Survey on Inflation and Growth Expectations - 2024 Q1

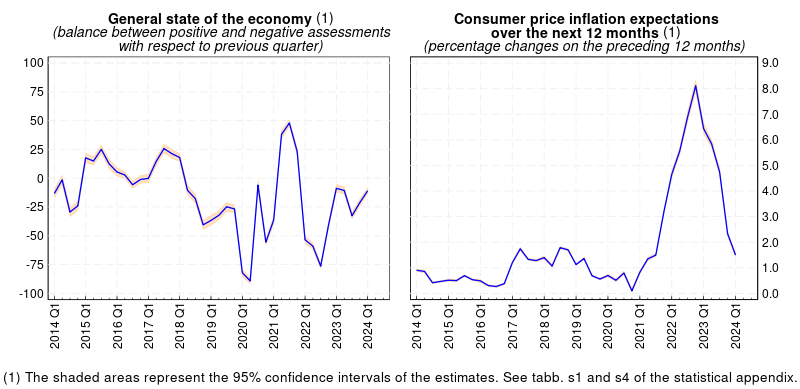

According to the survey conducted between 23 February and 18 March 2024 among Italian industrial and service firms with 50 or more employees, in the first quarter of this year opinions regarding the general state of the economy and firms' own business conditions were less negative than in the previous period. However, around one-third of manufacturing firms experienced delays or price increases in input procurement as a result of tensions in the Red Sea.

Demand was still weak but improving overall, with positive trends in services and in construction and less negative developments in industry excluding construction. Foreign sales too provided a boost, following two quarters of contraction. The outlook for the second quarter is for a recovery in sales, buoyed by both domestic and foreign demand.

Assessments of investment conditions and access to credit were significantly less downbeat than in the previous survey round. The balance between expectations of an increase and those of a reduction in investment spending in 2024 remained positive. Employment is expected to continue to grow in the second quarter.

Over the last 12 months, firms' selling prices have continued to slow, with changes well below 2023 peaks. Consumer price inflation expectations fell to 1.5 per cent across all time horizons, hitting their lowest levels since 2021 in all sectors.

Report text

-

10 April 2024

-

10 April 2024

-

10 April 2024TablesZIP 361 KB

Instagram

Instagram