Survey of Industrial and Service Firms in 2019

Statistics

Main results

The survey was carried out between 29 January and 14 May, a period marked by the spread of the COVID-19 epidemic and by the containment measures taken by the Government. Starting from the second half of March, the traditional questionnaire was complemented by some additional questions intended to assess how the epidemic was affecting firms' business and how firms were responding to it.

According to the respondent firms, the health emergency has mainly entailed a sharp contraction in demand, especially domestic, for goods and services. Financial difficulties, which were reported very frequently but were deemed less significant than those arising from the fall in sales, are ascribable to delays in the recovery of payments and the need to meet current expenses.

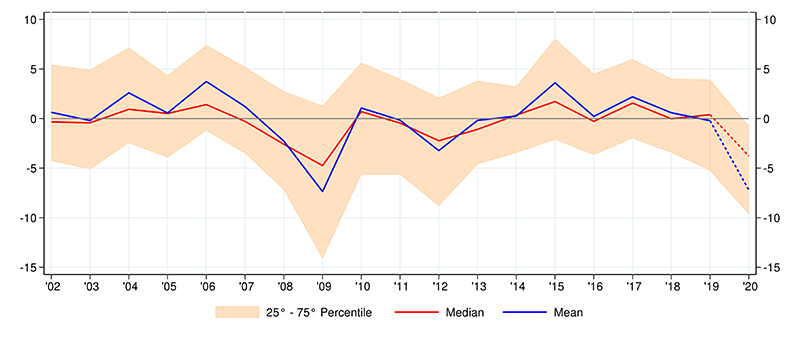

During the year as a whole, firms' turnover is expected to fall by about 7 per cent, after stagnating in 2019; The drop appears to be concentrated in the first half of the year (-25.8 per cent) and sharper for firms in trade, in the accommodation and catering industry (-37.5 per cent), and in the textiles, clothing, leather and footwear sector (-32.2 per cent). The contraction in employment expected in 2020, equal to 1.3 per cent, is very small compared with the expected fall in sales, likely owing to the ample recourse to wage supplementation.

In 2019, the output of construction firms with at least 10 workers accelerated, driven by the positive performance of those involved in public works; employment also benefited from this, holding stable for the first time since 2006. However, both output and employment are expected to turn downwards again in 2020.

Turnover (1)

(percentage changes)

Note: (1) Does not include the construction sector. Data weighted by population weights and turnover. Dotted lines indicate firms’ expectations for 2020.

Reference period: year 2019

Full text

-

01 July 2020

-

01 July 2020Table IsecoZIP 99 KB

-

01 July 2020Table InvindZIP 321 KB

-

03 July 2017

-

17 November 2020

-

01 July 2020Questionnaire IsecoPDF 84 KB

-

01 July 2020

Instagram

Instagram