The Bank of Italy authorizes market access for entities wishing to carry out licensed banking and financial activities that meet the relevant legal requirements, with a view to ensuring the sound and prudent management of financial intermediaries and the overall stability, effectiveness and competitiveness of the financial system. In this capacity, it performs the following functions:

- it submits bank licensing applications to the ECB, in accordance with the provisions of Regulation (EU) 1024/2013;

- authorizes financial intermediaries under Article 106 of the Consolidated Law on Banking (Testo Unico Bancario, TUB) including loan guarantee schemes, pawnbrokers and trust companies; asset managers (SGRs, SICAFs, SICAVs); payment institutions (PIs); and electronic money institutions (EMIs);

- authorizes the registration of microcredit companies in the list under Article 111 of the TUB, pending the establishment of a special body responsible for managing and supervising these companies.

Investment firms and crowdfunding service providers are licensed by CONSOB. For the purpose of issuing the licence, CONSOB requests the opinion of the Bank of Italy.

Specific information on how the Bank of Italy authorizes the different categories of intermediaries is available in the dedicated sections, which can be accessed from the links in the table below.

| Intermediary | Activities | Duration | Competent authority |

|---|---|---|---|

| Banks | Collecting savings from the general public and granting loans | 180 days | European Central Bank / Bank of Italy |

| Financial intermediaries | Lending in any form | 180 days | Bank of Italy |

| Loan guarantee schemes | Lending and issuing collective guarantees for exposures | 180 days | Bank of Italy |

| Trust companies | Safekeeping and administering assets entrusted to them by trustors based on a fiduciary mandate | 180 days | Bank of Italy |

| Pawnbrokers | Short-term financing to natural persons against pledged movable assets | 180 days | Bank of Italy |

| Microcredit operators | Loans for small amounts combined with the provision of ancillary services | 90 days | Bank of Italy |

| Payment Institutions | Payment services | 90 days | Bank of Italy |

| Electronic Money Institutions | Issuing e-Money | 90 days | Bank of Italy |

| Asset managers (SGRs, SICAVs, SICAFs) | Asset management | 90 days | Bank of Italy (after consulting CONSOB) |

The regulation applicable to financial intermediaries subject to licensing by the Bank of Italy are available on the Bank of Italy's web site. Supervisory publications and regulations are listed by sector, year and topic on the 'Banking and Financial Supervision' page. In addition, an e-mail alert service provides continuously updated news and information.

The licensing procedure

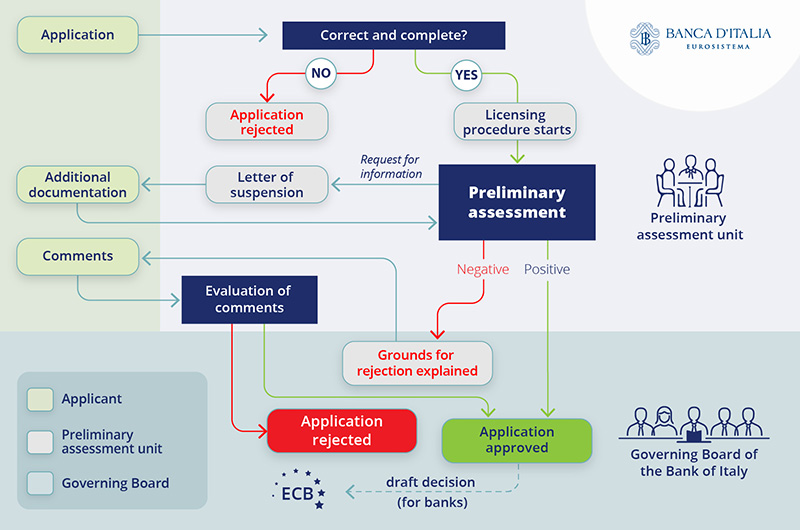

The licensing procedure (see infographic), only starts once the Bank of Italy has received a correct and complete application. If these requirements are not met, the procedure will not start and the applicant will be informed of the reasons why the application is considered incorrect or incomplete.

Licensign applications must be submitted by certified email (PEC) (see the Contacts section below). Applications for banking licences must be submitted via the Banking supervision portal or IMAS portal, as required by the Bank of Italy Regulation of 23 December 2021.

Before submitting an application, intermediaries may contact the Bank of Italy (see the Contacts section) and request a meeting to discuss their applications. These meetings are intended to assist the firm and are not compulsory. They do not count towards the application deadlines.

During the licensing procedure, the Bank of Italy may request additional information and certifications, carry out appraisals and investigations, and obtain the opinion of domestic and foreign authorities. Where provided for by law, the procedure may be suspended. Applications may be suspended for up to 180 days, after which the remaining time of the original deadline will resume.

Depending on the outcome of its preliminary assessment, the Bank of Italy will proceed as follows:

- positive outcome: the Bank of Italy grants the licence or, for banks, notifies the ECB of its proposal to grant the banking licence. The licence may be subject to restrictions or recommendations on measures to take to ensure compliance with prudential rules and sound and prudent management;

- negative outcome:

before rejecting an application, the Bank of Italy notifies the firm of the reasons for its decision. This notification suspends the procedure. Over the following 10 days, the applicant has the right to express its own observations in writing. The procedure resumes 10 days after the receipt of the firm's reply or, in the absence of a reply, 10 days after the Bank of Italy's notification. If the grounds for rejection are confirmed, the final rejection decision will state the reasons for not accepting the firm's comments, if any, and any further reasons arising from the comments.

The following provisions apply to the licensing procedure:

-

Bank of Italy Regulation under Law 241/1990; the deadlines are indicated in List 1a and List 1b;

- agreements signed with other authorities;

- supervisory rules and regulations applicable to each intermediary.

For specific information relating to the licensing procedures for banks, please see the dedicated section.

Contacts

For licences to operate in the banking and financial markets under the Bank of Italy's remit, contact the Supervisory Institutional Relations Directorate, New Banks and Financial Intermediaries Division, at the following email addresses:

- email: Servizio.Riv.Costituzioni@bancaditalia.it

- certified email (PEC): riv@pec.bancaditalia.it

Emails can be sent to the above addresses to request meetings or ask for clarifications strictly relating to the licensing process (for example with reference to timing, the applicable legislation, or the information and documents to be submitted). For queries of a general nature relating to Bank of Italy regulations, please see the dedicated page (only in Italian). For further details on the administrative procedure please see the FAQs below.

Questions regarding matters already covered on the Bank of Italy website will not be answered.

Applications from non-bank intermediaries must be submitted to the Bank of Italy by PEC. In accordance with Bank of Italy Regulation of 23 December 2021, banks must use the IMAS Portal.

When the application involves innovative initiatives in the fields of financial and payment services, and where certain requrements are met, it is possible to utilize the following innovation facilitators): Fintech Channel, Regulatory Sandbox and Milano Hub. Each of these has specific requirements, which are outlined in the respective sections.