Survey of Industrial and Service Firms in 2020

Statistics

Main results

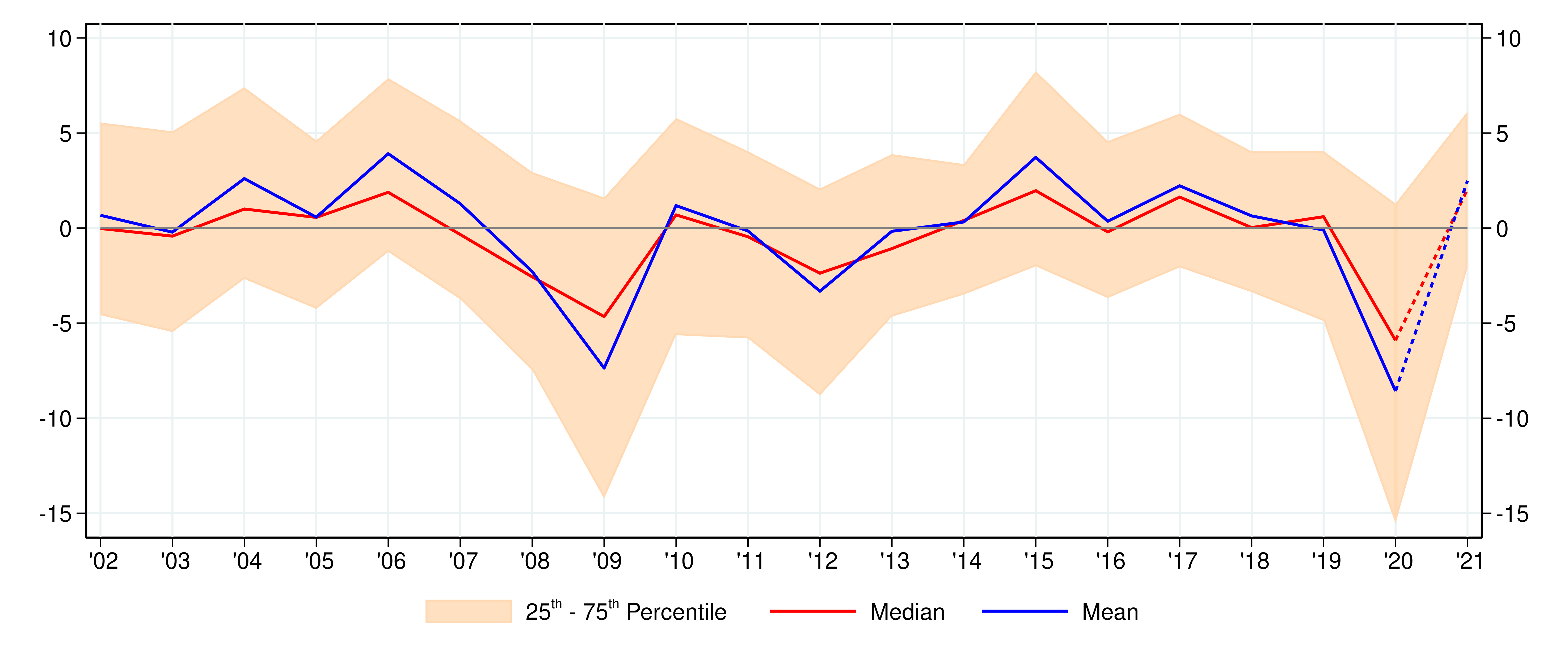

In 2020, the Italian production system was hit hard by the impact of the COVID-19 pandemic. Sales declined by 8.6 per cent; the contraction in turnover affected most firms and was worse for those in the sectors more directly impacted by the measures adopted to contain the virus. Hours worked fell by 10 per cent, although the number of persons employed only went down by 2.4 per cent, thanks to the freeze on dismissals and the widespread recourse to wage supplementation schemes. The average growth in selling prices slowed to 0.9 per cent.

The outbreak of the pandemic in the early months of the year generated exceptionally high uncertainty over the economic outlook, which led to an immediate reduction in investment plans across the board, compared with those drawn up previously. Overall, investment spending fell by 8.6 per cent, against the plans for growth made at the end of 2019.

For this year, firms expect sales to pick up again, although this would only partly compensate for the fall recorded in 2020. They also anticipate a marked increase in investment, both in services and in industry, and that employment levels will basically remain the same. On average, selling prices are expected to accelerate significantly.

Output in the construction sector fell by 7 per cent despite growth in the public works segment. This was accompanied by a fall in profitability and an increase in the demand for financing. The number of persons in employment did however increase. Firms expect a marked recovery in output in 2021, in both public and private sector construction.

Turnover (1)

(percentage changes)

Note: (1) Does not include the construction sector. Data weighted by population weights and turnover. Values at constant prices calculated based on the average deflators obtained from the survey. The dotted lines indicate firms’ expectations for 2021.

Reference period: 2020

Full text

-

01 July 2021

-

01 July 2021TablesZIP 189 KB

-

03 July 2017

-

01 July 2021

Instagram

Instagram