Survey on Inflation and Growth Expectations - 2024 Q3

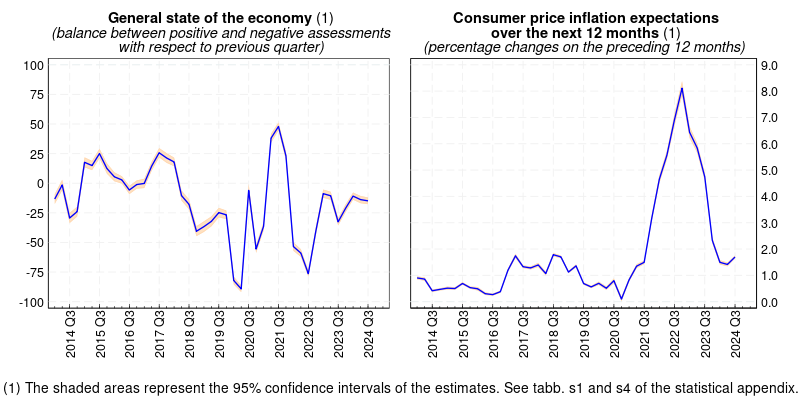

According to the survey conducted between 26 August and 16 September 2024 among Italian industrial and service firms with 50 or more employees, opinions on the general state of the economy remained cautious in the third quarter of this year. Assessments of both domestic and foreign current demand worsened overall, driven by the weak sales of firms in industry excluding construction. Expectations for the next quarter are also less positive compared with last spring across all sectors of activity. The outlook for firms' own business conditions in the short term remains weak; it is still mainly affected by economic and political uncertainty.

Firms continue to give negative assessments of investment conditions, while those for credit access remain stable. The overall liquidity position is still considered satisfactory. According to firms' expectations, total investment spending will slow this year.

The employment growth forecast for the next quarter is less favourable than in the previous survey, although it is still expected to rise, especially in construction.

Firms' selling prices over the last 12 months have grown less sharply compared with the previous survey; for the next 12 months, firms in industry excluding construction and in services continue to expect moderate growth in their prices, while those in construction anticipate an acceleration. Firms' expectations for consumer price inflation rose slightly across all time horizons, though they remained at low levels.

A special focus section included in this survey showed that, within the next two years, artificial intelligence will be used by about one third of industrial firms and by two fifths of service firms, especially the largest ones.

Report text

-

08 October 2024

-

08 October 2024

-

08 October 2024TablesZIP 419 KB

Instagram

Instagram