The economic and financial system amidst uncertainty and innovation

1. The international economy

The global economy is in a period of transition, shaped by two opposing forces. The first is the shock triggered by the conflict in the Middle East, which has led to higher energy prices, heightened uncertainty and renewed concerns about supply chain bottlenecks. The second is the spread of artificial intelligence, which is bolstering investment, trade in high-tech goods and services, equity market valuations and, through the latter, household wealth and consumption.

These two forces are playing out differently across the world. The United States benefits from its lower exposure to energy shocks and from its strong capacity to develop and deploy new technologies. In China, growth is supported by manufacturing and technology exports but remains constrained by the country's reliance on imported energy.

In the euro area, higher energy costs have compounded a situation already marked by low growth. Diversification of energy sources and suppliers has made the euro area less vulnerable than in the past, but sudden increases in gas and oil prices continue to weigh on economies that still depend on imports of fossil fuels. The contribution of artificial intelligence to investment is more limited than elsewhere.

In the months following the outbreak of the conflict, household confidence deteriorated and the outlook for service firms weakened. Inflation is currently hovering around 3 per cent and is expected to remain above that level until early 2027.

Following the easing of tensions in recent weeks, the resumption of hostilities in the past few days has been accompanied by further increases in oil and gas prices, confirming the fragility of the macroeconomic outlook.

Monetary policy must once again strike a delicate balance, as economic activity slows and inflation remains above the 2 per cent target. The 25-basis-point increase in interest rates decided by the ECB Governing Council at its June meeting was an initial and measured response to the predominance of upside risks to inflation.

When considering future decisions, the ECB Governing Council will carefully assess conditions in energy markets, and the evolution of the economic situation, of wages and of prices for goods and services. The objective is to keep inflation expectations firmly anchored, limiting the indirect and second-round effects of shocks.

2. International financial markets

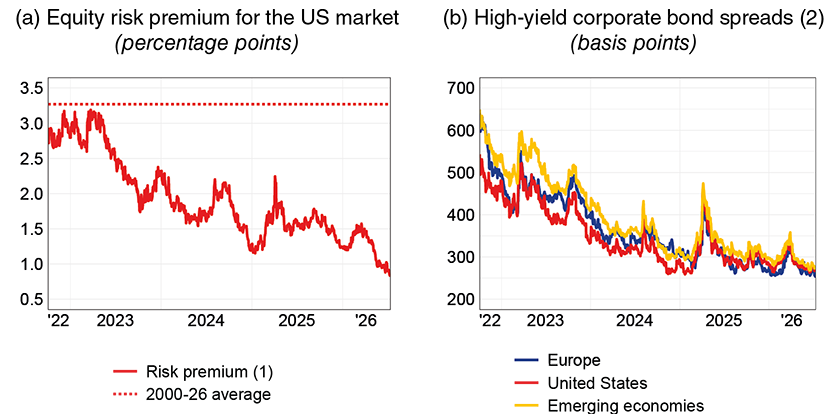

The start of the conflict between the United States and Iran at the end of last February triggered widespread tensions on the international financial markets. There was an increase in volatility and in investors' risk aversion; equity prices fell, risk premiums rose and there were capital outflows from emerging markets. Higher energy prices fuelled inflation expectations and led to a revision of monetary policy expectations, contributing to the marked rise in interest rates at various maturities.

Tensions then abated as the prospect of a ceasefire emerged. Equity markets began to rise as early as April, reaching new peaks in some sectors. Risk premiums on shares and spreads on high-yield corporate bonds decreased again (Figure 1). Government bond yields also went down, though they remain above pre-conflict levels, especially in countries with weaker public finances.

Figure 1

Equity risk premiums and corporate bond yield spreads

Sources: Based on Bloomberg and London Stock Exchange Group (LSEG) data.

(1) The premium is calculated using the ratio of the 10-year moving average of the earnings of the companies listed in the S&P 500 to the value of the index. From the resulting ratio, which is an estimate of the expected real return on equity, we subtract the real interest rate, i.e. the difference between the 10-year overnight indexed swap (OIS) rate and the inflation swap rate. − (2) Option-adjusted spreads on high-yield corporate bonds.

The speed of the recovery in the markets requires a cautious interpretation. It may indicate confidence in the capacity of the global economy to absorb tensions, but it may also point to an underestimation of risks.

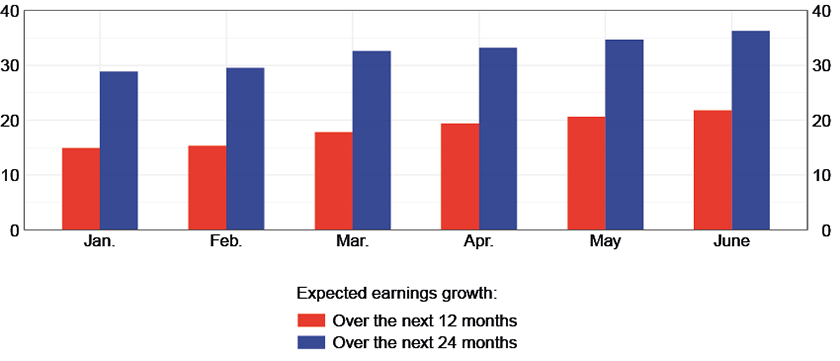

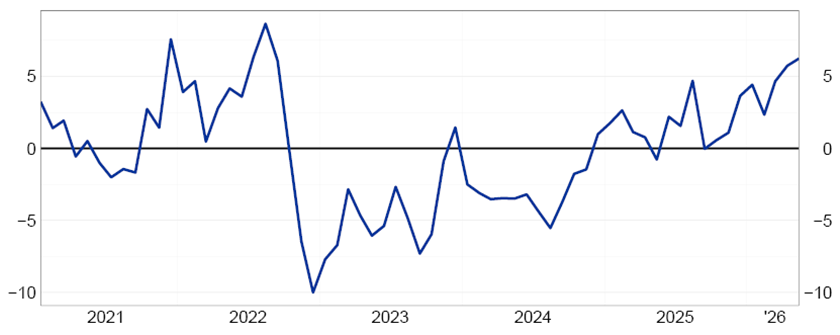

This second reading is confirmed by several indicators. The rise in equity prices has been accompanied by an increase in interest rates, a combination that reflects both very favourable expectations for future earnings growth (Figure 2), and the compression of risk premiums, to twenty-year lows. The recent experience of some speculative assets, such as crypto-assets, also reminds us how underestimating risks can support prices for a long time, before making way for broad corrections.1

Figure 2

Expected earnings growth for the US equity market

(percentage points)

Source: LSEG I/B/E/S.

Overall, the risks linked to higher energy prices, tighter financial conditions and persistent geopolitical uncertainty appear to be only partially incorporated into market evaluations.

In the foreign exchange market, the US dollar has resumed its safe-haven function. This marks a reversal from the spring of last year, when the announcement of the new tariffs had raised concerns, mainly over the outlook for the US economy, thus cooling the demand for dollar-denominated assets. This time, the use of the US dollar for oil trade invoicing2 and the position of the United States as a net oil exporter have instead fostered the appreciation of the dollar.

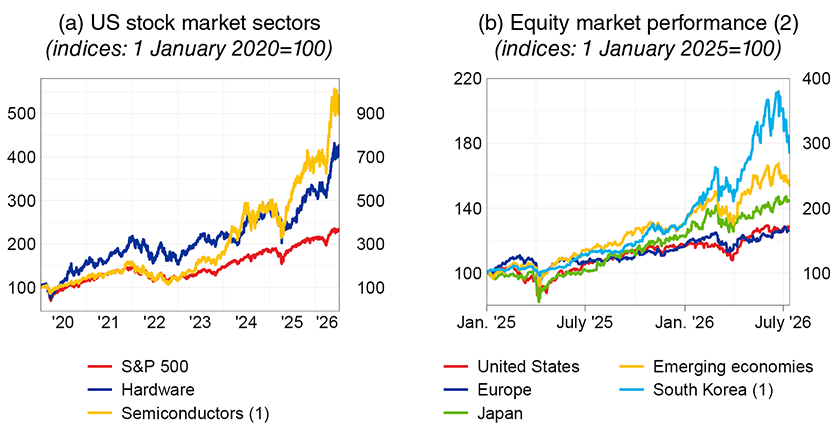

The recovery in equity prices has been driven by optimism over the prospects opened up by artificial intelligence. Demand for AI-related services has continued to expand rapidly, prompting big tech companies to accelerate investment in IT infrastructures. This has caused bottlenecks in the advanced semiconductors sector, which are essential for running data centres: prices have gone up, producers' margins have reached exceptional levels and their stock prices have risen considerably (Figure 3.a).

Figure 3

Equity markets

Source: Bloomberg.

(1) Right-hand scale. - (2) Indices: S&P 500 for the United States, STOXX Europe 600 for Europe, Topix for Japan, MSCI Emerging Markets for the emerging markets and KOSPI for South Korea.

The boost that this sector has given to the stock market indices has been stronger in the United States and, above all, in some Asian economies, where the semiconductor sector is more heavily represented in the overall stock index. In Europe, where it makes up a smaller share, the performance of the markets has been less bright (Figure 3.b), and has mainly reflected the increases in the financial and energy sectors.

Artificial intelligence is bound to have considerable effects on productivity and growth. However, the benefits are still uncertain in terms of timeframes and distribution.

The equity prices of some semiconductor firms seem to reflect the assumption that the current exceptional margins will last for a long time, but an increase in supply due to production capacity, the entry of new competitors or alternative technological solutions could lead to a downward revision of profitability expectations.3

The risks of greater competition also relate to US firms that provide AI services: the market entry of new operators and the spread of less costly models could dampen earnings expectations. At the same time, massive investment in IT infrastructure and computing capacity is increasing the financing needs of these firms. Many have upped their recourse to the bond market, while others have raised funds through capital increases or stock market public listings. For the former, greater indebtedness increases vulnerability to tighter financial conditions and potential downward revisions of expected earnings.

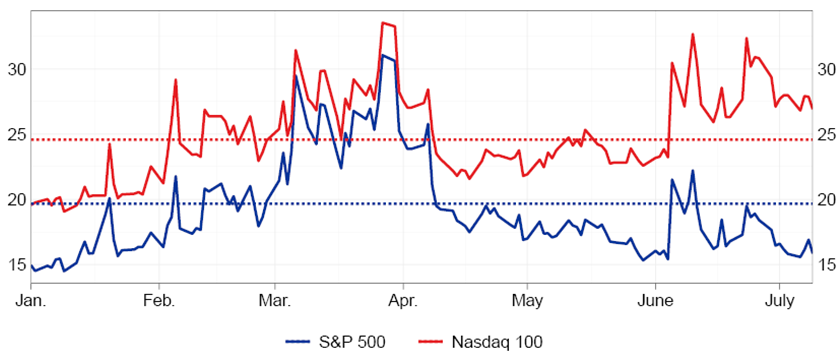

Market resilience is a positive signal, but it is not to be confused with an absence of risks. High valuations, increases concentrated in a few segments and persistent geopolitical uncertainty all expose markets to corrections that can also be sudden. The volatility of Nasdaq - in which technology companies account for a large share - remains high, although that of the broader market indices has stayed low (Figure 4).4

Figure 4

Implied volatility of equity indices

(annualized percentages)

Source: Bloomberg.

(1) The dashed lines show the historical averages over the 2001-26 period.

For investors, prudent management of exposures is necessary, especially in sectors where optimism is more intense and prices incorporate particularly high earnings expectations.

3. Banks

The banking system continues to play a central role in financing the Italian economy. The importance of bank lending has decreased over time, but it remains greater than in the other major European countries, especially for firms. In Italy, firms' bank debts account for 14 per cent of the sum of financial debt and equity, and 46 per cent of financial debt alone.

Such centrality comes with great responsibility. In a world of heightened uncertainty and recurrent geopolitical shocks, where instability can swiftly pass through to capital markets and the real economy, banks are called upon to strike a delicate yet essential balance between meeting the financing needs of households and firms with adequate credit ratings and preserving their asset quality and soundness.

The surge in energy prices has increased the liquidity needs of firms, in many cases resulting in higher demand for loans, especially short-term ones. So far, banks have met this demand. In May, the growth in lending to firms accelerated to 6.2 per cent on an annualized quarterly basis, from 2.3 per cent in February (Figure 5).

Figure 5

Loans to non-financial corporations in Italy

(annualized 3-month percentage changes)

Source: Based on Banca d'Italia data.

(1) Includes bad debts, repos and loans not reported in banks' balance sheets because they have been securitized. The percentage changes are net of reclassifications, exchange rate variations, value adjustments, and other variations not due to transactions. Data are seasonally adjusted following a methodology compliant with the guidelines of the European Statistical System.

In the coming months, credit dynamics will be shaped by the trajectory of the conflict in the Middle East, financial market conditions and banks' risk perception. A prolonged period of hostilities, coupled with renewed pressures on energy markets, could lead banks to be more cautious and to tighten their credit standards.

The indicators for the first quarter confirm that the Italian banking system is robust: profitability remains high, capitalization is more than adequate and asset quality is very good. This assessment is shared by market participants and international institutions. In its recently concluded Financial Sector Assessment Program, the IMF gave a positive evaluation of Italy's financial system, also acknowledging the contribution of effective supervision.5

The most noticeable improvement has been in terms of credit quality. Ten years ago, non-performing loans exceeded 8 per cent of total loans, one of the highest shares in the euro area. Today they account for 1 per cent.6

The balance sheet valuations of these loans remain prudent. This is partly due to EU rules requiring full provisioning for non-performing exposures originated since 2019 within specified timeframes under a calendar-based approach. For Italian banks, this system is burdensome, given the lengthy duration of civil court proceedings.7

Some differences remain with regard to non-performing loans granted by smaller banks before 2019, which are not subject to the more stringent criteria applied by the ECB to larger banks. In recent months, Banca d'Italia has started to collect updated data and announced its intention to extend the EU's approach to the rest of the Italian banking system, proceeding gradually and taking into account the specificities of individual institutions.8 The gap with larger banks has nonetheless already narrowed significantly.

The overall picture is sound, though there have been crisis episodes - albeit limited - involving small banks. Not all business ventures will prove successful in a market economy. Banca d'Italia works to prevent crises wherever possible and, when they do occur, to manage them so as to protect bank customers and financial stability.

Some of these episodes were associated with unlawful conduct, confirming the importance of robust corporate governance and strong business ethics.

This recommendation is far from abstract: it is a matter of integrity in corporate decision-making, transparency in customer relationships, awareness of the risks undertaken, and full accountability of corporate bodies and functions and of shareholders. Supervision can reduce risks, but it cannot replace corporate bodies; nor does it have - and rightly so - the powers entrusted to the judicial authorities, with which it works closely. The first line of defence remains the financial intermediaries themselves. Even more than supervisory action, it is their integrity that underpins the trust upon which banking ultimately rests.

Another development that is bound to affect the financial system is the ongoing process of consolidation. The mergers that have been recently launched or announced involve banks, insurers and asset managers, in a market in which the lines between the various sectors of finance are becoming less clear and competition is centred around the ability to offer bundled products.

This process can strengthen individual institutions and the system as a whole, encouraging investment in technology and cybersecurity, and improving the efficiency and quality of services for households and firms.

However, these results should not be taken for granted. They will depend on the capital strength of the newly merged banks, the sustainability of their business plans and business models, and their ability to create genuine synergies and to integrate different business structures, processes and cultures. Consolidation should be judged by its ability to achieve these goals, all the while preserving competition, pluralism and banks' responsiveness to the needs of the real economy.

Banca d'Italia performs its tasks - in cooperation with the ECB, IVASS, CONSOB and the other national and international authorities - by assessing each transaction based on these criteria and verifying its compliance with Italian and EU regulations. Provided that these conditions are met, the outcome of M&A transactions is ultimately determined by the market and by shareholder decisions.

4. Financing innovation

Following the global financial crisis, firms in the advanced economies have significantly reduced their reliance on debt, and especially on bank lending. At the same time, the share of equity has increased (Figure 6).

Figure 6

Capitalization of non-financial corporations

(per cent)

Sources: National financial accounts, ECB, Bank of England and the Financial Accounts of the United States.

This change reflects profound transformations in production and finance. Regulatory reforms aimed at strengthening banks' soundness have made credit supply policies more selective and favoured firms' deleveraging. At the same time, economic activity has progressively shifted towards the service sector, which tends to rely less on credit compared with the manufacturing sector.

Digitalization has further accelerated this process, changing the nature of firms' productive capital and, with it, their financing needs. Credit is less suited to financing high-risk innovative projects: creditors bear the uncertainty that comes with them, but only benefit to a limited extent from their potential success. For these initiatives, risk capital is therefore the most appropriate instrument. These dynamics are compounded by the increase in investment in intangible assets - patents, software, licences - whose value is difficult to estimate9 and to use as collateral for loans.10

This development has fostered the growth of intermediaries specialized in the financing of innovation, such as private equity and venture capital funds. Between 2014 and 2025, the assets managed by these intermediaries tripled globally, reaching $10 trillion, with stronger growth in countries where investment in intangibles accounts for a higher share of GDP.11

The importance of these funds derives not only from the financial resources they make available over medium- and long-term horizons, but is also based on the managerial and technical skills they provide, as well as on their access to wider business and financial networks. These funds make an essential contribution: innovating means not only adopting new technologies, but rethinking products, processes and organization. It is the combination of capital and skills that determines the success of an innovative project.

The Italian market

In Italy, funds specializing in the provision of risk capital are much less developed than in the other major countries. A significant share of the transactions involves operations aimed at corporate reorganization, often with low innovative content, and early-stage investment in start-ups, while the resources devoted to supporting firms' expansion and competitive capacity remain limited.12

This can result in a bottleneck at the most delicate stage of the innovation process, i.e. the one where a promising idea has to be transformed into a firm that is able to operate on an industrial scale. It is at this stage that many Italian business initiatives end up looking abroad for capital, skills, and production and funding opportunities.

In recent years, public sector intervention has made a significant contribution to strengthening private equity and venture capital by mobilizing private sector resources through funds of funds and co-investment vehicles.13 To achieve lasting development in the industry, however, what is needed is a broad and stable base of private investors.

Insurance companies and pension funds, whose liabilities are typically medium- and long-term, are among the best-suited intermediaries to invest in uncertain projects with long maturities and to benefit from expected earnings over long-term horizons. Yet their contribution remains limited: private equity accounts for just 0.5 and 0.7 per cent, respectively, of insurance companies' and pension funds' total investments, and the weight of each sector in venture capital is negligible.

The main constraints on development are not of a regulatory nature. The legislation already makes a significant increase of investment possible, also thanks to recent changes.14 Rather, the obstacles are largely typical of a market that is still undersized. Investing in private equity and venture capital requires specialist knowledge, the expertise to select fund managers and a long time horizon, which are difficult conditions for small operators to meet. At the same time, larger investors, who are properly equipped for the task, struggle to find a supply on the domestic market that is sufficiently broad, diversified and steady.

This leads to an underdevelopment equilibrium. The shortage of stable financiers hampers the growth of private equity and venture capital funds, small-sized funds are limited in their ability to help firms scale up, and the tendency by the most promising business ventures to seek foreign markets further reduces opportunities for domestic operators.

Such an equilibrium is not self-correcting: the longer it persists, the more it anchors investors' expectations and pushes the best firms towards other markets. Moving beyond this equilibrium requires a concerted effort across the entire ecosystem, involving fund managers, institutional investors, public sector entities and firms. The market needs to grow in scale and improve its capacity to select projects, support their expansion and mobilize capital throughout the innovation cycle, from start-up formation to industrial scale-up.

With these aims in mind, funds of funds - also thanks to the catalyst role of the public sector - are instruments that can help bridge the size gap in the market by pooling resources, increasing diversification, mitigating the constraints on less structured investors and supporting the development of specialized managers. Developing this instrument, based on selective and strict criteria and a clear market-based approach, would help to achieve a broader and more stable domestic supply of risk capital.

Household saving can also contribute to the growth of risk capital. Mobilizing a larger share of household resources requires simple, transparent and affordable tools, together with more robust financial literacy which is necessary for households to make informed choices. Italy already has tax incentives for investments in risk capital;15 streamlining them and making them simpler and more flexible would increase their effectiveness. This is also the aim of the European Commission's recommendation on savings and investment accounts.16

Only acting at the domestic level, however, is not enough. Without a truly integrated European capital market, the ability to mobilize resources, diversify risks and support the growth of innovative firms will remain limited. Overcoming fragmentation is therefore an essential condition for strengthening Europe's ability to be competitive at a time in which technological innovation is playing out on a global scale.

Conclusions

Geopolitical instability and rapid technological progress will continue to affect the outlook for households, firms and financial intermediaries. We cannot eliminate risks, nor can we foresee every future development. We can, however, strengthen the capacity of our economy to absorb shocks and to turn the opportunities offered by innovation into growth.

At this juncture, preserving monetary and financial stability is essential: it is the prerequisite for continuing to invest, even in times of heightened tension. Yet the stability we are called upon to safeguard is not the stillness of an inert economy: it is the balance of an economy in motion.

The translation of stability into growth requires a financial system capable of supporting the ongoing transformations. Banks will continue to play a central role, especially in a country such as Italy, where credit remains the main source of financing for firms. However, in an economy in which innovation and intangible investment are becoming increasingly important, we also need more highly developed capital markets and an adequate availability of risk capital. The aim is not to replace bank credit, but to complement it with instruments that can meet the different needs of the economy.

This is a commitment that involves the entire financial sector: banks, insurance companies, pension funds and asset managers, each playing its part. Public action can have an important role in fostering the coordination needed to channel private resources towards high-potential projects and firms.

Italy has solid foundations: a strengthened banking system, households with a high capacity to save, and firms that have demonstrated their ability to adapt even in the most difficult circumstances. The challenge is to transform these strengths into investment, innovation and sustained growth.

Endnotes

- 1 The price of gold has also varied considerably, reflecting the increase in real interest rates and the sales carried out by some emerging countries to support their respective currencies in a period of turbulence.

- 2 As the oil trade is largely invoiced in US dollars, an increase in the price of crude oil, with trade volumes being equal, increases the value of transactions in US dollars and thus the demand for US currency to settle them.

- 3 If new competitors succeeded in expanding their product supply rapidly, including through solutions capable of overcoming the current bottlenecks, profitability expectations could be sharply revised downwards. This kind of pressure could come from China, where public and private efforts have been stepped up in recent years to rapidly develop the semiconductor industry.

- 4 The Korean stock market, which is particularly exposed to firms that produce data centre components, has recorded a correction of 25 per cent in the last few weeks.

- 5 Italy, Staff Concluding Statement of the 2026 Article IV Mission, 27 May 2026. The statement anticipates the main findings of the Financial Sector Assessment Program, which will be published in the coming days.

- 6 This figure refers to loans net of loan loss provisions. Gross of provisions, the ratio of non-performing loans to total loans was 15.2 per cent in 2016 and 2.4 per cent at the end of last year.

- 7 The calendar-based approach and its impact on the stock of non-performing loans on banks' balance sheets is described in P. Angelini, 'La nuova regolamentazione sugli NPLs e il nuovo Codice delle crisi d'impresa' (The new rules on NPLs and the new business crisis code; only in Italian), speaking notes for the conference on the options available to borrowers in distress, Mantua, 12 October 2019, and for the workshop on 'Non-performing bank loans. The task of the legislator for a timely recovery' held by Arel, Rome, 21 October 2019. In recent years, the timeframe for civil court proceedings has shortened, though still not enough to bridge the gap with the other advanced economies. For further details, see Chapter 11 of the Annual Report for 2025, 2026 (only in Italian).

- 8 Banca d'Italia's announcement follows the launch of a public consultation on the ECB's draft guidelines issued to the national competent authorities, which introduce a calendar-based approach to non-performing exposures held by less significant banks and relating to loans originated before 26 April 2019. These guidelines provide for a gradual phase-in, with full implementation by the end of 2028. They also provide some leeway to take into account banks' specificities, including exempting certain institutions from their scope.

- 9 The uncertainty about the value of intangible assets reflects the riskiness of the innovative projects with which they are associated, the presence of information asymmetries between the entrepreneur and the lender, and the absence of secondary markets for assets whose usefulness is often closely linked to their use within the firm; see L. Demmou and G. Franco, 'Mind the financing gap: enhancing the contribution of intangible assets to productivity', OECD Economics Department Working Papers, 1681, 2021; J. Haskel and S. Westlake, 'Capitalism without capital: the rise of the intangible economy', Princeton, Princeton University Press, 2018; C. Corrado, J. Haskel, C. Jona-Lasinio and M. Iommi, 'Intangible capital and modern economies', Journal of Economic Perspectives, 36, 3, 2022; N. Crouzet, J.C. Eberly, A.L. Eisfeldt and D. Papanikolaou, 'The economics of intangible capital', Journal of Economic Perspectives, 36, 3, 2022, pp. 29-52.

- 10 G. Dell'Ariccia, D. Kadyrzhanova, C. Minoiu and L. Ratnovski ('Bank lending in the knowledge economy', The Review of Financial Studies, 34, 10, pp. 5036-5076) show that, in the United States, almost half of the decline in the share of business lending in banks' balance sheets is attributable to the rise in the share of intangible investment.

- 11 For further details, see G. Gobbi, 'La finanza nell'economia della conoscenza', Bancaria, 11, 2024, pp. 58-65.

- 12 Private equity investments are concentrated in traditional transactions, where investors typically obtain a controlling stake and embark on a restructuring of business activities (buyouts), while investments aimed at supporting the firm's expansion are less developed. In venture capital, the late-stage segment, which relates to the financing phases of start-ups following their initial launch, remains weak. These phases are crucial for enabling the most promising firms to grow and compete internationally.

- 13 Cassa Depositi e Prestiti has played a key role in this respect.

- 14 The amended European Solvency II Directive, which will be fully implemented by 30 January 2027, can facilitate investment in private equity and venture capital by insurance companies, reducing capital absorption for long-term equity investments and relaxing the constraints on the granting of public guarantees to meet prudential requirements. As regards pension funds and professional pension institutions, Budget Law 199/2025 favours the growth of assets under management and the allocation of funds to equity instruments, especially for new members; furthermore, Law 193/2024, as amended by Law 118/2025, encourages investments in venture capital funds, making the tax benefits that apply to qualifying investments subject to a minimum allocation to these funds.

- 15 These include tax exemptions for investment income from participating in venture capital funds, tax credits for investments in innovative start-ups, the standard and alternative individual savings plans (Piani individuali di risparmio, PIR), and the exemption for returns on qualifying investments made by pension funds and occupational pension funds.

- 16 The recommendation defines savings and investment accounts (SIAs) as accounts regulated by individual Member States to facilitate household participation in capital markets. The European Commission suggests designing SIAs as simple instruments, offered by a number of financial intermediaries, without minimum or maximum thresholds for investment or strict holding constraints for accessing tax benefits, where envisaged. SIAs should enable investment in a wide range of financial instruments, with no specific constraints on the tax residence of issuers; see the European Commission's website, 'Savings and Investment Accounts'.

Instagram

Instagram