Playing the long game: how should monetary policy adapt to the Great Reconfiguration?

1. Introduction

When we launched this research network in 2024, I described the previous four years as exceptional: a period marked by 'a combination of shocks and structural changes with few historical precedents'.1 Looking back, that assessment seems almost cautious.

What first appeared as a sequence of extraordinary events has become a defining feature of the global economy. Geopolitical tensions, trade fragmentation and technological disruption are no longer merely temporary disturbances. They are forces that continuously reshape the environment in which households, firms and policymakers operate. They generate uncertainty that is not only high, but persistent.

For central banks, these forces pose a common challenge. They are difficult to classify as sources of pure supply or demand shocks. They affect the supply side through energy prices, production costs, trade flows and critical inputs. But they also influence demand through income, confidence, consumption and investment.

More importantly, they can alter structural relations in the economy, including the transmission of monetary policy itself.

This environment requires more than a recalibration of the policy stance. It calls for a periodic review of how we examine the inflation outlook, assess the stance and adjust the reaction function.

The ECB's 2025 strategy review was an important step in this direction as it addressed many of the issues we confront today. We must continue to refine our analytical framework while preserving the clarity of our mandate: price stability.

Today I will focus on three themes. How should monetary policy respond to large energy shocks that simultaneously trigger inflationary and recessionary forces? How do structural transformations affect the outlook and the transmission of monetary policy? And what do they imply for the way central banks take decisions under uncertainty?

I will provide a few reflections, trusting that the research community will continue to address these questions in the future.

2. The economic outlook in the euro area

In 2025, the euro area faced higher US tariffs, stronger competition from China and a sharp rise in uncertainty.2 The economy proved more resilient than expected. Real GDP grew by 1.4 per cent.3 Domestic demand more than offset the decline in net exports. High employment supported consumption, while defence spending and investment in the digital and green transitions sustained capital formation. A less restrictive monetary stance supported both households and firms.

Inflation completed its return to target amid lower demand and cost pressures, rising tariffs and the disinflationary impulse coming from China.

This was a positive outcome. But it should be interpreted with caution.

First, European households continued to save more than before the pandemic. This suggests that uncertainty remains a significant drag on activity: households consume less because they are bracing for a more uncertain future.

Second, industrial production stagnated in the second half of the year. Competition from China, increasingly visible in high-technology sectors, weighed heavily on manufacturing economies such as Germany and Italy.4 If this weakness discourages investment, it may affect not only current activity, but also the euro area's longer-term growth potential.

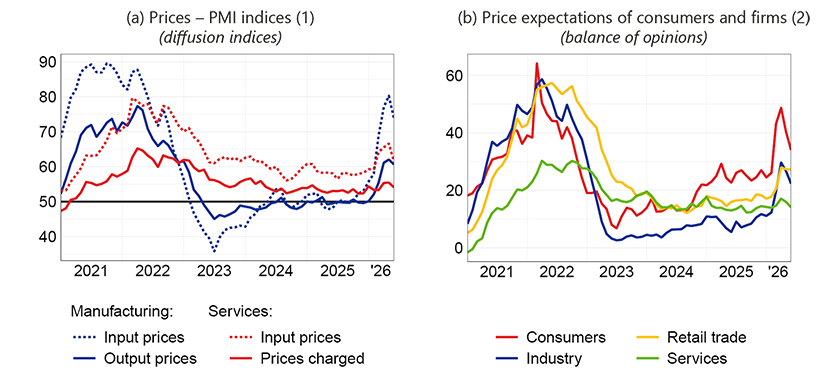

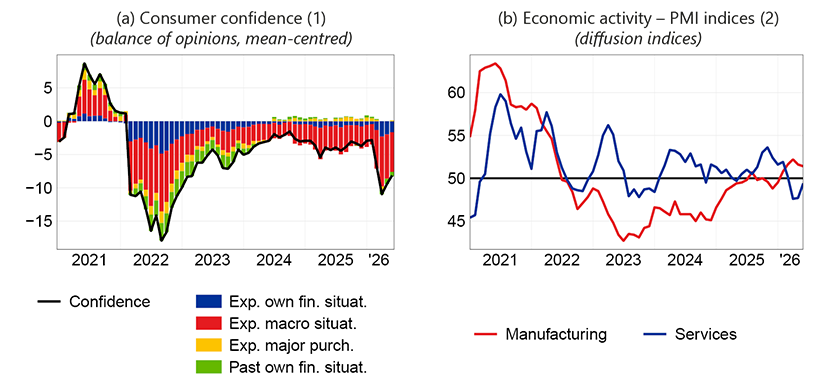

The outlook deteriorated significantly with the outbreak of the war in the Persian Gulf. Input costs and selling prices increased (Figure 1.a); short-term inflation expectations moved up (Figure 1.b). At the same time, consumer confidence fell sharply (Figure 2.a) and expected activity in services declined (Figure 2.b).5 Financial conditions also tightened: banks reported more restrictive lending standards,6 while bond yields and sovereign spreads rose.

Figure 1

Input costs, selling price intentions and inflation expectations in the euro area

Sources: Standard & Poor's Global Ratings and European Commission's Business and Consumers Surveys.

(1) Diffusion indices for input and output prices in the manufacturing and service sectors. Each index is obtained by adding half of the percentage of responses of 'stable' to the percentage of responses of 'increasing'. Latest observation: June 2026. - (2) Businesses selling price expectations over the next 3 months and consumers price expectations over the next 12 months; balance between the replies indicating 'an increase' and those indicating 'a decrease'. Positive values indicate that respondents expecting price increases outnumber those expecting price decreases. Latest observation: June 2026.

Figure 2

Consumer confidence and economic activity in the euro area

Sources: Standard & Poor's Global Ratings and European Commission's Consumer Confidence Indicator.

(1) Consumer confidence is centred on the 2000-19 average. Latest observation: June 2026. - (2) Diffusion indices for input and output prices in the manufacturing and service sectors. Each index is obtained by adding half of the percentage of responses of 'stable' to the percentage of responses of 'increasing'. Latest observation: June 2026.

The euro area faced a difficult combination: renewed inflationary pressures from commodity prices and supply chains, together with weaker confidence and demand prospects. This is precisely the environment in which monetary policy becomes more complex.

3. Dealing with the energy shock

How should the ECB deal with the energy crisis and its aftermath? Two simple answers lie at the extremes of the debate. Both are misleading.

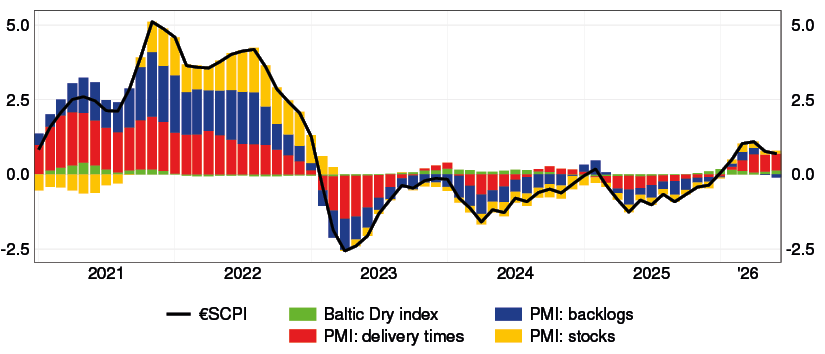

The first is that central banks should simply 'look through' temporary supply shocks. This view underestimates the scale and possible persistence of the current shock. The hit to global energy supply has been large. Damage to production and transport infrastructure could affect prices even if the conflict subsides. The governance of the Strait of Hormuz - a critical chokepoint not only for oil and gas, but also for fertilizers, aluminium, and other industrial inputs - remains uncertain. This is reflected in incipient strains on supply chains (Figure 3).

Figure 3

Euro area Supply Chain Pressure Index

(index and contributions)

Sources: Based on S&P Global PMI and LSEG data.

(1) The euro area Supply Chain Pressure Index (€SCPI) is based on the methodology of the Federal Reserve Bank of New York's Global Supply Chain Pressure Index, adapted to the euro area. The index combines four indicators: the Baltic Dry Index (BDI), capturing shipping and transportation conditions, and three PMI-based measures reflecting suppliers' delivery times, work backlogs, and inventories of production inputs. The BDI is detrended using annual growth rates. Because these indicators may respond to both supply and demand shocks, demand-driven movements are removed by regressing each series on contemporaneous and lagged values of PMI new orders, used as a proxy for demand conditions. The €SCPI is then constructed as the first principal component of the filtered series. The contribution of each component is computed using the corresponding loadings from the first eigenvector of the covariance matrix. For the sake of interpretation, the €SCPI and its components are reported as 3-month moving averages. Latest observation: June 2026.

Monetary policy cannot prevent higher energy prices from spreading through the economy. But it must prevent this process from becoming embedded in the expectations and decisions of firms and workers. Once a shock turns into a broader inflationary spiral, the cost of restoring price stability becomes materially higher.

The second misleading answer is that the current episode is a replay of the dramatic spike in energy prices of 2022, and that the ECB should therefore react forcefully, as it did then, to prevent inflation from becoming entrenched.

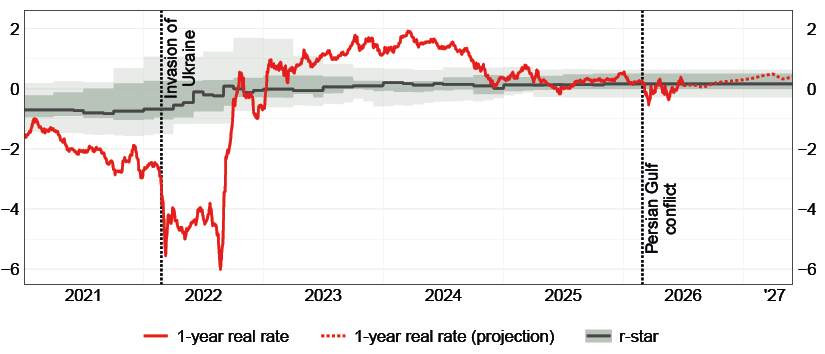

But this is not a replay of 2022. Demand is weaker. Real interest rates are higher (Figure 4). The shock has affected oil prices more than gas prices; this matters because oil prices tend to generate weaker and less persistent inflationary effects than gas prices.7 The euro area economy has also changed: its capacity to import liquefied natural gas has increased, allowing for greater diversification of suppliers; the share of renewables in electricity generation has risen. These developments have reduced - though not eliminated - the euro area's vulnerability to energy shocks.

Figure 4

Short-term real interest rate in the euro area

(per cent)

Sources: Based on ECB, Bloomberg and LSEG data.

(1) The figure shows the 1-year real interest rate (solid red line), together with its market-implied expected path (dashed red line), computed using the methodology described in M. Bernardini, L. D'Arrigo, A. Lin and A. Tiseno, 'Real interest rates and the ECB's monetary policy stance', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers), 857, 2024. The grey line and bands show, respectively, the median and the 25th-75th and 10th-90th percentile ranges across a set of quarterly estimates of the equilibrium real interest rate (r-star). The estimates are available until 2025Q4 and are held constant thereafter for visual reference. The vertical black dotted lines mark the days before the outbreak of the two conflicts (respectively, 23 February 2022 and 27 February 2026). Latest observation: 2 July 2026.

The ECB must navigate between these two extremes. It must neither dismiss the shock as temporary nor respond as if the economy were in the same position as four years ago.

3.1. Large shocks 'travel fast', but they also squeeze spending …

Faced with large cost shocks, firms tend to raise selling prices more quickly in order to protect margins, especially when their competitors are affected by the same shock.8 The frictions that make inflation sluggish in normal times may become less relevant after a large increase in costs.

This mechanism may have strengthened in recent years. After the inflation surge of 2021-22, firms have paid closer attention to their pricing strategies; furthermore, digital tools allow prices to be adjusted with far greater speed than in the past.9

Households may also update their inflation expectations more rapidly when they have recently experienced high inflation.10

These forces suggest that the first-round effects of a large energy shock can pass through to prices relatively quickly.

But this is only half of the story.

Large energy shocks also depress demand. They reduce households' purchasing power, compress firms' margins, worsen income prospects and increase uncertainty. Consumers may cut discretionary spending; firms may postpone investment. The result is a downward shift in aggregate demand, which has a negative effect on inflation.

3.2. … with complex implications for monetary policy

This dual nature makes these shocks especially difficult for monetary policy. They raise inflation through costs and lower it through demand. Their net effects depend on the relative strength and persistence of these channels.

This is why central banks must look beyond the immediate price increases. They must assess whether the shock is likely to trigger second-round effects, whether expectations remain anchored, and to what extent weaker demand will contain inflationary pressures over the medium term.

How has this approach been applied in practice? In June, the ECB Governing Council raised the deposit facility rate by 25 basis points. The decision reflected three considerations.

First, the Eurosystem staff projections pointed to a deterioration in the inflation outlook. Inflation was projected to rise to 3.0 per cent in 2026 and to return to target in the second half of 2027. Second, inflation risks were tilted to the upside, partly owing to the continued closure of the Strait of Hormuz. Third, the recalibration was aimed at preserving the anchoring of medium-term inflation expectations, a crucial condition for containing indirect and second-round effects.

Importantly, the decision to raise rates was judged to be robust across a range of scenarios. This reflects a key principle of policy making under uncertainty.11

The ongoing negotiations between the United States and Iran may lead to lower energy prices than assumed in the June baseline projections. But the outlook remains fragile. Upside risks to inflation continue to coexist with downside risks to growth. This requires constant monitoring of geopolitical developments, energy markets, supply chains, wages and inflation expectations. It also requires that monetary policy avoid committing to a predetermined path.

4. The Great Reconfiguration: challenges for monetary policy

So far, I have focused on the energy shock and its implications for monetary policy. But this shock is not an isolated event.

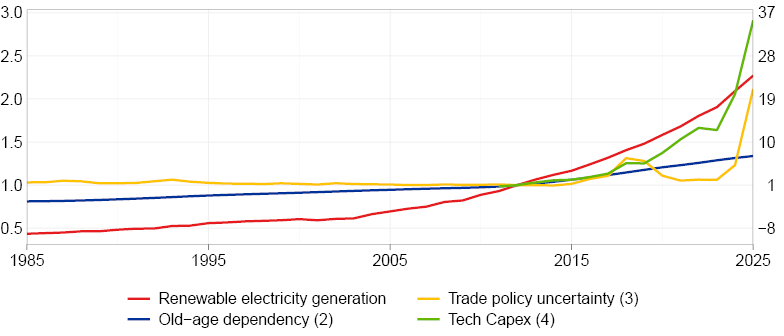

Geopolitical fragmentation, artificial intelligence and digital finance, population ageing and climate change are reshaping the environment in which households, firms and policymakers operate (Figure 5). After the Great Moderation, the world has entered what we may call a 'Great Reconfiguration'.

Figure 5

The Great Reconfiguration

(indices: 2012=1)

Sources: Based on data from LSEG, Our World in Data, PolicyUncertainty.com, and the UN.

(1) All series refer to the world unless otherwise specified. - (2) Number of people aged 65 or over per 100 people aged between 15 and 64; 2024-25 values are based on projections. - (3) Annual average of a newspaper-based index; right-hand scale. - (4) Combined capital expenditure of Alphabet, Amazon, Meta, Microsoft and Oracle; right-hand scale.

Structural change is not new. What is distinctive today is the simultaneous occurrence of several major transitions. Historical comparisons should be used with caution - especially by non-historians - but one parallel may provide useful insights: the period at the turn of the twentieth century that was to be known in Europe as the Belle Époque. It was a period of remarkable technological innovation, economic progress, trade expansion and financial integration. But it was also marked by large inequalities, geopolitical rivalries and an arms race - as well as being the apex of European imperialism.12 Beneath a surface of prosperity, tensions were building.

I do not want to push the parallel too far. It merely serves to illustrate that structural change does not necessarily unfold smoothly. Technological progress does not automatically produce stability. Economic integration does not by itself prevent fragmentation. And unresolved tensions can eventually lead to severe disruption.

Central banks are not the main actors in addressing these tensions. But they must understand how structural forces affect the economy and the transmission of monetary policy. The channels through which technology, demographics, climate change and geopolitics may impact growth and inflation are reasonably well understood.13 But the scale and timing of these effects are not.

In this context, the Great Reconfiguration raises three specific questions for monetary policy. How does the interaction of these structural forces affect the way we assess the macroeconomic outlook? How will monetary policy transmission change? How should the reaction function adapt? Let me consider each question in turn.

4.1. What happens when the trends collide?

Structural trends do not operate in isolation. Their effects may reinforce or offset each other.14

Consider AI. Some forces may amplify its macroeconomic impact. AI requires large amounts of energy and water. Therefore, it has important complementarities with the green transition. Expanding the supply of clean and affordable energy, and improving the management of natural resources, would support the development of more powerful AI systems. In turn, AI can improve energy efficiency, optimize water use and accelerate innovation in clean technologies.

Other forces may hold it back. Geopolitical fragmentation could restrict access to critical inputs, data and digital infrastructure. Ageing could reduce the supply of skills needed to adopt and use new technologies effectively.

These interactions create additional uncertainty around the ultimate impact of AI on productivity, inflation and growth.

They also complicate one of the most important tasks of macroeconomic analysis: distinguishing structural change from cyclical fluctuations. Identifying a single structural shift in real time is difficult. Identifying several shifts at once, while they interact with one another, is even harder.15

The Great Reconfiguration requires first and foremost intellectual humility in interpreting real-time data.

4.2. How will the transmission mechanism evolve?

The second question concerns the transmission of monetary policy. Structural changes are likely to alter some of the channels through which monetary policy affects the economy.16 But the direction of these effects is not obvious.

Some forces may strengthen the transmission. AI can help firms process information on costs and demand more rapidly, allowing them to adjust prices more frequently. Inflation may therefore react more quickly and sharply to changes in financing conditions.17

Digital banking might work in a similar direction. Digital tools make it easier for depositors to compare rates and move their funds across banks. If this intensifies the competition for deposits, the pass-through from policy rates to deposit rates should become faster and stronger.18

Other forces may weaken the transmission. Ageing is one example. In societies where pensioners account for a large share of the population, household spending may depend less on interest-sensitive decisions, such as buying homes or durable goods.19 Ageing may also interact with digitalization: digital tools reduce search and switching costs, but their impact may be smaller if older households are less inclined to use them.

Geopolitical fragmentation may also weaken the link between investment and interest rates. Firms and governments may invest more in resilience: diversifying suppliers, strengthening cyber security or holding larger inventories. When these decisions are driven by long-term strategic considerations, they may be less responsive to financing costs.

These examples point to a broader conclusion: structural change can make monetary policy transmission less predictable. The same change in policy rates may have different effects depending on the structure of the financial system, the age profile of the population, the degree of digitalization and the geopolitical environment.

This means that the transmission mechanism must be continuously reassessed.

4.3. Does monetary policy need a new playbook?

The third question concerns the reaction function.20

Structural change complicates the assessment of the monetary policy stance. This assessment typically relies on estimates of the equilibrium interest rate, or r-star. But the forces at play today push r-star in different directions. Demographics tend to reduce it, while artificial intelligence and fragmentation may operate through opposing channels. The net effect is uncertain.21

The difficulties do not end there.

If structural change alters the transmission mechanism, it becomes harder to calibrate the appropriate response to shocks. A policy adjustment that would have had predictable effects in the past may now operate differently.

Structural change could also modify the nature and the distribution of the financial stability risks confronted by monetary authorities.

In this environment, robustness becomes even more important.

Central banks should continue to use central projections, but they may have to rely more systematically on alternative scenarios and sensitivity analysis. They should test policy choices against different assumptions about energy prices, supply chains, productivity, financial conditions and expectations.

5. Conclusions

Let me conclude.

Supply shocks are an old challenge for monetary policy. Today, however, they are becoming more frequent, more persistent and more closely intertwined with the structural transformations of the global economy.

In this fluid environment, central banks must keep improving the way they interpret shocks, assess transmission and take decisions under uncertainty. Monetary policy must adapt to a changing economy.

This requires investing in new forms of knowledge. During the pandemic, epidemiology became part of the policy conversation. Today, computer science, political science, climate science and energy economics are increasingly part of the toolkit of central banks.

This applies even more to research. The ChaMP network took this challenge seriously from the start. It was established to study the 'challenges for monetary policy transmission in a changing world'. That world is changing faster than expected.

I am sure the network has laid the foundations for partnerships that will continue to bear fruit in the years ahead. Many of these partnerships will be interdisciplinary. Economists and non-economists will need to work together to understand a future that remains uncertain, but is rapidly approaching.

As central bankers, playing the long game means keeping our mandate firmly in sight while adapting our analysis to the world in which that mandate must be delivered.

Thank you very much and enjoy the rest of the conference.

Endnotes

- 1 F. Panetta, 'Monetary policy in a shifting landscape', inaugural Conference of the Research Network on 'Challenges for Monetary Policy Transmission in a Changing World', Frankfurt, 25 April 2024.

- 2 Not quite an 'everything everywhere all at once' situation, but almost (F. Panetta, 'Everything everywhere all at once: responding to multiple global shocks', speech at a panel on 'Global shocks, policy spillovers and geo-strategic risks: how to coordinate policies' at The ECB and its Watchers XXIII Conference, Frankfurt, 22 March 2023).

- 3 Excluding Ireland's contribution - which is influenced by the statistical treatment of multinationals' operations - growth remained around 1.0 per cent.

- 4 V. Aprigliano et al., 'China Shock 2.0: structural drivers and implications for the euro area', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers), 1025, 2026.

- 5 Historical regularities show that energy shocks trigger a rapid adjustment in discretionary spending, mostly related to recreational services, reflecting their immediate effects on consumer prices and households' overall purchasing power; see Corsello, A. Foschi, M. Fruzzetti and M. Riggi, 'Household consumption in Italy: basket composition and responsiveness to macroeconomic shocks', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers), forthcoming. The resilience of the manufacturing sector is largely due to frontloading, as the war could lead to new supply bottlenecks.

- 6 The tightening was driven by higher risk perception and lower risk tolerance. Among the main countries, banks in Spain, France and Germany reported tighter credit standards, whereas banks in Italy indicated no changes. In Q2 2026 banks anticipate a marked tightening, which, if realized, would match the change in credit standards observed in Q2 2022. Descriptive evidence suggests that the credit supply tightening was primarily associated with banks more exposed to sectors highly affected by higher energy costs.

- 7 This reflects the key role of gas and electricity across economic sectors; see F. Corsello and A. Foschi, 'The different effects of oil and gas supply shocks on euro-area inflation', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers),1024, 2026, and S. Neri 'Energy prices, inflation, and the ECB's monetary policy during the 2021-22 energy crisis', European Economic Review, forthcoming.

- 8 A. Cavallo, F. Lippi and K. Miyahara, 'Large Shocks Travel Fast', American Economic Review, 6, 4, 2024, pp. 558-574.

- 9 Z.Y. Brown and A. MacKay, 'Competition in Pricing Algorithms', American Economic Journal: Microeconomics, 2023. This view is consistent with the assessment made by the firms that took part in the symposium of the National Association for Business Economics hosted by the Bank of Italy in Rome in April 2026.

- 10 Research shows that those households that experienced high inflation adapt their expectations very quickly when a new shock occurs. See U.M. Malmendier and S. Nagel, 'Seemingly Anchored Inflation Expectations', CEPR Discussion Paper Series, 21632, 2026.

- 11 F. Panetta, 'Normalising monetary policy in non-normal times', speech delivered at a policy lecture hosted by the SAFE Policy Center at Goethe University and the Centre for Economic Policy Research (CEPR), Frankfurt, 25 May 2022.

- 12 The Belle Époque (1871-1914) was a period characterized by increasing industrialization, rapid economic growth, expanding international trade - also fuelled by declining transport costs - and an unprecedented degree of financial integration under the Gold Standard. Transformative innovations - including electricity, the telephone, modern steel production, advances in chemistry and pharmaceuticals, and the automobile - progressively reshaped production, communication, and everyday life. Yet beneath this climate of prosperity and optimism, geopolitical rivalries continued to build. In the words of Eric Hobsbawm, 'It was an era of unparalleled peace in the western world, which engendered an era of equally unparalleled world wars' (E.J. Hobsbawm, The Age of Empire, 1875-1914, Vintage Books Ed., 1989, p. 9).

- 13 See, for example, ECB, 'A strategic view on the economic and inflation environment in the euro area', Occasional Paper Series, 371, 2025.

- 14 For an initial approach to this complex issue, see L. Rachel, 'What Next for r*? A Capital Market Equilibrium Perspective on the Natural Rate of Interest', Brookings Papers on Economic Activity, Fall, 2025, pp. 131-187. The paper develops a framework to quantify the effects of structural forces on r-star accounting for their interactions.

- 15 For monetary policy, this distinction is essential. Mistaking a structural shift for a temporary fluctuation - or the reverse - is a well-known recipe for policy errors. If productivity growth is underestimated, a sustainable expansion may be mistaken for excess demand, leading monetary policy to become too restrictive. Conversely, if a temporary boom is mistaken for a permanent increase in potential output, inflationary pressures may be underestimated, and monetary policy may become too loose. See, for instance, A. Orphanides, 'Monetary Policy Rules Based on Real-Time Data', American Economic Review, 91, 4, 2001, pp. 964-985.

- 16 G. Ascari et al., 'Monetary policy transmission and structural changes', European Central Bank, Occasional Paper Series, 393, 2026.

- 17 G. Avaradi, Z. Liu and S. Zhao, 'AI-Powered Algorithmic Pricing and Monetary Policy', Federal Reserve Bank of San Francisco Economic Letter, 12, 2026.

- 18 See, for example, F. Ciocchetta, R. Gallo, S. Magri and M. Molinari, 'Friends or foes? Banks' deposits and digitalization during monetary tightening', Banca d'Italia, Temi di Discussione (Working Papers), 1490, 2025; I. Erel, J. Liebersohn, C. Yannelis and S. Earnest, 'Monetary Policy Transmission Through Online Banks', NBER Working Paper Series, 31380, 2025; K. Budnik, 'Digital banking and the evolving monetary policy transmission', European Central Bank, Working Paper Series, 3206, 2026; M. Brei, G. Cornelli, L. Gambacorta and B. Hofmann, 'The digitalisation of banking and social media: implications for deposit pricing', BIS Working Papers, 1357, 2026.

- 19 J.V. Leahy and A. Thapar, 'Age Structure and the Impact of Monetary Policy', American Economic Journal: Macroeconomics, 14, 4, 2022, pp. 136-173; J. Kopecky and G. Mangiante, 'Monetary Policy Goes Boomer: The Effect of Population Age Structure on Policy Transmission', Trinity Economic Paper, 1725, 2025.

- 20 ECB, Report on monetary policy tools, strategy and communication, Occasional Paper Series, 372, 2025.

- 21 The issue is more complex than this summary suggests. AI may boost productivity and investment, raising r-star; but it may also increase markups or inequality, lowering it. Geopolitical fragmentation may reduce efficiency and potential growth, lowering r-star; but it may also partly reverse the global savings glut, raising it. For a discussion of these issues see, for instance, L. Rachel, 2025, op. cit., and L. Esposito, E. Guglielminetti, E. Moracci, A. Papetti and M. Pisani, 'The implications of AI for monetary policy: a first assessment', Banca d'Italia, Questioni di Economia e Finanza (Occasional Papers), forthcoming. See also F. Panetta, 'The ECB must stay pragmatic in setting rates. R-star debate becomes less useful as monetary policy approaches neutral level', Financial Times, 26 March 2025.

Instagram

Instagram