Survey on Inflation and Growth Expectations - 2022 Q1

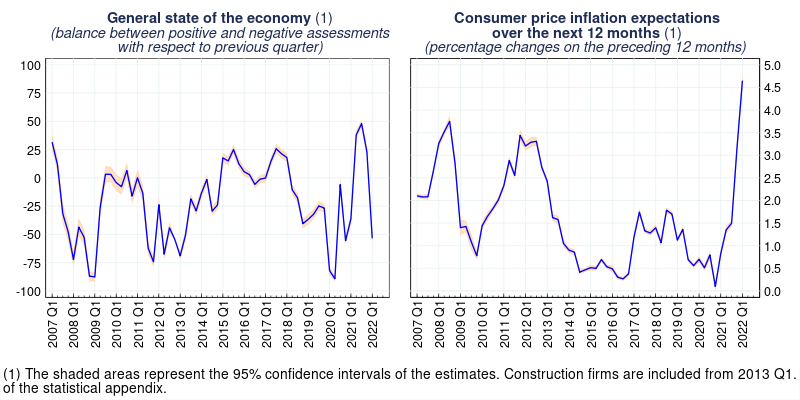

According to the survey conducted between 23 February and 16 March 2022 among Italian industrial and service firms with 50 or more employees, opinions regarding the general economic situation in the first quarter of 2022 and their own operating conditions in the following quarter have worsened compared with the previous survey, reflecting the effects of the Russian invasion of Ukraine, which began immediately after the survey for this quarter was launched. While they are worsening significantly, firms' assessments are much less negative than those prevailing during the first wave of the pandemic.

The main obstacles to economic growth in the months to come are the uncertainty about economic and political factors, developments in commodity prices, and international trade tensions. Demand dynamics are expected to remain positive, though weaker.

Despite the sharp worsening of investment conditions, a further expansion in investment is expected for 2022, though at a slightly more moderate pace than that reported in the last survey. Employment looks set to continue to grow in the second quarter of 2022.

Expectations for consumer price inflation have reached historically high levels and remain well above 2 per cent across all time horizons (12-month expectations are now equal to 4.6 per cent, those between 3 and 5 years stand at 3.8 per cent). Selling prices have risen and will likely increase further over the next 12 months, driven by the increase in inflation expectations and in the prices of production inputs.

Report text

-

07 April 2022

-

07 April 2022

-

07 April 2022TablesZIP 327 KB

Instagram

Instagram