Interconnect to stabilize: cross-border payments in a fragmenting world

At the heart of every financial system lies its payments infrastructure, which enables money to move safely and efficiently between people, firms, and governments, at home and across borders.

But payments are far more than a technical utility. They are a critical enabler of the widespread acceptance of money and its effective use in practice.

Without a reliable payment system, money cannot fully perform its role as a means of payment - and trust in the financial system ultimately rests on that foundation. This is why payments sit at the intersection of monetary policy, financial stability and financial inclusion.

Cross-border payments remain the most glaringly unfinished business of financial modernization. Domestic payments have been transformed over the past two decades - faster, cheaper and available around the clock. Yet the moment a payment crosses a border, it often enters a world that still runs on slow rails, characterized by fragmented rules and high costs.

This is no longer just a test of financial efficiency. It is becoming a test of whether the global economy can remain connected in a world increasingly exposed to strategic rivalry.

Today, I will examine why this gap persists and chart a course towards faster, cheaper and more inclusive cross-border payments - one that can help jurisdictions navigate towards a more open and interoperable global system.

1. Why enhancing cross-border payments matters - the economic case

Enhancing cross-border payments is not simply a matter of convenience. It is essential for a more efficient and inclusive global economy. Two considerations stand out.

First, more efficient cross-border payments support trade and integration. For a business serving international customers or sourcing goods abroad, reliable payment channels are as vital as the ships, trucks and planes that move the goods. Households, too, increasingly transact across borders - buying online or sending money to family members overseas. Yet these payments too often still move through inefficient channels, constraining commerce and investment.

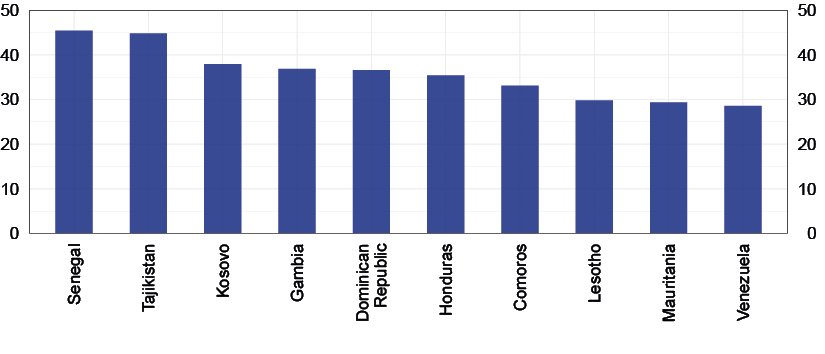

Second, improvements in cross-border payments would make the greatest difference for the most vulnerable. Over the last decade, remittances have increased by 60 per cent1 and are likely to continue rising amid growing migration flows. In some countries, more than one adult in three receives international remittances (Figure 1).

Figure 1

Share of adults who received an international remittance in 2024 in selected countries

(per cent)

Source: L. Klapper, D. Singer, L. Starita and A. Norris, 'The Global Findex Database 2025: Connectivity and Financial Inclusion in the Digital Economy', World Bank, 2025.

Low-value remittances can carry prohibitive fees. In Sub-Saharan Africa, sending $200 through formal channels can cost $20 or more. These costs act as a shadow tax on labour income earned abroad and discourage the use of formal channels, pushing individuals towards informal and less secure alternatives.2

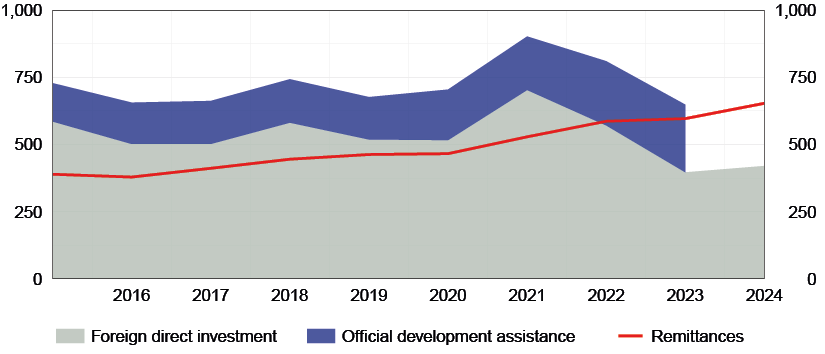

In 2024, remittances to low- and middle-income countries reached $650 billion, an amount broadly comparable to the combined value of foreign direct investment and official development assistance (Figure 2).3 Lowering remittance costs to the G20 and UN target of 3 per cent would generate savings of between $7 and $22 billion per year,4 directly benefiting many low-income households and communities.

Figure 2

External financial flows to low and middle-income countries

(billions of US dollars)

Source: World Bank, World Development Indicators.

(1) Nominal values. Official Development Assistance data for 2024 are not yet available.

In some countries, corporates and households are turning to stablecoins for remittances and cross-border payments.5 The appeal is understandable: faster transfers and, for users faced with weak currencies or capital controls, a store-of-value alternative outside fragile domestic systems.

Yet the evidence on their efficiency remains inconclusive.6 A preliminary analysis by Banca d'Italia shows that stablecoin-based solutions offer no systematic cost advantage. Costs differ markedly across corridors and are strongly influenced by on- and off-ramp fees, reaching 9 per cent in some cases.7

The risks, however, are real: vulnerability to runs, threats to monetary sovereignty in smaller economies, irreversible losses from operational failures - due to lost keys, coding flaws and cyberattacks - and serious financial integrity concerns where private wallets operate on opaque networks.8 And a fundamental question persists: who manages disputes when payments occur on a borderless ledger with no jurisdictional anchor?

Nonetheless, these risks are not a reason to close the door on innovation. Several jurisdictions are adopting dedicated regimes that help mitigate them,9 and where sound regulation is in place, stablecoins will have a role to play for specific corridors.

However, regulation alone is not sufficient. We also need efficient payment solutions anchored in the safety of central bank money. The answer is not regulation alone, but better alternatives - and many are already operational, with more under development.

2. Why cross-border payments underperform

International payments face structural challenges rooted not just in technical limitations, but also in the way cross-border arrangements are organized.

First, cross-border payments are inherently complex, involving multiple jurisdictions, currencies and time zones. Transactions must navigate a patchwork of legal regimes, compliance obligations, data protection rules, capital controls and supervisory authorities. Where rules and procedures are not harmonized, establishing effective governance frameworks is difficult. Moreover, sending money across regions with large time zone differences can be particularly burdensome, as delays in clearing and settlement raise liquidity costs and constrain international financial flows.

Second, this complexity is compounded by the fragmentation of the technical infrastructures underpinning cross-border payments. Unharmonized messaging standards and legacy formats often lack the structured information needed for straight-through processing and effective compliance screening, leading to delays, manual interventions and false positives.

Third, the correspondent banking model - long the backbone of international payments - has become more concentrated and less competitive,10 keeping costs high and leaving some markets underserved.11 For geographically distant jurisdictions or thinly traded currencies, transactions may have to travel through long chains of intermediaries. Each link adds processing steps, compliance checks, reconciliation and costs. 12

Finally, foreign-exchange (FX) conversion costs remain a major obstacle. They reflect limited liquidity in many local currency markets, the frequent use of major reserve currencies as intermediaries, and limited competition in FX provision - the latter compounded by insufficient transparency in retail pricing to individuals. These costs, often passed on to end users, are further inflated by the significant funding challenges faced by intermediaries due to the need to pre-position liquidity across multiple currencies.

These problems cannot be solved by technology alone. They require action to harmonize rules and standards, expand interoperability13 and foster competition - supported, but not substituted, by innovation.

3. The G20 Roadmap on cross-border payments: the initial response

In 2020, the G20 launched a comprehensive programme to enhance cross-border payments, known as the G20 Roadmap.14

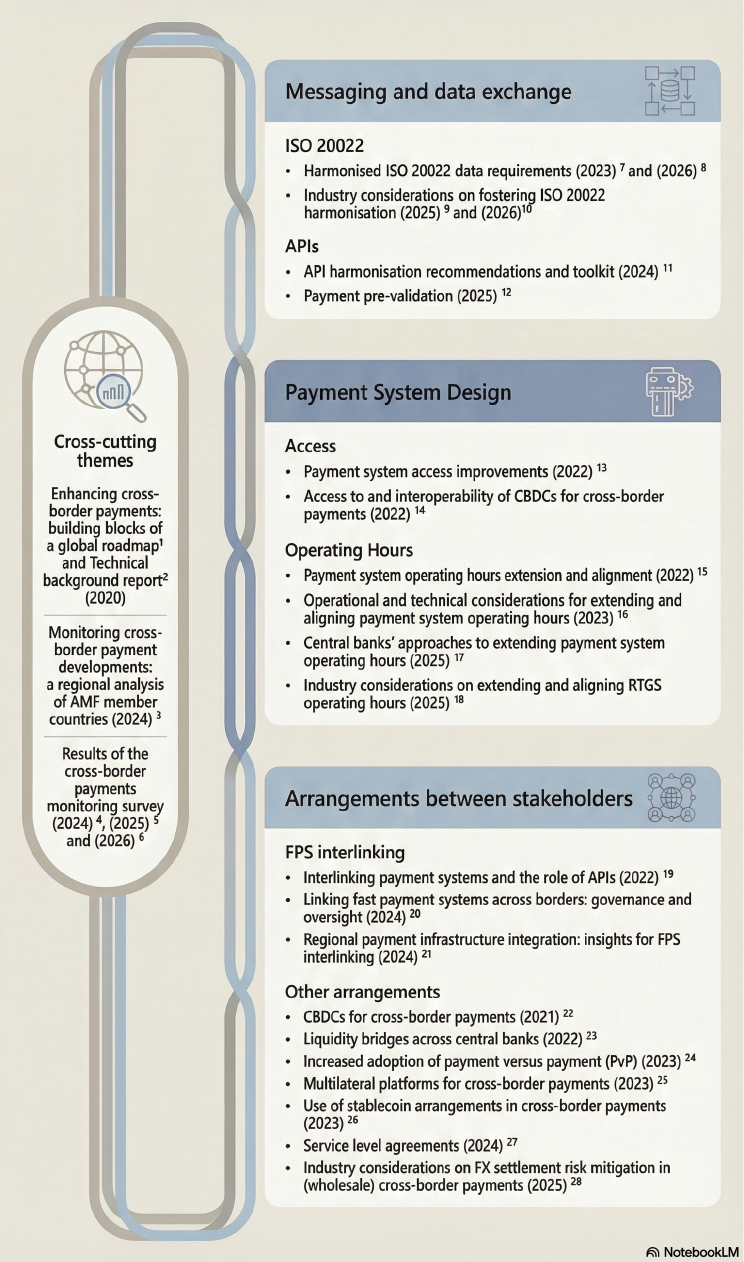

Six years on, considerable progress has been made in identifying the structural frictions and shaping practical policy responses.15 The Committee on Payments and Market Infrastructures (CPMI) has played a leading role in strengthening messaging standards, improving payment system design, and enhancing the arrangements that support cross-border payments (see Appendix).

The CPMI has developed practical frameworks to help payment system operators extend operating hours,16 broaden access to new participants, such as non-bank payment service providers,17 harmonize application programming interfaces (APIs)18 and strengthen the governance and oversight of interlinking arrangements.19 One major achievement has been the development of harmonized ISO 2002220 message data requirements.21

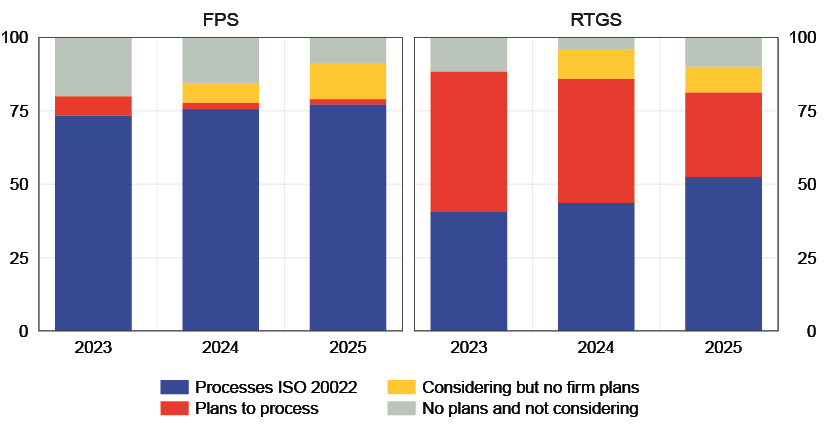

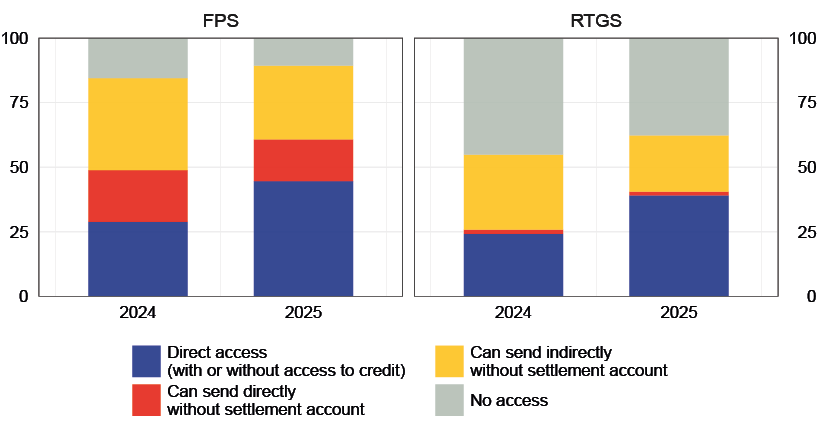

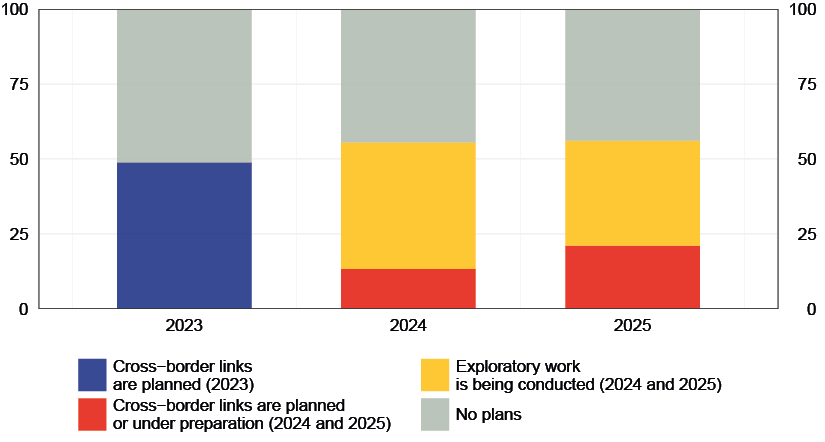

These policy efforts have started to yield tangible signs of change in payment systems across the globe. According to the latest monitoring survey, 22 approximately 80 per cent of payment systems have either already migrated to ISO 20022 messaging for domestic payments or plan to do so (Figure 3). The proportion of fast payment systems (FPSs)23 and real-time gross settlement (RTGS) systems24 providing direct access to non-bank payment service providers has also increased, reaching 45 and 39 per cent respectively (Figure 4). Moreover, the number of FPSs planning to establish new cross-border links doubled in 2025 (Figure 5).

Figure 3

ISO 20022 adoption

(per cent)

Source: T. Lammer, F. Leppanen and F. Semorile, 'Enhancing crossborder payments step by step: insights from the 2025 monitoring survey', CPMI Brief, forthcoming.

(1) As a percentage of 45 FPSs for 2023 and 2024 and 57 FPSs for 2025, and 69 RTGS systems for 2023, 71 RTGS systems for 2024 and 80 RTGS systems for 2025. The category 'considering but no firm plans' was not included as a separate category in the 2023 survey.

Figure 4

Non-bank payment service providers' access to payment systems

(per cent)

Source: T. Lammer, F. Leppanen and F. Semorile, forthcoming, op. cit.

(1) As a percentage of 45 FPSs for 2024 and 56 FPSs for 2025, and 62 RTGS systems for 2024 and 69 RTGS systems for 2025.

Figure 5

FPS plans to establish interlinking arrangements

(per cent)

Source: T. Lammer, F. Leppanen and F. Semorile, forthcoming, op. cit.

(1) As a percentage of 45 FPSs for 2023 and 2024, and 57 FPSs for 2025. The 2025 and 2024 surveys included categories on 'plans and preparations', 'exploratory work' and 'no plans' while the 2023 survey only included categories on 'plans' and 'no plans'.

Despite these positive developments at infrastructure level, none of the four G20 targets - speed, cost, transparency and access - has been achieved for remittances:25 For example, the global average cost remains close to 6.4 per cent, more than double the 3 per cent target set for end-2030.26

The main obstacles are both structural and domestic. Structural because they stem from the complexity of managing multiple currencies, time zones, fragmented rules, standards and infrastructures across borders. Domestic because many bottlenecks reflect national policy choices beyond the direct reach of central banks or international bodies such as the G20.

Yet the world in which the Roadmap was conceived is no longer the world in which it must now be implemented.

4. The geopolitical complication

Cross-border payment infrastructures are not neutral channels. They are part of the broader international monetary and financial system and reflect its underlying distribution of economic weight. The central role of the dollar - and, to a lesser extent, of the euro - means that a large share of global payment, clearing and settlement activity is concentrated in a limited number of jurisdictions. This centrality has long supported efficiency, liquidity and stability, but it also carries strategic implications.

This became particularly evident following Russia's invasion of Ukraine. In response, a broad coalition of countries introduced coordinated financial sanctions. Access to SWIFT was suspended for designated financial institutions, and certain official reserve assets held in sanctioning jurisdictions were immobilized.27

These measures were not arbitrary; they reflected the collective response of sovereign states to an armed conflict widely regarded as a violation of international law. They demonstrated that payment infrastructures are not merely technical arrangements, but instruments of economic statecraft embedded in the geopolitical landscape.

At the same time, some countries and regional groupings have stepped up their efforts to strengthen monetary sovereignty and reduce external dependencies. New payment arrangements, alternative messaging systems and regional settlement initiatives are emerging - some driven by resilience, others by strategic autonomy.28

This raises the risk of fragmentation. A proliferation of parallel systems - weakly connected or politically segmented - would reduce interoperability, increase costs and erode the efficiency gains the G20 Roadmap seeks to deliver, particularly for low-income countries.

These developments raise fundamental questions about whether the G20 Roadmap can retain the political support and global relevance it needs.

5. Mapping the road ahead

The answer is not to retreat behind parallel systems, but to reaffirm the Roadmap's purpose in a changed environment. Fragmentation would deliver neither resilience nor sovereignty - only higher costs, shallower liquidity, and new divisions, with the heaviest burden falling on the economies least able to bear it.

These are not abstract concerns, and the political resolve needed to keep the global payments system open and connected cannot be taken for granted. Yet precisely because the stakes are high, the case for collective action is stronger, not weaker.

Advancing this agenda, however, also demands bold action at the domestic level. Inefficiencies tend to concentrate in the first and last mile of international payments, where domestic frameworks and policies apply, many of which lie beyond the remit of central banks and international institutions. Progress therefore requires decisive action at national level by a broad set of public authorities and industry.

With this in mind, the CPMI and the Financial Stability Board (FSB) are encouraging individual jurisdictions to volunteer and develop their own Multi-stakeholder Action Plan - in short, a national MAP for cross-border payments. Each MAP should reflect the jurisdiction's unique starting point and domestic priorities, while setting out a coherent strategy that builds on and complements the work already done at the international level, in order to make cross-border payments faster, cheaper, more transparent and more inclusive.

Progress will be most effective if jurisdictions structure their MAPs around three key coordinates.

First coordinate: National payment infrastructures

First, strengthening national payment infrastructures.29 Extending operating hours and widening the global settlement window30 are practical steps that can materially improve end-to-end speed. Full adoption of ISO 20022 - the lingua franca of payments - will provide the common data foundation needed for straight-through processing, greater automation, including in AML/CFT controls, and lower operational costs.31

Strengthening national payment infrastructures also means building tomorrow's system - one that fully harnesses new technologies. Even as digital transformation reshapes the monetary architecture, its foundations remain intact. Technology can enhance how money works, but it cannot be a substitute for the credibility of an independent central bank or for the authority of the State, on which monetary trust ultimately rests.32 Central bank money must remain the ultimate settlement asset, interacting with private payment solutions seamlessly so that innovation is both efficient and safe.33

Second coordinate: Regulation

Second, improving regulation - with a particular focus on competition, transparency and security.

Regulation must reinforce competition by creating a level playing field between banks and non-bank providers of cross-border payments.34 Transparency is equally important: users should be able to compare fees, FX rates, mark-ups and execution times at a glance. The harmonized implementation of the Financial Action Task Force (FATF) 'Travel Rule'35 will also reinforce security by reducing errors and fraud, while helping detect financial crime.

Finally, data frameworks - the regulatory requirements for collecting, storing and managing data - should enable data exchange across borders, while being anchored in the highest standards of privacy and security.36 This goal calls for the systematic involvement of Data Protection Authorities, whose expertise is indispensable in aligning payment efficiency and financial crime compliance with data protection principles.

Third coordinate: Global reach

Third, safeguarding openness, interoperability and global reach. In an era of strategic rivalry, lower costs and faster payments only matter if the underlying rails remain accessible, resilient and trusted.

Two interlinkage models are emerging - bilateral and multilateral - and a genuinely multipolar architecture will need both.

Regional hubs harness network effects and economies of scale where economic integration and strategic alignment run deep; bilateral links offer simplicity, flexibility and agile governance to connect major corridors and hubs with one another.

This layered structure lets jurisdictions recalibrate agreements as priorities and alliances evolve, while preserving the autonomy of domestic systems and strengthening resilience. Europe is already moving in this direction: TIPS, the Eurosystem instant payment system, has become the regional platform for cross-border payments and is being connected bilaterally with other countries.37

Completing the MAP: Collaboration and capacity building

These three coordinates must be underpinned by two cross-cutting commitments.

First, public-private collaboration.38 Policymakers can provide regulatory clarity, and central banks can set common standards, but without sustained industry action - automating compliance, advancing interoperability, and improving transparency for end users - reforms will inevitably fall short.

Second, capacity-building and technical assistance. International organizations can help emerging and developing economies to upgrade their systems, adopt global standards and connect to regional infrastructures. Economies with more mature systems have a particular responsibility to lead by example - strengthening their own systems, linking them across borders, and innovating within sound and open governance structures - and technical cooperation can naturally evolve into broader regional integration.39 Finally, it is important that jurisdictions share their experience with each other, within and beyond the G20.40

Conclusion

The G20 Roadmap has set the course. Now, it is up to each jurisdiction to map its own route by translating the global agenda into domestic action. For those economies still lagging behind, multi-stakeholder action plans offer a concrete path to strengthen domestic infrastructures, remove bottlenecks, and ensure that progress is not confined to a few jurisdictions. For more advanced economies, the action plans represent an opportunity - and a responsibility - to lead by example.

Efficiency alone, however, is not enough. Faster, cheaper, more transparent and more accessible payments are only meaningful if the underlying rails remain open, interoperable, resilient and trusted. In an era of growing strategic rivalry, preserving a global system that remains connected rather than divided is not simply desirable - it is indispensable.

Interconnect to stabilize. That is the guiding principle - and the only path forward.

APPENDIX

Overview the CPMI's contribution to the G20 Roadmap for enhancing cross-border payments

Source: CPMI.

(1) CPMI, Enhancing cross-border payments: building blocks of a global roadmap. Stage 2 report to the G20, July 2020.

(2) CPMI, Enhancing cross-border payments: building blocks of a global roadmap. Stage 2 report to the G20 - technical background report, July 2020. - (3) H. Attia, M. Glowka, A. Illes and T. Lammer, 'Monitoring cross-border payment developments: a regional analysis of AMF member countries', CPMI Brief, 2, 2024. - (4) E. Fitzgerald, A. Illes and T. Lammer, 'Steady as we go: results of the 2023 CPMI cross-border payments monitoring survey', CPMI Brief, 5, 2024. - (5) E. Fitzgerald, A. Illes, T. Lammer, F. Leppanen and F. Semorile, 'Moving on up: results of the 2024 cross-border payments monitoring survey', CPMI Brief, 10, 2025. - (6) T. Lammer, F. Leppanen and F. Semorile, 'Enhancing cross-border payments step by step: insights from the 2025 monitoring survey', CPMI Brief, forthcoming. - (7) CPMI, Harmonised ISO 20022 data requirements for enhancing cross-border payments. Report to the G20, October 2023. - (8) CPMI, Harmonised ISO 20022 data requirements for enhancing cross-border payments. Updated report, February 2026. - (9) Cross-border payments interoperability and extension taskforce, Fostering ISO 20022 harmonisation. Consolidated report, January 2025. - (10) Cross-border payments interoperability and extension taskforce, Fostering ISO 20022 harmonisation. Follow-up report, February 2026. - (11) CPMI, Promoting the harmonisation of application programming interfaces to enhance cross-border payments: recommendations and toolkit. Report to the G20, October 2024. - (12) D. Chamberlain, A. Ismail, M. Kroon, T. Lammer and P. Makgetsi, 'Safety and efficiency through payment pre-validation: spotting issues before money moves' , CPMI Brief, 9, 2025. - (13) CPMI, Improving access to payment systems for cross-border payments: best practices for self-assessments, May 2022. - (14) CPMI, BIS Innovation Hub, IMF and World Bank, Options for access to and interoperability of CBDCs for cross-border payments. Report to the G20, July 2022. - (15) CPMI, Extending and aligning payment system operating hours for cross-border payments. Final report, May 2022. - (16) CPMI, Operational and technical considerations for extending and aligning payment system operating hours for cross-border payments: An analytical framework. Technical report, February 2023. - (17) J. Choolhun, C. Conesa, E. Fitzgerald, M.J. García Ravassa and T. Lammer, 'Changing the clock: practical approaches to extend payment system operating hours', CPMI Brief, 6, 2025. - (18) Cross-border payments interoperability and extension taskforce, Extending and aligning RTGS operating hours, March 2025. - (19) CPMI, Interlinking payment systems and the role of application programming interfaces: a framework for cross-border payments. Report to the G20, July 2022. - (20) CPMI, Linking fast payment systems across borders: governance and oversight. Final report to the G20, October 2024. - (21) A. Di Iorio, E. Fitzgerald, T. Lammer and T. Rice, 'Regional payment infrastructure integration: insights for interlinking fast payment systems', CPMI Brief, 4, 2024. - (22) CPMI, BIS Innovation Hub, IMF and World Bank, Central bank digital currencies for cross-border payments. Report to the G20, July 2021. - (23) CPMI, Liquidity bridges across central banks for cross-border payments. Analysis and framework, September 2022. - (24) CPMI, Facilitating increased adoption of payment versus payment (PvP). Final report, March 2023. - (25) CPMI, BIS Innovation Hub, IMF and World Bank, Exploring multilateral platforms for cross-border payments, January 2023. - (26) CPMI, Considerations for the use of stablecoin arrangements in cross-border payments. CPMI Report, October 2023. - (27) CPMI, Service level agreements for cross-border payment arrangements: recommendations and key features. CPMI Report, April 2024. - (28) Cross-border payments interoperability and extension taskforce, FX settlement risk mitigation in (wholesale) cross-border payments, March 2025.

Endnotes

- * I would like to thank Alberto Di Iorio, Thomas Lammer and Antonio Perrella for their valuable insights and contributions; Valentina Memoli for editorial support.

- 1 Value of remittances, in nominal terms.

- 2 For example, according to a recent study, between 17 and 25 per cent of migrants remit funds via informal channels in some African jurisdictions (see O. Alper, M. Camino, A. Garcia Vargas and B. Savonitto, 'Remittance behaviors among migrant communities evidence from Ethiopian and Nigerian senders', September 2025).

- 3 In 2023, the combined value of foreign direct investment and official development assistance received by low- and middle-income countries amounted to approximately $650 billion (see World Bank, World Development Indicator Database). Data on official development assistance for 2024 are not yet available.

- 4 Assuming an average cost of between 4.1 and 6.4 per cent. These estimates are based on the World Bank's Remittance Prices Worldwide report for Q3 2025, which reflects the average cost for sending $500 and $200.

- 5 For example, the total value of crypto-assets received by Sub-Saharan Africa, Latin America, and Eastern Europe increased by approximately 40 per cent from 2023 to 2024, likely driven by stablecoin-based remittances (see IMF, 'Crypto-assets monitor', 23 May 2025).

- 6 Evidence on the cost of stablecoin-based cross-border payments is mixed. The 2024 Geography of Crypto Report by Chainalysis indicates that, in Sub-Saharan Africa, some stablecoin transfers can be considerably cheaper than traditional remittance channels. Certain industry sources also report very low fees for stablecoin transactions (see the Coinbase Institute website, 'Crypto and Remittances'). However, other analyses find that these advantages are not consistent across corridors: FXC Intelligence, for instance, shows that stablecoins only outperform traditional transfers in specific cases (L. Ingham, C. Tyndall, A. Lawal and D. Webber, 'The state of stablecoins in cross-border payments: the 2025 industry primer', FXC Intelligence, 17 July 2025). Moreover, recent empirical work indicates that stablecoin transactions - even before accounting for on-ramp fees - can exceed the G20 cost targets and, in some instances, be significantly higher (L. Nestor, 'Stablecoin performance in cross-border payments: evidence from a digital dollar wallet', September 2025).

- 7 A. Di Iorio, E. Di Stefano, M. Mascioli and G. Trebeschi, 'Are stablecoins efficient for remittances? Evidence from a mystery shopping exercise by the Bank of Italy', Banca d'Italia, mimeo, 2026.

- 8 P. Angelini, 'Crypto-assets, stablecoins, and anti-money laundering', opening remarks at the 5th UIF Bocconi Workshop on 'Quantitative Methods and Fighting Economic Crime', Rome, 28 November 2025.

- 9 Notably Europe's MiCAR and the United States' GENIUS Act.

- 10 Between 2011 and 2022 the number of active correspondent banks fell by 30 per cent globally, with some regions experiencing reductions of up to 50 per cent (see the CPMI quantitative review of correspondent banking data).

- 11 Post-crisis prudential and AML/CFT reforms have strengthened financial integrity but, together with low margins, have reduced banks' participation in less profitable corridors. See FSB, Report to the G20 on actions taken to assess and address the decline in correspondent banking, 6 November 2015; T. Rice, G. von Peter and C. Boar, 'On the global retreat of correspondent banks', BIS Quarterly Review, March 2020.

- 12 In a correspondent banking arrangement, the correspondent bank holds deposits owned by a foreign bank (the respondent bank) and provides this respondent bank with payment and other services. See CPMI, Correspondent banking, July 2016. If the bank does not hold an account with a correspondent bank in the destination country, the transaction must be routed through a third party (typically a large international bank that maintains links with both sides). This arrangement adds layers of complexity and cost: multiple currency conversions, mismatched operating hours across time zones, repeated know-your-customer checks, and other bureaucratic hurdles that slow down the process and make it more expensive.

- 13 Interoperability refers to the ability of end users to transact with each other seamlessly across payment systems (see C. Boar, S. Claessens, A. Kosse, R. Leckow and T. Rice, 'Interoperability between payment systems across borders', BIS Bulletin, 49, 2021). It operates at three levels: at the technical level, systems share common standards and formats so they can physically connect; at the semantic level, they speak the same language so that data are interpreted consistently across all of them; and at the business level, they agree on the rules - who can participate, under what conditions, and how to handle failures.

- 14 The G20 Roadmap aims to make cross-border payments faster, cheaper, more transparent and more inclusive. Specifically, it seeks to achieve quantitative targets for each of these four objectives and for three different market segments: wholesale, retail and remittances. For the wholesale segment, however, it was deliberately decided not to set a quantitative cost target.

- 15 In February 2023, the work was reprioritized around three main priority themes: (a) payment system interoperability and extension, (b) legal, regulatory and supervisory frameworks, and (c) data exchange and message standards.

- 16 CPMI, Extending and aligning payment system operating hours for cross-border payments. Final report, May 2022.

- 17 CPMI, Improving access to payment systems for cross-border payments: best practices for self-assessments, May 2022.

- 18 APIs are a set of rules and specifications to enable software programmes to communicate with each other, which form an interface between different programmes to facilitate their interaction. See CPMI, Promoting the harmonisation of application programming interfaces to enhance cross-border payments: recommendations and toolkit. Report to the G20, October 2024.

- 19 CPMI, Linking fast payment systems across borders: governance and oversight. Final report to the G20, October 2024.

- 20 ISO 20022 is a global messaging standard for financial communications, launched by the International Organization for Standardization (ISO) in 2004. It standardizes data objects, rules, and processes to enhance interoperability between financial institutions, market infrastructures, and end users across business domains such as payments, securities, and treasury. ISO 20022 is recognized in the G20 Roadmap for enhancing cross-border payments as a solution to harmonize fragmented messaging standards, and improves processing efficiency, reduces costs, accelerates transactions, and strengthens compliance, fraud prevention, and risk management in financial infrastructures.

- 21 CPMI, Harmonised ISO 20022 data requirements for enhancing cross-border payments. Updated report, February 2026.

- 22 T. Lammer, F. Leppanen and F. Semorile, 'Enhancing cross-border payments step by step: insights from the 2025 monitoring survey', CPMI Brief, forthcoming.

- 23 An FPS, also referred to as an instant payment system, is a retail payment system that clears and/or settles end-user (or retail) payments in which the transmission of the payment message and the availability of 'final' funds to the payee occur in real time or near real time, and on as near to a 24-hour and seven-day (24/7) basis as possible.

- 24 An RTGS system is defined as a wholesale payment system that enables the real-time gross settlement of predominantly interbank (or wholesale) payments. RTGS is the continuous process of settling payments on an individual order basis, without netting debits with credits.

- 25 FSB, G20 Roadmap for enhancing cross-border payments. Consolidated progress report for 2025, 9 October 2025.

- 26 World Bank, Remittance Prices Worldwide Quarterly, 54, September 2025.

- 27 Similarly, several Iranian banks were disconnected in 2012, following coordinated sanctions by the European Union and the United States, adopted in response to the expansion of Iran's nuclear programme in contravention of international agreements.

- 28 In 2014, Russia introduced a proprietary messaging system (SPFS) and, in 2015, a card network (Mir) to process domestic payments in the absence of access to SWIFT and international card schemes, respectively. In 2015, China launched the Cross-Border Interbank Payment System (CIPS) to support renminbi internationalization, operating both on SWIFT standards and a parallel proprietary messaging system. Other examples of proprietary messaging systems are India's Structured Financial Messaging System and Iran's SEPAM. More recently, BRICS members have also announced new multilateral initiatives - such as the BRICS Cross-Border Payments Initiative and the DLT-based BRICS Pay - aimed at enhancing interoperability among domestic payment systems. See C. Di Luigi and A. Perrella, 'The architecture of cross-border finance', Mercati, infrastrutture, sistemi di pagamento, Banca d'Italia, forthcoming.

- 29 Recent empirical evidence shows that implementing a domestic fast payment system can also benefit remittances by reducing costs for end users by up to 1 percentage point. See M. Brandi, A. Di Iorio and A. Nobili, 'Send me money ASAP: fast payment systems and the cost of remittances', Mercati, infrastrutture, sistemi di pagamento, Banca d'Italia, forthcoming.

- 30 The global settlement window is the time period during which the largest number of RTGS systems are operating simultaneously. At present, the global settlement window is generally defined as the time span from 06:00 to 11:00 Greenwich Mean Time (GMT) on business days.

- 31 Since 1-3 per cent of payments generate inquiries that typically require 5-10 manual touchpoints and rely heavily on free-format data, a harmonized and global implementation of ISO 20022 will significantly reduce manual effort and accelerate investigations, cutting resolution times by up to 80 per cent (see E. Fitzgerald, A. Illes, T. Lammer, F. Leppanen and F. Semorile, 'Moving on up: results of the 2024 cross-border payments monitoring survey', CPMI Brief, 10, 2025).

- 32 In a two-tier monetary system, central bank money serves as the common settlement asset that eliminates credit risk among private institutions and anchors trust in the broader financial system. Digital transformation does not alter this logic - it reinforces it. What will change is the technological form of this architecture: retail and wholesale central bank digital currencies, tokenized bank deposits and modernized settlement infrastructures will allow it to evolve while preserving its core principles. As payment systems grow more sophisticated and interconnected, the stabilizing role of central bank money becomes more, not less, important. For a fuller discussion, see F. Panetta, 'The struggle to reshape the international monetary system: slow- and fast-moving processes', Whitaker Lecture, Central Bank of Ireland, Dublin, 9 December 2025.

- 33 The Eurosystem and Banca d'Italia are already moving in this direction, with initiatives such as the digital euro and the Pontes and Appia projects. The digital euro aims to safeguard the role of public money in retail payments. It is an electronic equivalent to cash and would therefore complement banknotes and coins for retail use. The Pontes project, operating on a short- to medium-term horizon and with a Pilot phase planned for 2026, aims to connect DLT platforms with T2, the wholesale payment infrastructure currently used in the euro area, thus extending the use of central bank money to interbank DLT-based transactions. The Appia project has a broader, longer-term perspective, envisaging the creation of a fully DLT-based ecosystem for settling wholesale transactions in central bank money, including cross-border payments.

- 34 FSB, Recommendations for regulating and supervising bank and non-bank payment service providers offering cross-border payment services. Final report, 12 December 2024.

- 35 The revised FATF Recommendation 16 on payment transparency specifies the information required in payment messages to improve transparency and traceability.

- 36 FSB, Recommendations to promote alignment and interoperability across data frameworks related to cross-border payments. Final report, 12 December 2024.

- 37 TIPS already settles instant payments in euros, Swedish krona and Danish kroner, with the Norwegian krone expected to join in 2028. On 29 September 2025, the Governing Council of the European Central Bank approved the launch of an exploratory phase to evaluate the potential establishment of a bilateral link between TIPS and the Swiss Interbank Clearing Instant Payments (SIC IP) system. In the same vein, on 20 November 2025, it decided to start the realization phase for interlinking with India's Unified Payments Interface (UPI), an instant payment system developed by the National Payments Corporation of India and regulated by the Reserve Bank of India.

- 38 In Europe, effective examples of stakeholder engagement in the payments sector include cooperative bodies such as the Euro Retail Payments Board (ERPB), the Advisory Group on Market Infrastructures for Payments (AMI-Pay), and national payments committees - such as Italy's Comitato Pagamenti Italia - where public authorities and market participants jointly address issues relevant to the evolution of the payments ecosystem, under the aegis of central banks. At global level, the FSB brings together senior policymakers and industry leaders through the Payments Summit and legal experts from the private sector through the Legal, Regulatory and Supervisory Task Force. The CPMI provides the platform for two industry groups: the Cross-border Payments Interoperability and Extension (PIE) task force, which provides expert advice on market conventions and industry practices, and the Harmonization Panel on ISO 20022, which promotes and supports industry efforts to adopt the harmonization requirements, to maintain them and, where appropriate, propose updates.

- 39 A concrete illustration is Banca d'Italia's work with Western Balkan countries to modernize domestic payment infrastructures and lay the foundations for more seamless cross-border payments. As the operator of TIPS, Banca d'Italia is collaborating with the central banks of Albania, Bosnia and Herzegovina, Kosovo, Montenegro and North Macedonia, to provide a TIPS clone. This platform will enable domestic instant payments both in local currencies (where applicable) and in euros (commercial bank money), alongside cross-border and cross-currency functionalities. In addition, the TIPS clone can easily be bilaterally linked with TIPS, highlighting how technical cooperation can evolve into broader regional collaboration by revealing shared priorities and integration opportunities.

- 40 For example, the CPMI's Community of Practice on Payment Systems is a forum for central banks to exchange views on developing or upgrading payment systems, including an international dimension in their desing, and discussing innovative developments. The community brings together representatives from over 60 jurisdictions as well as from regional and international organizations. It was launched in 2023 with the aim of strengthening the involvement of both G20 and non-G20 central banks in the cross-border payments programme and supporting the implementation of payment system enhancements.

Instagram

Instagram