Survey of Industrial and Service Firms in 2017

Statistics

Main results

According to the Bank of Italy survey conducted last spring, in 2017 the increase in sales of industrial and private non-financial services firms with at least 20 employees gained strength on both domestic and foreign markets. The acceleration stimulated labour demand, which rose at a pace similar to that of the previous year. Sales prices returned to growth at a more sustained rate; firms attributed this mainly to the trend in the prices of raw materials and to stronger demand.

Firms expect sales to keep growing robustly in 2018, although at a slower pace compared to last year; price growth is also expected to stabilize.

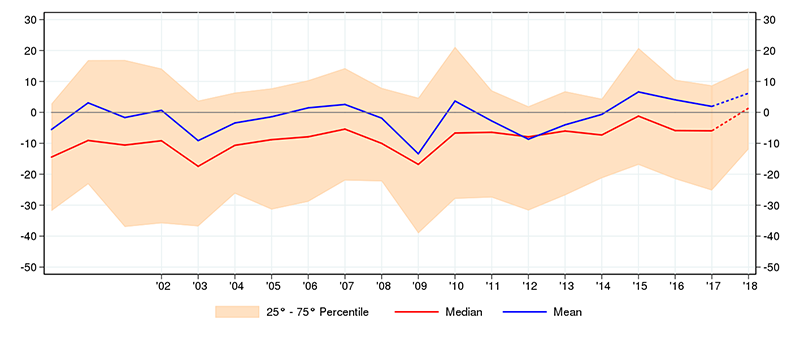

Investment expenditure increased further, due especially to the growth in capital accumulation by small and medium-sized firms. Planned investment is expected to pick up in 2018, driven mostly by greater investment by firms with at least 500 employees, which as a group contributed little to total investment growth over the last two years.

The output of construction firms with at least 10 employees fell again in 2017, although by less than in the previous year. The contraction reflected a decline in public works, which was only partially offset by the recovery in housing.

The balance between the share of firms expecting an improvement and those that foresee a worsening in credit conditions remains positive and essentially unchanged in the industrial and services sectors; in construction, it is positive for the second consecutive year and is increasing.

Investment (1)

(percentage changes)

Note: (1) Does not include the construction sector. Total expenditure on tangible assets and on software and databases and mineral exploration; calculated at constant prices using deflators found in the survey. Statistics weighted by firm distribution and investment spending. Dotted lines indicate firms’ expectations for 2018.

Reference period: 2017

Full text

-

26 March 2019

-

26 March 2019

-

02 July 2018Survey of Industrial and Service Firms in 2017PDF 1016 KB

-

02 July 2018TablesZIP 336 KB

-

03 July 2017

Instagram

Instagram