and Pantelopoulos, G. (2025), "Digital Money and Finance: A Critical Review of Terminology.", ECB Working Paper No. 3022. European Central Bank.

Branzoli, N., Moracci, E., Padellini, T., and Pietrosanti, S. (2026), "A dynamic model of CBDC holdings and transactional use", Banca d'Italia, Workshop paper.

Cerutti, E., Firat, M., Hengge, M., and Sagawa, T. (2026), "Stablecoin Shocks", IMF Working Paper, Workshop paper.

Cipollone, P. (2025), "Preparing the future of payments and money: the role of research and innovation", Bocconi/CEPR/ECB conference, 26th September, keynote speech.

Cipollone, P. (2026), "Building the rails for Europe's tokenised financial markets", Building Europe's Integrated Digital Asset Ecosystem: From Vision to Implementation", House of the Euro, Brussels, 23rd March, keynote speech.

Dornbusch (1976), "Expectations and Exchange Rate Dynamics", Journal of Political Economy, Vol. 84, No. 6

European Banking Authority (2024), "Report on Tokenised Deposits.", EBA, December 2024.

ECB (2026), "The Eurosystem's Comprehensive Payments Strategy", 31st March 2026.

Garratt, R. and Shin, H. S. (2023), "Stablecoins versus Tokenised Deposits: Implications for the Singleness of Money.", Bank for International Settlements, Bulletin No. 73.

Giannini, C., (2011), "The Age of Central Banks.", Edward Elgar Publishing.

Hristov, N., Kolb, B., and Menno, D. (2026), "Stablecoins and Financial Panics", Deutsche Bundesbank, Workshop paper.

KPMG (2024), "Tokenisation: Taking Stock of Developments.", KPMG LLP.

Panetta, F. (2020), "The two sides of the (stable)coin", ECB Frankfurt am Main, 4th November, speech.

Panetta, F. (2022), "Public money for the digital era: towards a digital euro.", National College of Ireland, 16th May, ECB, keynote speech.

Panetta, F. (2023), "Paradise lost? How crypto failed to deliver on its promises and what to do about it", remarks at the BIS Annual Conference, Basel, June.

Panetta, F. (2025), "The struggle to reshape the international monetary system: slow- and fast-moving processes", Whitaker Lecture, Central Bank of Ireland, 9th December, Banca d'Italia.

Scotti, C. (2024), "Digital euro: one for all and all for one", speech, Banca d'Italia.

Scotti, C. (2026), "Sostenere l'innovazione per innovare la finanza", speech, Banca d'Italia.

Simmel, G., (1900), "The Philosophy of Money", third edition, Routledge, 2004.

Townsend, R., M., (2021), "Distributed Ledgers: Design and Regulation of Financial Infrastructure and Payment Systems", MIT Press.

UK Finance (2025), "Reflecting on 2025: Tokenised Deposits and the Future of Payments". UK Finance, December 2025.

Tables and Figures

Table 1

Digital money and key policy questions

Endnotes

- * I would like to thank Claudia Biancotti, Giuseppe Ferrero and Giorgio Merlonghi for their assistance in preparing this text.

- 1 Inscription on the Maltese pataca, a fiduciary copper coin minted by the Order of St John following the Great Siege of Malta of 1565, to pay the labourers building the new city of Valletta. The inscription is discussed by Georg Simmel, who writes that it 'indicates very appropriately the element of trust without which even a coin of full value cannot perform its function in most cases' and that what is ultimately indispensable in any monetary transaction is 'non aes, sed fides - the confidence in the ability of an economic community to ensure that the value given in exchange for an interim value, a coin, will be replaced without loss.' Simmel (1900).

- 2 In the digital domain, preserving trust also means ensuring that people can use payment instruments safely - protected against fraud, cyber theft and unwarranted intrusions into privacy. These are not secondary concerns, since they shape user's confidence in the usability, safety and reliability of the payment instrument itself, even if they are not addressed here.

- 3 As Giannini (2011) puts it, the technology embedded in any payment system is 'largely of a social character, given the role that trust plays in it' - and whether its evolution serves the collective interest or not 'will depend on the solidity of the institutional environment, in its legal and political components.' The spread of any payment technology is therefore conditional on the existence of institutions and rules that sustain the confidence of its users; and the history of central banking is, in his reading, nothing but 'an aspect of the institutional adjustment process set in motion by the development of payment technologies.'

- 4 Townsend's (2021) central argument is that regulation and market structure 'need to be part of the overall ex ante design' of financial systems. The goal, in Townsend's framework, is to provide blueprints for the optimal design and regulation of financial infrastructure, covering not only the endpoints of centralised versus decentralized systems but also the hybrid forms in between.

- 5 The term 'tokenized deposits' is used here broadly, encompassing both bearer and non-bearer forms, whether recorded on a bank's traditional ledger or natively on-chain - the latter sometimes is referred to as 'deposit tokens.' Unlike stablecoins, which are subject to regulatory frameworks in several jurisdictions, neither term carries a consolidated regulatory definition. The EBA (2024) acknowledges the ambiguity, and Bindseil, Coste and Pantelopoulos (ECB Working Paper No. 3022, 2025) note more broadly that 'inconsistent and misleading terminology is a serious issue' in digital finance. Where reference is made to a specific design, this will be indicated explicitly in the text.

- 6 Garratt and Shin (2023) develop this distinction by contrasting two models of private tokenized money: a digital bearer instrument model, exemplified by stablecoins, in which tokens circulate as transferable claims and settle outside the central bank core - and may therefore trade away from par - and a tokenized deposit model, in which transfers are effected through regulated intermediaries with concurrent settlement in central bank money, structurally preserving the singleness of money. In their framework, the bearer/non-bearer distinction maps directly onto the stablecoin/tokenized deposit distinction. The FSB (2024) explicitly acknowledges that tokenized deposits 'could be developed as non-bearer instruments' but that, if 'designed as a transferable claim (i.e. akin to a bearer instrument)', the token may circulate without the issuer's knowledge or control, with implications for the singleness of money. The EBA (2024) similarly recognizes that a bearer model 'may also be contemplated', and the Eurosystem's Comprehensive Payments Strategy (ECB, 2026) implicitly confirms the point by referring specifically to 'non-bearer tokenised deposits' as a distinct category.

- 7 These seven questions are, of course, not intended to be exhaustive. They are meant rather to highlight a set of dimensions that appear particularly relevant for assessing the monetary and policy implications of digital forms of money. Nor do they address in any depth the issue of infrastructure costs, which may prove important in shaping scalability, market structure and adoption dynamics. Where such costs are large or highly concentrated, they may also raise questions about coordination failures, common standards and the possible role of public intervention. See also Scotti (2026).

- 8 Angelini (2026) offers a concrete illustration of this point: while many initiatives remain at the pilot stage, others have moved into production - most clearly stablecoins, but also tokenized deposits and DLT-based collateral management.

- 9 Panetta (2025) offers a clear characterization of the dual nature of DLT and tokenization: they are reshaping money and payments, bringing greater efficiency - by integrating messaging, clearing and settlement within a single architecture and sharply reducing the need for reconciliation - but also novel risks, including new forms of operational failures, cyber threats and digitally amplified financial instability.

- 10 Panetta (2020) presents an early analysis of the risks to par acceptance and monetary singleness posed by stablecoins. See also Panetta (2022) and Scotti (2024).

- 11 Benigno (2026) develops a monetary framework in which central bank liabilities and stablecoins jointly provide liquidity services and shows that the wedge between the market nominal rate and administered remuneration on reserves and tokens makes the supply of public liquidity an independent policy instrument. Full liquidity satiation is a knife-edge outcome that fails under balance-sheet risk and intermediation frictions; an intermediate regime with a small central bank balance sheet and an elastic backstop stabilises both liquidity premia and inflation.

- 12 Panetta (2025) observes that, in a two-tier monetary system, public and private money are fully interchangeable at par - but stablecoins may break this parity. If such instruments were to scale globally, these deviations would in effect create exchange rates between competing private monies, fragmenting the monetary environment and undermining the smooth functioning of payments.

- 13 Ma, Zeng and Zhang (2024) show that when only a limited number of authorised agents are permitted to interact with the issuer in primary markets - creating and redeeming stablecoins for cash - while the vast majority of investors can only trade at secondary market prices, a fundamental trade-off emerges: more efficient arbitrage improves secondary market price stability, but amplifies run risk by reducing investors' price impact from selling - lowering strategic substitutability and making panic selling more likely.

- 14 Panetta (2020) makes the case that stablecoins are vulnerable to runs and 'the need to cover redemptions could force the stablecoin issuer to liquidate assets, generating contagion effects throughout the entire financial system.' Panetta (2025) describes the mechanism: in a stress episode, large redemption demands could force stablecoin issuers into abrupt asset sales; if many holders act at once, this could trigger fire sales - and with instant settlement, global access and coordination amplified by social media - these dynamics could unfold far faster than in traditional finance.

- 15 Hristov et al. (2026) employs a medium-scale New Keynesian model with endogenous system-wide bank runs to study how a growing stablecoin sector affects financial stability, showing that bank runs and stablecoin runs may interact - with non-trivial consequences for financial stability and monetary policy transmission both in normal and crisis times.

- 16 Cerutti et al. (2026) construct novel high-frequency measures of stablecoin demand shocks from a daily narrative dataset of USDC/USDT-specific news and uses heteroskedasticity-based identification within event-study and SVAR-IV frameworks to estimate causal effects. A 1 per cent increase in the combined USDC and USDT market capitalization causes a persistent decline of approximately 1.9 basis points in the 1-month US Treasury yield, with effects concentrated at the short end of the yield curve and consistent with stablecoin issuers' reserve composition (as of end-2025, 62 per cent of Tether's reserves and 35 per cent of USDC's were held in short-term Treasuries). Ahmed and Aldasoro (2025) use daily data from 2021 to 2025 and an instrumental variable strategy based on idiosyncratic crypto market shocks and show that a 2-standard deviation inflow into dollar-backed stablecoins lowers 3-month US Treasury yields by 2-2.5 basis points within 10 days, with effects concentrated at the short end of the yield curve and asymmetric - i.e. outflows raise yields by two to three times as much as inflows lower them.

- 17 Altavilla et al. (2026) use confidential granular data on euro area banks and a Bayesian VAR identified with Google Trends attention shifts; the paper documents a deposit-substitution mechanism whereby stablecoin adoption erodes retail funding and increases banks' reliance on wholesale deposits. This structural shift strengthens the bank lending channel while weakening the deposit channel, and increases uncertainty around the pass-through of policy rates to lending volumes.

- 18 Branzoli et al. (2026) develop an inventory model of cash management and payment choice augmented with a CBDC, calibrated on ECB SPACE survey data. It shows that CBDC holdings and transactional use are highly sensitive to design choices - especially the opportunity cost of holding CBDC, the cost per transaction, acceptance rates, and the availability of reverse waterfall functionalities - and that these design parameters have first-order implications for the displacement of cash and the interaction with the monetary policy transmission mechanism.

- 19 Assenmacher et al. (2026) develop a two-country DSGE model with financial frictions to study the transition to a steady state with CBDC. In the steady state, CBDC unambiguously improves welfare without disintermediating the banking sector - banks endogenously raise deposit rates to attract savers. But macroeconomic volatility increases significantly in the transition, driven by exchange rate overshooting reminiscent of the Dornbusch (1976) mechanism: CBDC introduction generates a new 'super-charged' uncovered interest parity condition that amplifies exchange rate movements. The model finds that holding limits set at around 50 per cent of steady state CBDC demand are optimal for managing excess demand in the transition, reducing disintermediation and output losses while preserving the long-run welfare gains.

- 20 Another important distinction is between transmission through traditional finance and DeFi protocols. In a world where a significant share of financial intermediation migrates onto distributed ledger infrastructure, monetary policy would encounter a lending channel governed not by banks but by algorithmic protocols - where rates are determined by supply and demand dynamics hardcoded in smart contracts. Barbon et al. (2026) document a substantial and persistent disconnect between policy rates and stablecoin lending rates in DeFi platforms, driven primarily by crypto-specific demand shocks - in particular surges in leverage demand that push rates sharply upward while supply adjusts sluggishly - with monetary policy accounting for only a small fraction of rate variance, and its passthrough being partial, delayed, and state-dependent. The authors note that this disconnect may narrow as tokenization of real-world assets lowers the friction cost of earning risk-free yields on-chain, increasing the elasticity of DeFi supply to conventional rates and potentially integrating DeFi more fully into the monetary policy transmission network.

- 21 European Central Bank, The Eurosystem's payments strategy.

- 22 See Pontes & Appia - Eurosystem strategy for a competitive and integrated tokenised financial ecosystem in Europe.

- 23 See Single Euro Payments Area (SEPA).

Instagram

Instagram